)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

- 5.6.2 Maintenance

- 5.6.2.1 Program Scope and Objective

- 5.6.2.1.1 Background

- 5.6.2.1.2 Authority

- 5.6.2.1.3 Responsibilities

- 5.6.2.1.4 Program Management and Review

- 5.6.2.1.5 Program Control

- 5.6.2.1.6 Terms/Definitions/Acronyms

- 5.6.2.1.7 Related Resources

- 5.6.2.2 CEASO Confirmation of New Collateral to IRACS

- 5.6.2.3 CEASO Semi-Annual Verification

- 5.6.2.3.1 CEASO Sufficiency Review

- 5.6.2.3.2 CEASO Physical Verification

- 5.6.2.4 CEASO Annual Reconciliation of Collateral Holdings

- 5.6.2.5 Transfer to Another Area

- 5.6.2.5.1 Transferring Employee Procedures

- 5.6.2.5.2 Transferring CEASO Procedures

- 5.6.2.5.3 Receiving CEASO Procedures

- 5.6.2.6 Disposition of Collaterals (Overview)

- 5.6.2.7 CEASO Action for Account Satisfied

- 5.6.2.7.1 Surety Bond

- 5.6.2.7.2 Mortgages

- 5.6.2.7.3 Other Collateral

- 5.6.2.8 CEASO Actions for Agreement in Default

- 5.6.2.8.1 Surety Bond

- 5.6.2.8.1.1 Estate Tax Installment Cases

- 5.6.2.8.1 Surety Bond

- 5.6.2.9 International Collateral Maintenance and Disposition

- 5.6.2.9.1 Foreign Investment Real Property Tax Act (FIRPTA)

- 5.6.2.9.2 Federal Insurance Excise Tax

- 5.6.2.9.3 Captive Insurance

- 5.6.2.9.3.1 Examination Verification Requests

- 5.6.2.9.3.2 Release of Letter of Credit

- 5.6.2.9.3.3 Meeting "Office/Assets Test"

