)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

- HIGHLIGHTS OF THIS ISSUE

- Part I

- Part III

- 2023 Marginal Production Rates

- Credit for Renewable Electricity Production and Publication of Inflation Adjustment Factor and Reference Price for Calendar Year 2023

- Part IV

- Deletions From Cumulative List of Organizations, Contributions to Which are Deductible Under Section 170 of the Code

- Deletions From Cumulative List of Organizations, Contributions to Which are Deductible Under Section 170 of the Code

- Notice of Proposed Rulemaking

- Definition of Terms

- Numerical Finding List1

- Finding List of Current Actions on Previously Published Items1

- How to get the Internal Revenue Bulletin

Internal Revenue Bulletin: 2023-30

July 24, 2023

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

These proposed regulations set forth rules specifying the methodology for constructing the corporate bond yield curve that is used to derive the interest rates used in calculating present value and making other calculations under a defined benefit plan, as well as for discounting unpaid losses and estimated salvage recoverable of insurance companies. These regulations affect participants in, beneficiaries of, employers maintaining, and administrators of certain retirement plans, as well as insurance companies.

The purposes of this announcement are to announce that: (1) taxpayers will not be required to report the new excise tax imposed by section 4501 of the Internal Revenue Code on repurchases of corporate stock during a covered corporation’s taxable year (stock repurchase excise tax) on any returns filed with the IRS, or to make any payments of such tax, before the time specified in forthcoming regulations; (2) there will be no addition to tax under section 6651(a) of the Internal Revenue Code (or any other provision of the Internal Revenue Code) for failure to file a return reporting the stock repurchase excise tax, or for failure to pay the stock repurchase excise tax, before the time specified in the forthcoming regulations; and (3) the forthcoming regulations will require covered corporations to keep complete and detailed records to establish accurately any amount of stock repurchases (including repurchases made after December 31, 2022, but before the forthcoming regulations are published) and to retain these records as long as their contents may become material.

Revocation of IRC 501(c) (3) Organizations for failure to meet the code section requirements Contributions made to the Organizations by individual donors are no longer deductible under IRC 170 (b)(1)(A)

In response to the end of the Coronavirus Disease 2019 (COVID-19) public health emergency and the National Emergency Concerning the Novel Coronavirus Disease 2019 Pandemic, this notice modifies prior guidance regarding benefits relating to testing for and treatment of COVID-19 that can be provided by a health plan that otherwise satisfies the requirements to be a high deductible health plan under section 223(c)(2)(A). Specifically, this notice provides that the relief described in Notice 2020-15, 2020-14 IRB 559, applies only with respect to plan years ending on or before December 31, 2024. This notice also clarifies whether certain items and services are treated as preventive care under section 223(c)(2)(C). Specifically, this notice clarifies that the preventive care safe harbor, as described in Notice 2004-23, 2004-15 IRB 725, does not include screening (i.e., testing) for COVID-19, effective as of the date of publication of this notice. This notice also provides that items and services recommended with an “A” or “B” rating by the United States Preventive Services Task Force on or after March 23, 2010, are treated as preventive care for purposes of section 223(c)(2)(C), regardless of whether these items and services must be covered, without cost sharing, under Public Health Service Act section 2713.

This notice announces that under § 613A(c)(6)(C) of the Internal Revenue Code, the applicable percentage for purposes of determining percentage depletion on marginal properties for calendar year 2023 is 15 percent. The format of the notice is identical to the format of notices previously published on this issue.

This notice publishes the inflation adjustment factor and reference price for calendar year 2023 for the renewable electricity production credit under section 45 of the Internal Revenue Code. The 2023 inflation adjustment factor and reference price are used in determining the availability of the credit and apply to calendar year 2023 sales of kilowatt hours of electricity produced in the United States or a possession thereof from qualified energy resources. This notice also provides the credit amounts for calendar year 2023 under section 45.

This document contains final regulations that finalize, in part, proposed regulations issued on Oct. 9, 2019. The proposed regulations were published to facilitate an orderly transition in connection with the discontinuation of London interbank offer rates (LIBOR) and other IBORs. One issue addressed by those proposed regulations was to propose an alternative interest rate (specifically, yearly average Secured Overnight Financing Rate (SOFR)) for the election provided by § 1.882-5(d)(5)(ii)(B) (the published rate election). Generally, § 1.882-5 provides rules for determining the amount of a foreign corporation’s interest expense that is allocable to its income effectively connected with the conduct of a U.S. trade or business. The published rate election permits a foreign bank to elect to use the 30-day USD LIBOR rate to compute the interest expense attributable to its excess U.S.-connected liabilities. A comment to the proposed regulations asserted that SOFR was not an appropriate replacement for 30-day USD LIBOR and recommended that finalization be delayed until a suitable replacement could be identified. In July 2022, a comment recommended using the average published one-month Term SOFR plus a static spread adjustment of 0.11448%. This final regulation adopts that recommendation.