- 5.6.2.9.3.4 Reduction of Letter of Credit

- 5.6.2.9.3.5 Expiration of Letter of Credit

- 5.6.2.9.3.6 CEASO Monitoring

- 5.6.2.9.3.7 Liquidation of Letters of Credit

- 5.6.2.9.4 Expatriate Tax

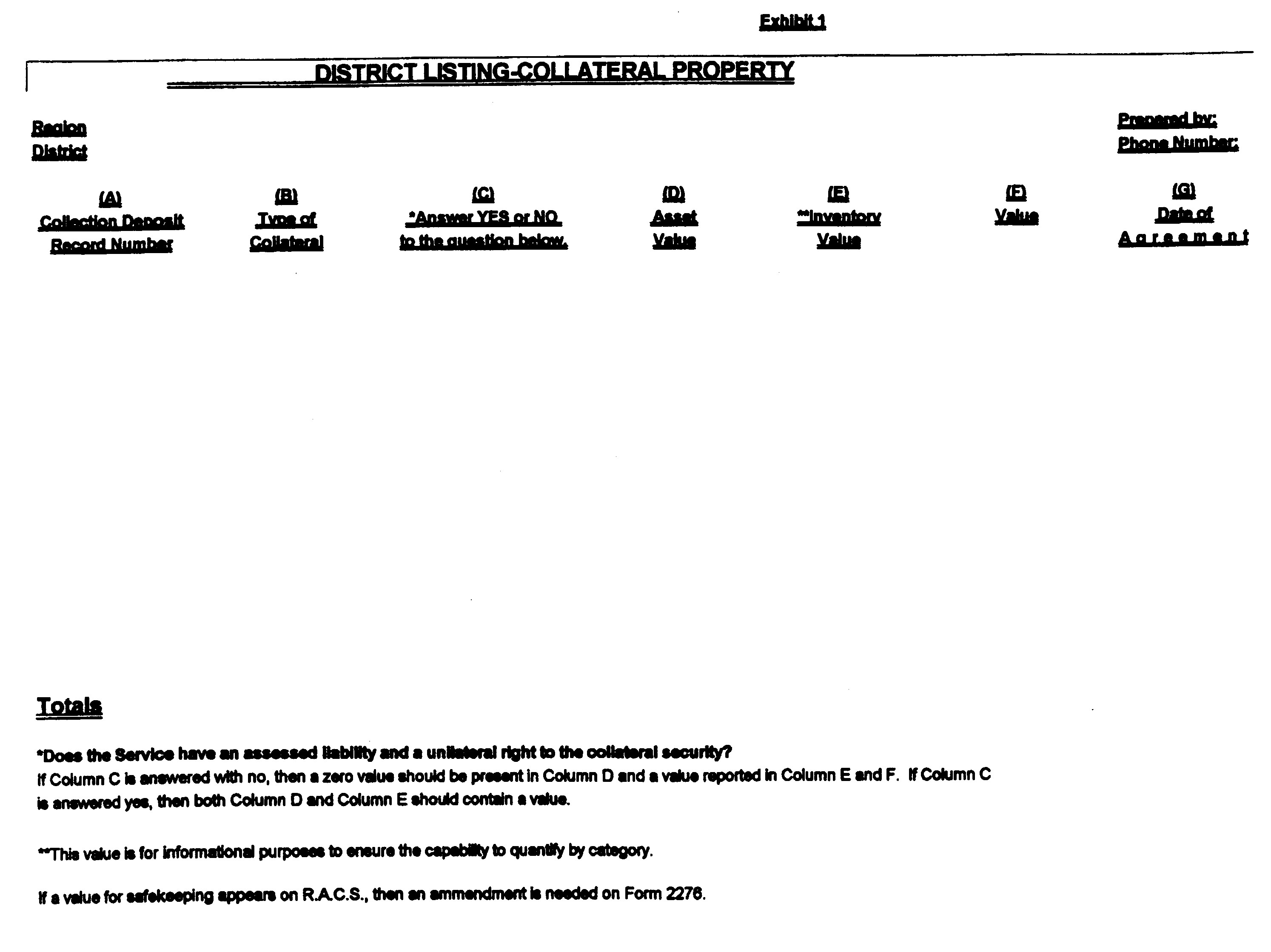

- Exhibit 5.6.2-1 Area Listing —Collateral Property

- Exhibit 5.6.2-2 Pattern Letter P–299

- Exhibit 5.6.2-3 Pattern Letter P–300

- Exhibit 5.6.2-4 Pattern Letter P–301

- 5.6.2.1 Program Scope and Objective

Part 5. Collecting Process

Chapter 6. Collateral Agreements

Section 2. Maintenance

5.6.2 Maintenance

Manual Transmittal

December 08, 2020

Purpose

(1) This transmits revised IRM 5.6.2, Collateral Agreements, Maintenance.

Material Changes

(1) The following is a description of the material changes to this IRM:

| IRM Section | Description of Change |

|---|---|

| IRM 5.6.2.1 | A new subsection, Program Scope and Objectives, was inserted to provide internal controls information. All following subsections were renumbered. |

| IRM 5.6.2.4(4) | Updated to correct the annual reconciliation date. |

| IRM 5.6.2.4(5) | Updated the documents included in the reconciliation. |

| IRM 5.6.2.4(7) | Removed the table regarding collateral property because guidance will vary based on the National RACS Reconciliation Coordinator. |

| Throughout | Replaced all references to "Advisory" with "Civil Enforcement Advice and Support Operations" (CEASO). |

| Throughout | Updated citations, IRM references and links. Editorial and grammatical changes made for clarity. |

Effect on Other Documents

This supersedes IRM 5.6.2, dated September 27, 2011.Audience

Small Business/Self Employed Collection EmployeesEffective Date

(12-08-2020)Ronald Takakjy

Acting Director, Collection Policy

Small Business/Self Employed Division

-

Purpose. This Internal Revenue Manual (IRM) provides the procedures for maintaining collateral agreements. While many topics are touched upon in this chapter, comprehensive guidance about all of them cannot be included here. As you use this chapter, remain alert for references to other resources, such as related IRM’s and websites and access that guidance as needed to ensure a thorough understanding of topics.

-

Audience. These procedures and guidance apply to IRS Field Collection employees, Civil Enforcement Advice and Support Operations(CEASO) , and group managers.