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1

Additional Guidance on the Transition from Interbank Offer Rates to Other Reference Rates with Respect to the Interest Rates of a Foreign Bank

AGENCY: Internal Revenue Service (IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document contains additional final regulations that provide guidance on the transition away from the use of interbank offer rates (“IBORs”) to other reference rates. Specifically, this regulation provides the replacement rate for the IBOR presently used in the published rate election, which may be used by taxpayers to determine the amount of interest expense attributable to their excess U.S.-connected liabilities and allocable to income that is effectively connected with the conduct of a trade or business within the United States (“ECI”). The final regulations will affect foreign banks that have income that is ECI.

DATES: Effective date: This regulation is effective on June 30, 2023.

Applicability date: For dates of applicability, see § 1.882-5(f)(3).

FOR FURTHER INFORMATION CONTACT: D. Peter Merkel or Caleb W. Trimm, (202) 317-6938 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

This document contains final regulations that provide for the replacement of the 30-day IBOR rate presently referenced by § 1.882-5(d)(5)(ii)(B) with the Secured Overnight Financing Rate (“SOFR”) of the same tenor, plus a fixed spread adjustment.

The London Interbank Offered Rate (“LIBOR”) is an interest rate benchmark that was the dominant reference rate used in financial contracts, at one point serving as the benchmark for more than $200 trillion of contracts worldwide. On July 27, 2017, the Financial Conduct Authority, the United Kingdom regulator tasked with overseeing LIBOR, announced that publication of all currency and term variants of LIBOR, including the U.S. dollar LIBOR (“USD LIBOR”), may cease after the end of 2021. On March 5, 2021, the administrator of LIBOR, Intercontinental Exchange (ICE) Benchmark Association, announced that publication of the overnight, one-month, three-month, six-month, and 12-month USD LIBORs would cease following the LIBOR publication on June 30, 2023. The ICE Benchmark Association will continue to publish an unrepresentative synthetic USD LIBOR in one-month, three-month, and six-month tenors until September 30, 2024.1 Publication of all other currency and tenor variants of LIBOR (including the one-week and two-month USD LIBOR) ceased following the LIBOR publication on December 31, 2021.

The Alternative Reference Rate Committee (“ARRC”), whose ex officio members include the Board of Governors of the Federal Reserve System, the Department of the Treasury (“Treasury Department”), the Commodity Futures Trading Commission, and the Office of Financial Research, was convened by the Board of Governors of the Federal Reserve System and the Federal Reserve Bank of New York to identify alternative reference rates that would be both more robust than USD LIBOR and that would comply with standards such as the International Organization of Securities Commissions’ “Principles for Financial Benchmarks.” In 2017, the ARRC identified a SOFR-based rate as its recommended replacement for LIBOR.

In 2021, the ARRC recommended the forward-looking term SOFRs published by the Chicago Mercantile Exchange Group Benchmark Administration, Ltd. in one-month, three-month, and six-month tenors. The ARRC has also recommended static spread adjustments to each of those tenors to adjust for the fact that SOFRs are risk-free rates, while IBORs include an element of bank credit risk. The static spread adjustments are based on the historical median over a 5-year lookback period calculating the difference between USD LIBOR and compounded averages of SOFR, set on March 5, 2021.2 The recommended static spread adjustment for one-month SOFR is 0.11448%.

To support the transition away from USD LIBOR, the ARRC has published recommended fallback language for inclusion in the terms of certain cash products. Contracts governed by U.S. law that reference USD LIBOR but that do not have any (or that have inadequate) fallback provisions are generally required by the Adjustable Interest Rate Act (“LIBOR Act”), Pub. L. 117-103, div. U, to use the SOFR of the same tenor, plus a static spread adjustment. The static spread adjustments to SOFR for each USD tenor required by the LIBOR Act are the same as those recommended by the ARRC.

The transition from IBORs to SOFRs or other reference rates may give rise to various tax issues. To minimize market disruption and facilitate an orderly transition in connection with the discontinuation of LIBOR and other IBORs, the Treasury Department and IRS published proposed regulations (REG-118784-18) in the Federal Register (84 FR 54068) on October 9, 2019 (“2019 Proposed Regulations”).

One issue addressed by the 2019 Proposed Regulations was the election provided by § 1.882-5(d)(5)(ii)(B). A foreign corporation that has a U.S. branch or other trade or business within the United States applies § 1.882-5 to determine its interest expense allocable under section 882(c) to its ECI. If a foreign corporation uses the method described in § 1.882-5(b) through (d), that foreign corporation could have liabilities attributable to its U.S. branch (U.S.-connected liabilities) that exceed its U.S.-booked liabilities (excess U.S.-connected liabilities). When a foreign corporation has excess U.S.-connected liabilities, § 1.882-5(d)(5)(ii)(A) entitles the foreign corporation to increase its interest expense allocable to its ECI in an amount determined by reference to the average U.S.-dollar borrowing cost on all U.S.-dollar liabilities other than its U.S.-booked liabilities. If the foreign corporation is a bank, it may elect under § 1.882-5(d)(5)(ii)(B) to use a published average 30-day LIBOR for the year rather than the actual rate computed under § 1.882-5(d)(5)(ii)(A). Because use of that election will no longer be possible when LIBOR is phased out, the 2019 Proposed Regulations included a proposal to replace 30-day USD LIBOR referenced in § 1.882-5(d)(5)(ii)(B) with a yearly average SOFR. Because SOFR is an overnight risk-free rate, the Treasury Department and the IRS acknowledged that the yearly average SOFR was likely to result in a lower rate than the 30-day LIBOR calculation previously allowed under § 1.882-5(d)(5)(ii)(B) and requested comments on whether another rate might be more appropriate.

Following publication of the 2019 Proposed Regulations, the Treasury Department and the IRS received one comment regarding the proposal to use yearly average SOFR in place of 30-day USD LIBOR for the election available under § 1.882-5(d)(5)(ii)(B). The comment noted two key differences between 30-day LIBOR and the yearly average SOFR, which the commenter stated made the yearly average SOFR an inappropriate substitute for 30-day LIBOR. First, SOFR is a risk-free rate, while LIBOR is an unsecured rate. Second, SOFR is an overnight rate, while the 30-day LIBOR is a one-month rate. The comment noted that SOFR removes the credit risk premium and term liquidity premium from the cost of borrowing as compared to 30-day LIBOR. The comment, however, did not identify a more reasonable substitute for 30-day LIBOR at that time and recommended that the Treasury Department and the IRS defer finalizing the proposed rule under § 1.882-5(d)(5)(ii)(B) because a yearly average SOFR calculation was not a reasonable replacement rate for 30-day USD LIBOR.

On January 4, 2022, the Treasury Department and the IRS published final regulations (TD 9961) in the Federal Register (87 FR 166) relating to the transition from IBORs to other reference rates (“2022 Final Regulations”). The 2022 Final Regulations did not finalize the proposed change to § 1.882-5(d)(5)(ii)(B). Instead, the Treasury Department and the IRS sought additional comments regarding the appropriate replacement rate for 30-day USD LIBOR for the purpose of the election under § 1.882-5(d)(5)(ii)(B).

Following the publication of the 2022 Final Regulations, the Treasury Department and the IRS received one additional comment regarding the appropriate replacement rate for the 30-day USD LIBOR rate referenced by § 1.882-5(d)(5)(ii)(B).

This comment is available for public inspection at https://www.regulations.gov or upon request. No public hearing was requested, and none was held. After consideration of the comments, the Treasury Department and the IRS adopt the 2019 Proposed Regulation as amended by this Treasury decision (“final regulations”).

In response to the request for additional comments in TD 9961, one comment was received relating to the 30-day USD LIBOR replacement in § 1.882-5(d)(5)(ii)(B). The comment made three recommendations for the final regulations under § 1.882-5(d)(5)(ii)(B).

A. One-Month Term SOFR Plus a Static Spread Adjustment

First, the comment recommended finalizing the regulation using the one-month term SOFR plus static spread adjustment of 0.11448% as recommended by the ARRC (which endorsed Term SOFR rates in June of 2021 and spread adjustments in October of 2021) and codified in the LIBOR Act (enacted in December of 2021). The comment noted that the one-month term SOFR plus a fixed spread adjustment accounts for some of the differences between SOFR and LIBOR rates and implied that one-month term SOFR plus static spread adjustment of 0.11448% is a more appropriate replacement than yearly average SOFR. The published rate election provides eligible taxpayers with administrative relief from the burden of calculating their actual borrowing rate, which is based on data maintained outside the United States.