-

Policy Owner. Director, Collection Policy, Small Business/Self-Employed Division (SBSE)

-

Program Owner. SBSE Collection Policy, Case Resolution Alternatives (CRA), is the program owner of this IRM

-

Primary Stakeholders. This IRM impacts:

-

Field Collection

-

CEASO

-

Counsel

-

-

Program Goal. There are circumstances in which the government accepts a pledge, guaranteed by security, for the performance of a particular act (a “collateral agreement”). It is very important that these agreements be monitored so that the taxpayer either complies with their pledge, or the appropriate action is taken. By following the procedures in this IRM, the employee will be able to properly maintain and resolve collateral agreements.

-

This section provides guidance to collection employees for maintaining collateral agreements. A collateral agreement is a pledge, guaranteed by security, for the performance of a certain act, (i.e., payment of a delinquency or the filing of a return).

-

IRC 7101, Form of bonds

-

26 CFR 301.7101-1, Form of bond and security required

-

The Director, Collection Policy is the executive responsible for the policies and procedures to be employed by collection personnel.

-

Field Collection group managers, CEASO group managers, Field Collection territory managers, and CEASO territory managers are responsible for ensuring the guidance and procedures described in this IRM are complied with.

-

Collection employees are responsible for following the guidance provided in the IRM.

-

Program Reports.

-

National Quality Review System (NQRS) Reports

-

ICS Reports

-

IRACS Report

-

-

Program Effectiveness. The program effectiveness is measured by the following review types and by level of management.

-

Case reviews are conducted by group managers and are recorded in the Embedded Quality Review System (EQRS)(managers) or National Quality Review System(NQRS)(Field Quality) to ensure compliance with this IRM.

-

Operational reviews are conducted by territory managers and area directors annually to evaluate program delivery and conformance to administrative and compliance requirements.

-

Program reviews are conducted by Headquarters Policy annually to evaluate program delivery and conformance to administrative and compliance requirements.

-

-

Collateral agreements are monitored by these types of program controls:

-

ICS open control

-

Unique serial number

-

Collateral agreements are input into the Redesigned Revenue Accounting and Control System (RRACS). The RRACS Unit in Ogden monitors these agreements.

-

Certain actions relating to collateral agreements that require managerial approval.

-

-

Frequently used terms within this IRM along with their definition include:

-

Bond: a debt investment in which an investor lends money to an entity which borrows the funds for a defined period of time at a variable or fixed interest rate.

-

Escrow Arrangements: an arrangement in which one party deposits an asset with a third person, who, in turn, makes a delivery to another party if and when the specified conditions of the contract are met.

-

Mortgage: a legal agreement by which a bank or other creditor lends money at interest in exchange for taking title of the debtor’s property, with the condition that the conveyance of the title becomes void upon the payment of the debt.

-

Security: a fungible, negotiable financial instrument that holds some type of monetary value.

-

-

This table lists acronyms commonly used within this IRM and their definitions.

Acronym Definition ACQ Acquired CDR Collateral Deposit Record EQRS Embedded Quality Review System FC Field Collection FET Federal Excise Tax FIRPTA Foreign Investment Real Property Tax Act ICS Integrated Collection System IRACS Interim Revenue Accounting Control System IRC Internal Revenue Code IRM Internal Revenue Manual LOC Letter of Credit NFTL Notice of Federal Tax Lien NQRS National Quality Review System QDOTS Qualified Domestic Trusts QMS Quality Measurement Staff RRACS Redesigned Revenue Accounting and Control System

-

Related resources include:

-

IRM 10.5.2, Privacy and Information Protection

-

Treasury Department Circular No. 570 may be found at https://fiscal.treasury.gov/surety-bonds/circular-570.html

-

IRM 5.5.8.5.1, Bond/Lien Determinations for Estate Tax Deferred Under IRC § 6166

-

IRM 21.8.1.12.20, IRC 877A - Mark-To-Market Exit Tax, for complete guidance for expatriation and taxable consequences.

-

All IRS personnel must be familiar with and responsible for execution of duties in accordance with taxpayer rights afforded by the provisions in the Internal Revenue Code, including the Taxpayer Bill of Rights (TBOR) listed in IRC 7803(a)(3). For additional information about TBOR, see https://www.irs.gov/taxpayer-bill-of-rights.

-

IRM 5.6.1.3.3, Estate Tax Bonds and Other Collateral

-

-

Ogden Service Center Accounting Operations records collateral transactions into the Interim Revenue Accounting Control System (IRACS) from the Form 2276, Collateral Deposit Record, Part 3, which is submitted to IRACS from CEASO. Refer to IRM 3.17.63.10.3.1, Account Series 3200, Collateral Held (Real Account, DR Normal Balance)(Ogden Only).

-

At any time that the value or status of collateral changes during a given month, CEASO will:

-

Prepare an amended Form 2276 and write “Amended” in red,

-

Send Part 3 of the amended Form 2276 to the Service Center Accounting Operations,

-

Resolve missing and incorrect items with the Service Center Accounting Operation.

-

-

Semi-annual verification of the Revenue Accounting Control System Area Office Inventory Detail Report (RACS 135) is required. The reports issued by the service center Revenue Accounting Control System (RACS) for March 31 and September 30 will be used for the semi-annual verification.

-

CEASO will:

-

Conduct a semi-annual reconciliation value sufficiency review and verification of all collateral;

-

Prepare a memorandum of confirmation with responses, either agreeing to the Area Office Inventory Detail Report or reconciling any discrepancy(s) to the Service Center Accounting Operation within 30 calendar days after receiving the listing;

-

Retain a copy of the confirmation memorandum and the Inventory Detail Report (collateral account portion).

-

-

CEASO will examine each case file to determine whether collateral is to be:

-

Retained and amount remains sufficient to protect the government’s interest, or

-

Disposed of due to default or resolution of the contested issues. See IRM 5.6.2.5 for disposal instructions.

-

-

CEASO must physically examine each item of collateral listed on the collateral account portion of the RACS 135 Detail Report to ensure complete agreement. Form 2276 6(d) will show the value of the collateral or will be noted "Safekeeping" .

-

List each item, amount and identifying information of collateral on a verification worksheet.

If the envelope is. . . Then. . . not opened it is not necessary to open it. Notate the face of the envelope with the date and names of the persons conducting the review. opened -

Examine the contents to ensure they agree with Form 2276

-

Reseal the envelope and sign and date across the seal.

-

-

When a difference between the contents and what is shown on Form 2276 is discovered then:

-

Determine the reason,

-

Amend the Form 2276 when the difference is accounted for,

-

Reseal the envelope and sign, date across the seal,

-

Record the reason for the difference on the verification worksheet,

-

Report the discrepancies to the Service Center Accounting Operation by photocopy of the amended Form 2276 and write "Amended" in red.

-

-

The Chief Financial Office (CFO) requires that Collection provide a year-end balance of seized assets, acquired property, collateral property, and other property for inclusion in IRS’ fiscal year end financial statements.

-

Since all balances must be validated, the reconciliation serves to:

-

verify and correct asset information,

-

ensure that CEASO’s recorded asset amounts are current and supportable (property and documentation exist), and

-

resolve discrepancies between CEASO records and RACS during this process.

-

-

If all discrepancies are resolved, then adjusted CEASO recorded asset information will match adjusted RACS. The reconciliation process ensures that the most current and supportable information is provided to the CFO.

-

The annual reconciliation of collateral holdings will occur one month prior to the semi-annual reconciliation.

-

Each area will provide to the Headquarters Office—The National RACS Reconciliation Coordinator will provide guidance and a due date for the Annual Reconciliation process, Generally, the reconciliation will include:

-

Revenue Accounting Control System (RACS) Area Office Inventory Detail Report for collateral property (RACS 135) (Exhibit 5.6.2-1)

-

Copies of Form 2276 that were forwarded to the Service Center Accounting Operation during reconciliation to resolve any discrepancies with the current RACS 135

-

Collateral property reconciliation excel worksheet

-

-

Exhibit 5.6.2-1, Area Listing - Collateral Property, will coincide with the columns on Form 2276.

-

Follow the guidance provided by the Coordinator to complete the RACS reconciliation.

-

Do not include in the Collateral 135 Report any Form 2276 that was prepared for a seized item that is being held for safekeeping.

-

A Form 2433 should be attached identifying it as a seized item.

-

Areas must maintain their own control of the seized asset.