The final regulations adopt this recommendation. The ARRC, whose ex officio members include the Treasury Department, has generally recommended that contracts referencing USD LIBOR adopt fallback provisions that reference the term SOFR of the same tenor, plus a static spread adjustment. The Treasury Department has supported the recommendations of the ARRC in prior guidance issued in Revenue Procedure 2020–44, 2020–45 I.R.B. 991 and the 2022 Final Regulations. In addition, contracts governed by U.S. law that have not voluntarily adopted such fallback provisions are generally required by the LIBOR Act to use the SOFR of the same tenor, plus the ARRC-recommended static spread adjustment, as a matter of law. Pub. L. 117-103, div. U. Accordingly, both the Treasury Department and the U.S. Congress have endorsed, or required, the use of a term SOFR of the same tenor, plus the ARRC-recommended static spread adjustment, as a replacement for term USD LIBORs. Because the published rate election available under § 1.882-5(d)(5)(ii)(B) references 30-day LIBOR, the one-month term SOFR (plus static spread adjustment) is the most appropriate replacement rate.

B. Alternative Method Approximating Actual Rate

The comment also recommended that the final regulations allow taxpayers to use a rate that reasonably approximates the bank’s actual rate and that is consistently applied from year to year. This recommendation is based on the approach taken in regulations that were in effect from 1981 through 1996. TD 7749, 46 FR 1681 (Jan. 7, 1981) (codified at former § 1.882-5(b)(3)(i)(B)). This historical regulation provided that, if information needed to calculate the taxpayer’s actual interest rate could not be reasonably obtained, then the taxpayer could determine its interest rate by applying any method that reasonably approximated its actual interest rate and that was consistently applied year over year, including, for example, approximating its interest rate by reference to 30-day LIBOR. Id. at 1684-85. The comment expressed concern that the one-month term SOFR plus static spread adjustment may be less than the actual cost of borrowing; however, for some taxpayers it may not be worthwhile or possible for the corporation to calculate its actual borrowing rate.

The final regulations do not adopt this recommendation. An approach based on a reasonable approximation of a taxpayer’s actual interest would establish a different method for determining a taxpayer’s borrowing rate that does not provide the certainty, accuracy, and simplicity of a published rate election. Additionally, the IRS would face significant challenges in administering such a rule. For example, the comment did not suggest any standard by which the IRS might determine whether a taxpayer’s method is a reasonable approximation of its actual borrowing rate.

Finally, data from recent filing years indicates that the actual rate calculation is not a significant burden to taxpayers. For taxable years 2020 and 2021 (the most recent years for which data is available), a majority of foreign banks with excess U.S.-connected liabilities chose to calculate their actual rate rather than use the published rate election. In both years, approximately 80% of such taxpayers opted to calculate their actual rate, while less than 20% chose to use the published rate election available under § 1.882-5(d)(5)(ii)(B).

C. Mechanism for Endorsing Additional Replacement Rates

Finally, the comment recommended that the final regulations include a mechanism for identifying additional qualified alternative reference rates via Internal Revenue Bulletin, Revenue Procedure, or another similar notice. The final regulations do not adopt this recommendation. The Treasury Department and the IRS do not anticipate a need to name additional alternative reference rates, and, if the need does arise in the future, the Treasury Department and the IRS may prefer to propose any new alternative reference rate through the regulatory process.

If a taxpayer failed to file a timely return or incorrectly determined that it did not have excess U.S.-connected liabilities, § 1.882-5(d)(5)(ii)(B) allowed the Director of Field Operations to calculate the taxpayer’s interest expense with respect to excess U.S.-connected liabilities using either the taxpayer’s actual rate or the published rate provided by § 1.882-5(d)(5)(ii)(B). The final regulations amend this rule to require the Director of Field Operations to use the published rate in order to reduce the administrative burden of calculating the actual rate for both the IRS and taxpayers.

For a taxable year that begins before and ends after the USD LIBOR cessation date of June 30, 2023, a taxpayer that makes the published rate election available under § 1.882-5(d)(5)(ii)(B) must calculate a blended published rate average for the taxable year which uses the 30-day USD LIBOR for the portion of its taxable year ending on June 30, 2023, and the one-month Term SOFR, plus static spread adjustment, for the portion of its taxable year beginning on July 1, 2023.

Pursuant to the Memorandum of Agreement, Review of Treasury Regulations under Executive Order 12866 (June 9, 2023), tax regulatory actions issued by the IRS are not subject to the requirements of section 6 of Executive Order 12866, as amended. Therefore, a regulatory impact assessment is not required.