-

-

If the balance due, or other underlying assignment, is to be transferred to another area, the collateral must also be transferred.

-

The Collection employee initiating the transfer will:

-

Prepare a memorandum in triplicate to CEASO explaining the transfer;

-

Leave Part 4 of Form 2276 attached to the balance due;

-

Attach copy of memorandum to the balance due;

-

Forward original memorandum and one copy to CEASO.

-

-

Upon receipt of the memorandum, CEASO will:

-

Complete item 20 on all parts of Form 2276 and notate in the "Other block" balance due and collateral transferred to— "Area" and include the area number;

-

Notate in item 11 "Remarks" of Parts 2 and 5 the date and area office to which collateral was transferred;

-

Retain a copy of the memorandum in the case file pending confirmation of the transfer;

-

Send the collateral, a copy of the collection employee memorandum and all parts of Form 2276 via Form 3210 addressed to CEASO in the receiving area by registered mail no later than 10 calendar days of receipt of the transferring employee memorandum;

-

Immediately notate ICS of action taken and establish a reasonable follow-up date.

-

-

Enter a value for area listing—collateral property (see IRM 5.6.2.4)

-

Upon receipt of photocopied Parts 2 and 5 from the receiving CEASO office:

-

Attach a copy of the transferring employee memorandum to Part 2 of Form 2276 and maintain in the closed file;

-

Send Part 5 of Form 2276 to Service Center Accounting Operation;

-

Close ICS OI control.

-

-

Upon receipt the receiving CEASO office will:

-

Assign a CDR serial number,

-

Prepare a new Form 2276 for control purposes,

-

Send Part 3 of the new Form 2276 to the Service Center Accounting Operation,

-

Retain Part 2,

-

Send Part 4 to the collection employee,

-

Open a control on ICS using action code 184 no later than 7 calendar days of receipt of the transferred collateral,

-

Send photocopies of Parts 2 and 5 to the transferring CEASO office,

-

Monitor the RACS 135 Area Office Inventory listing to ensure that the item is included in the RACS inventory.

-

-

This section covers procedures for disposition of the collateral upon satisfaction of the liability or default.

-

IDRS issues a transcript (IMF and BMF) 4 cycles before expiration of the stay to CEASO when the module balance changes and a collateral stay is in effect.

If advised by Area Counsel that the. . . Then. . . liability has not been sustained in litigation, release the collateral. account will be abated, do not wait for the abatement to post before releasing the collateral. -

When the conditions for releasing the collateral security have been complied with or account shows a zero balance and after consulting with Area Counsel, CEASO will:

-

Input TC 525,

-

Complete items 12–15 on Form 2276, Parts 2 and 5,

-

Enter name in item 16 as the person releasing the collateral,

-

Note in item 11 "Remarks" of Parts 2 and 5 of Form 2276, to whom collateral was released and the date released,

-

File Part 2 of Form 2276 in the closed file,

-

Document ICS with actions taken and follow-up date.

-

Send Part 5 to Service Center Accounting Operation.

-

Above actions will be completed within 10 calendar days of Area Counsel concurrence that the conditions for releasing the collateral security have been complied with or account shows a zero balance.

-

-

No later than 10 calendar days of Area Counsel concurrence, CEASO will:

-

Prepare Pattern Letter P–299 in quadruplicate (see Exhibit 5.6.2-2) to notify the surety company that it is relieved of liability under the bond;

-

Associate copy of letter with case file and mail: —original with the surety bond to the surety company, —copy to the taxpayer;

-

Check appropriate blocks for item 20 of Parts 2 and 5 of Form 2276;

-

Return Part 5 to the Service Center Accounting Operation.

-

-

No later than 10 calendar days of Area Counsel concurrence, CEASO will:

-

Mail original and copy of release of the mortgage to the taxpayer with the mortgage and advise to record the release;

-

Check appropriate blocks for item 20 of Parts 2 and 5 of Form 2276;

-

Return Part 5 to the Service Center Accounting Operation.

-

-

IDRS issues a Notice of Disposition to CEASO and a balance due four cycles after the stay expires.

-

For all collaterals, except surety bond (see IRM 5.6.2.7.1), send Pattern Letter P–301 (Exhibit 5.6.2-4) default letter to the taxpayer within 10 calendar days of receipt of the IDRS Notice of Disposition. Establish a reasonable follow-up date to monitor for taxpayer response.

If in response to the letter. . . Then. . . payment received, follow procedures in IRM 5.6.2.7 for Accounts Satisfied. If no response to the letter, or. . . Then no later than 10 calendar days of follow-up date. . . Payment not received -

Complete items 12–15 on Form 2276 Parts 2 and 5.

-

Request input of TC 525.

-

Apply the collateral to the liability in accordance with the terms of the agreement.

-

Seek assistance from Area Counsel as needed.

-

Check "Other." in item 20 of Form 2276 after disposition and notate item 20 "Taxpayer failed to comply with the conditions of the agreement—Collateral deposited for application to taxpayer’s account."

-

Return Part 5 of Form 2276 to the Service Center Accounting Operation.

-

-

Send Pattern Letter P–300 (see Exhibit 5.6.2-3) to the surety, with a copy to the taxpayer within 10 calendar days of receipt of the IDRS Notice of Disposition. Establish a reasonable follow-up date to monitor for the surety or taxpayer response.

If. . . Then. . . the surety full pays the account process per IRM 5.6.2.7 the account is not fully satisfied seek assistance from Area Counsel to enforce against the bond no later than 10 calendar days of follow-up date. -

After disposition, complete items 20 and 21 of Form 2276.

-

Retain Part 2 of Form 2276 pending verification of the next monthly RACS 135 Area Office Inventory Summary Report then associate with closed file.

-

Send Part 5 to the Service Center Accounting Operation in the Accounting Control Package within 10 calendar days of disposition.

-

Resolve any discrepancies with the Service Center Accounting Operation.

-

In those instances when an estate defaults on the installment election, CEASO will be notified as described in IRM 5.5.8.5.2, Miscellaneous Documentation From Campus or Appeals.

-

Annually, CEASO must validate that the value of collateral securing the lien is equal to the outstanding IRC 6166 balance on the account. Procedures concerning evaluation of collateral are outlined in IRM 5.5.8.5.3, Monitoring Accounts During the Deferral Period.

-

See additonal policy guidance on bonds and collateral secured by CEASO for estate tax accounts in IRM IRM 5.6.1.3.3Estate Tax Bonds and Other Collateral.

-

The CEASO responsibilities for the maintenance and disposition of collateral pledged in international situations varies by the type of international taxation event. See IRM 5.6.1.10, International Collateral Agreements, for a discussion of the different international collateral agreements.

-

The CEASO FIRPTA Coordinator will establish an ICS control to follow-up for compliance with the agreement and to monitor the purchaser(s) filing its annual U.S. income tax return. The CEASO FIRPTA Coordinator will secure a signed copy from the applicant and forward it to Examination FIRPTA at the Philadelphia Campus for review of the FIRPTA transaction(s).

-

The Examination FIRPTA Unit will notify CEASO with the results of the review of the FIRPTA transaction(s).

-

If there is an outstanding liability, CEASO will issue an NFOI to Field Collection to pursue appropriate collection actions.

-

-

Once all of the FIRPTA transactions are properly reported and all tax paid, the CEASO FIRPTA Coordinator will return the collateral to the applicant via memorandum. Close out the ICS NFOI.

-

There are maintenance situations which will require some form of administrative CEASO action:

-

Proper termination of closing agreement,

-

Change in the issuing bank guaranteeing the LOC,

-

-

There are two situations in which CEASO will be required to enforce against the LOC:

-

IRS receives notice from bank that the LOC will be not be renewed at the expiration date,

-

Foreign insurer failure to honor the closing agreement.

-

-

When it becomes necessary to take enforcement action against the LOC, Chief Counsel will contact CEASO with a request for enforcement action and a detailed justification for such action.

-

Upon notification by Chief Counsel, CEASO will advise the QMS Unit of Technical Services in Baltimore, MD of the pending enforcement action providing the name, address, and EIN of the foreign insurance company along with the amount of the LOC.

-

The local CEASO will transmit the original LOC via overnight mail to the CEASO territory manager (TM).

-

The CEASO TM will contact the Collection Field function TM in the location where the bank is located and request a revenue officer (RO) collect the LOC.

-

The CEASO TM will prepare and sign a pro forma letter and Sight Draft for the RO to present to the bank. The pro forma letter, Sight Draft and original LOC will be mailed to the RO via overnight mail.

-

-

The RO will collect the LOC, apply the proceeds and mail copies of the check and posting voucher(s) to the original advisor.

-

Historically, it has been rare that a LOC has been liquidated. Nevertheless, there are a number of maintenance procedures that will require CEASO action. These actions include:

-

Examination requests for verification of IRC 953(d),

-

Taxpayer requests for release of LOC,

-

Taxpayer request for a reduction on the LOC,

-

Financial institution notification that LOC will not be renewed and will expire.

-

-

On occasion, Examination will request verification of IRC 953(d) elections as part of an ongoing examination. These requests should be handled via electronic mail and will be limited to:

-

The effective date of approved elections,

-

The determination and date of rejected elections or LOCs,

-

No record of election request.

-

-

Taxpayers can request a release of the LOC if they:

-

are in liquidation,

-

are merging with another company,

-

claim that they now meet the "Office/Assets Test,"

-

claim an U.S. affiliate can meet the "Office/Assets Test" for them. IRM 5.6.2.9.3.3

-

-

For taxpayers that are facing liquidation or merger, a detailed written statement requesting the release must be submitted by the taxpayer including a copy of the most recently filed income tax return.

-

Upon receipt of the request, CEASO will, within 10 calendar days, send a copy of the file (taxpayer's written request, closing agreement, election statement and income tax return) to Examination QMS in Jacksonville for review and concurrence. No LOCs will be released without Examination concurrence.

-

-

After Examination concurrence, return the LOC to the financial institution via certified mail. Include part 4 of Form 2276 for the financial institution to sign Item 17 and return to the IRS.

-

Prepare and send the appropriate letter to the taxpayer notifying them of the release of collateral.

-

The closing agreement sets forth procedures for the release of the LOC when a taxpayer can meet the "Office/Assets Test" or when an U.S. affiliate can meet the test for the taxpayer.

-

The LOC must remain in effect until a stamped copy of the amended election statement is returned to the taxpayer.

-

Process Form 2276 according to IRM 5.6.2.9.3.1.

-

-

On occasion a taxpayer will request a reduction in their letter of credit because of a decrease in gross income.

-

Requests should be referred to Examination for concurrence.

-

Upon Examination’s concurrence, notify the taxpayer to submit an amended LOC in the new amount.

-

Process Form 2276 accordingly.

-

On occasion, an issuing financial institution will notify the IRS that a LOC will not be renewed and will expire on a specific date.

-

The financial institution is required to notify the IRS at least 180 days prior to the state expiration date.

-

If the notification is timely, mail the appropriate letter to the taxpayer requiring a replacement LOC or risk termination of the election. The closing agreement requires the taxpayer to submit a replacement LOC 60 days prior to the lapse or termination of the existing LOC.

-

If the replacement LOC is not submitted, forward a referral to Examination to address any examination potential that would allow the IRS to draw on the LOC to satisfy any tax liability established by Examination.

-

-

If the LOC is not renewed or replaced, and CEASO is advised that there is no examination potential, CEASO will, within 10 calendar days:

-

Retrieve the LOC from the safe,

-

Return it to the issuing financial institution including part 4 of Form 2276,

-

Mail the appropriate letter to the taxpayer notifying them of the termination of the election.

-

-

On an annual basis a compliance check should be conducted on all IRC 953(d) entities who are subjects of closing agreements involving LOC. The check should ensure that all returns have been filed and paid. The compliance review should closely follow the due date(s) for all filing requirements.

-

If there are compliance issues, the appropriate letter should be mailed to the taxpayer addressing the compliance issue and advising them of the risk of termination of the election.

-

The latest filed return should be reviewed (BRTVUE) to determine if there could have been an increase in gross income by more than 20% of the amount of gross income for the base year.

-

Such an increase would require the taxpayer to submit an amended or new letter of credit reflecting the new base year assets requirement (10 percent ). Because the gross income, as defined in IRC 803 or IRC 832(b)(1) cannot be determined from BRTVUE, the appropriate letter and Assets Calculation Worksheet should be mailed to the taxpayer to be completed and returned.

-

The closing agreement requires the taxpayer to monitor and calculate this amount on an annual basis however experience has shown that this is not always done and therefore the reminder letter is required. Failure to maintain a LOC at the proper level is grounds for termination of the election.

-

-

If the taxpayer does not resolve any issues with the terms and conditions of the closing agreement, a letter will be sent to the taxpayer detailing the corrections that need to be made, providing a specific date for response and explaining that the consequence will be termination of the election and potential Examination action. If the corrections are not made, make a referral to Examination to review for examination potential and concurrence in the termination of the election.

-

If Examination concurs with the termination, send a memorandum to Chief Counsel, International for final concurrence. Include a draft copy of the termination letter for Counsel review.

-

Once Chief Counsel concurrence is received, send the termination letter to the taxpayer. Process the LOC and Form 2276 accordingly.

-

At any time that it appears that the value of the collateral will not remain sufficient to secure the deferral of tax, accruing interest and any penalty additions, the covered expatriate will have 60 days to increase the amount of collateral security. Notification will be made via Letter 4537, Collateral Becomes Insufficient.

-

At the expiration of three years, or upon the death of the taxpayer executing the tax deferral agreement, and after notification via Letter 4538, Termination of Deferral Agreement, this tax deferral agreement will be terminated and the deferred tax and interest will be immediately due, unless:

-

The covered expatriate, or their U.S. Agent, certifies in writing, prior to the expiration of the current agreement, that none of the property or properties that are the subject of the tax deferral agreement have been disposed of by sale, gift, disposal in a transaction in which gain is not recognized in whole or in part, or by the death of the covered expatriate.

-

If the covered expatriate so certifies, this tax deferral agreement will be renewed and remain in effect for another three years from the date of certification. The covered expatriate may continue to renew the tax deferral agreement every three years. Renewal is contingent upon the covered expatriate increasing the value of the collateral security as described above in (1).

-

-

If the tax deferral agreement is not renewed within the time frame specified in the tax deferral agreement, the collateral will be applied to the tax liability and interest.

| [AREA DIRECTOR LETTERHEAD] | ||

| Name and Address of Principal: | ||

| Name of IRS Contact: | ||

| Contact Telephone Number: | ||

| [Name and address of surety] | ||

| [Salutation] | ||

| Our records show the principal named above has complied with the conditions under which a surety bond in the amount of $[amount] was executed by you, as surety, and by the principal under Internal Revenue Code section [number]. You are therefore released from liability under this bond. | ||

| We are sending the principal a copy of this letter. | ||

| If you have any questions, please contact the Internal Revenue Service representative whose name and telephone number are shown above. | ||

| Sincerely yours, | ||

| Area Director | ||

| cc: [Name of Taxpayer] | ||

| [AREA DIRECTOR LETTERHEAD] | ||

| Name and Address of Principal: | ||

| Name of IRS Contact: | ||

| Contact Telephone Number: | ||

| [Name and address of surety] | ||

| [Salutation] | ||

| Our records show the principal named above has not paid the tax liability for which the surety bond in the amount of $[amount] was executed by you, as surety, and by the principal under Internal Revenue Code section [number]. The liability should have been paid in full not later than [date]. Consequently, we must ask you to make payment as provided by the terms of the bond agreement. | ||

| We will appreciate your early response. If you have any questions, please contact the Internal Revenue Service representative whose name and telephone number are shown above. | ||

| Thank you for your cooperation. | ||

| Sincerely yours, | ||

| Area Director | ||

| cc: [Name of Taxpayer] | ||

| [AREA DIRECTOR LETTERHEAD] | ||

| Taxpayer Identifying Number: | ||

| Name of IRS Contact: | ||

| Contact Telephone Number: | ||

| [Name and address of taxpayer] | ||

| [Space for Salutation] | ||

| Our records show you have not complied with the conditions of the agreement you executed for payment of Federal taxes. The following items were pledged as security. | ||

| Description: | ||

| We must now ask you to pay the amount due within 10 days from the date of this letter. Otherwise, the above items will be disposed of under the terms of the agreement. | ||

| If you have any questions, please contact the Internal Revenue Service representative whose name and telephone number are shown above. | ||

| Sincerely yours, | ||

| [Space for signature] | ||

| Area Director | ||