The final regulations affect any foreign bank that has ECI and that has excess U.S.-connected liabilities, but which cannot reasonably calculate its actual borrowing rate. The number of small entities potentially affected by the final regulations is unknown; however, it is unlikely to be a substantial number because the final regulations only affect foreign banks that operate in the United States. In addition, data collected from Forms 1120-F, Schedule I filed in recent taxable years indicates that fewer than 100 total taxpayers are foreign banks with both ECI and excess U.S-connected liabilities. The data from Forms 1120-F, Schedule I shows that the number of foreign banks that elected to use the 30-day USD LIBOR rate to compute the interest expense attributable to their excess U.S.-connected liabilities varied from year to year. In some years, as many as 50 foreign banks made the election on Schedule I to use the 30-day USD LIBOR rate; in other years, fewer than ten taxpayers made that election. The Secretary has determined that the economic impact on any small entities affected by the final regulations is not significant.

The final regulations provide that the annual published rate election available under § 1.882-5(d)(5)(ii)(B) will be modified by substituting the one-month term SOFR, plus a static spread adjustment, for 30-day USD LIBOR. The rule does not require taxpayers to collect additional information to determine whether the taxpayer is eligible for the election. Additionally, the rule does not impose any new costs on taxpayers because it only replaces the published rate used for the purpose of the election and does not affect a taxpayer’s obligation with respect to the information to be gathered and reported.

In accordance with the Regulatory Flexibility Act (5 U.S.C. 601 et seq.) the Secretary hereby certifies that these final regulations will not have a significant economic impact on a substantial number of small entities.

Pursuant to section 7805(f), the proposed regulations (REG-118784-18) preceding these final regulations were submitted to the Chief Counsel for Advocacy of the Small Business Administration for comment on the impact on small business, and no comments were received.

Section 202 of the Unfunded Mandates Reform Act of 1995 requires that agencies assess anticipated costs and benefits and take certain other actions before issuing a final rule that includes any Federal mandate that may result in expenditures in any one year by a state, local, or tribal government, in the aggregate, or by the private sector, of $100 million in 1995 dollars, updated annually for inflation. This rule does not include any Federal mandate that may result in expenditures by state, local, or tribal governments, or by the private sector in excess of that threshold.

Executive Order 13132 (entitled “Federalism”) prohibits an agency from publishing any rule that has federalism implications if the rule either imposes substantial, direct compliance costs on state and local governments, and is not required by statute, or preempts state law, unless the agency meets the consultation and funding requirements of section 6 of the Executive order. This regulation does not have federalism implications and does not impose substantial direct compliance costs on state and local governments or preempt state law within the meaning of the Executive order.

IRS Notices and other guidance cited in this preamble are published in the Internal Revenue Bulletin (or Cumulative Bulletin) and are available from the Superintendent of Documents, U.S. Government Publishing Office, Washington, DC 20402, or by visiting the IRS website at https://www.irs.gov.

The principal authors of these regulations are D. Peter Merkel and Caleb W. Trimm of the Office of Associate Chief Counsel (International). However, other personnel from the IRS and Treasury Department participated in their development.

List of Subjects in 26 CFR Part 1

Income taxes, Reporting and recordkeeping requirements.

Adoption of Amendments to the Regulations

Accordingly, the Treasury Department and IRS amend 26 CFR part 1 as follows:

PART 1—INCOME TAXES

Paragraph 1. The authority citation for part 1 is amended by revising the entry for § 1.882-5 to read in part as follows:

Authority: 26 U.S.C. 7805 * * *

* * * * *

Section 1.882-5 also issued under 26 U.S.C. 882(c), 26 U.S.C. 864(e), 26 U.S.C. 988(d), and 26 U.S.C. 7701(l).

* * * * *

Par. 2. Section 1.882-5 is amended by revising the fourth sentence of paragraph (a)(7)(i) and paragraphs (d)(5)(ii)(B) and (f) to read as follows:

§ 1.882-5 Determination of interest deduction.

(a) * * *

(7) * * *

(i) * * * An elected method (other than the fair market value method under paragraph (b)(2)(ii) of this section, or the published rate election in paragraph (d)(5)(ii) of this section) must be used for a minimum period of five years before the taxpayer may elect a different method. * * *

* * * * *

(d) * * *

(5) * * *

(ii) * * *

(B) Annual published rate election—(1) In general. For each taxable year in which a taxpayer is a bank within the meaning of section 585(a)(2)(B) (without regard to the second sentence of section 585(a)(2)(B) or whether any such activities are effectively connected with a trade or business within the United States), the taxpayer may elect to compute the interest expense attributable to excess U.S.-connected liabilities by using the average published one-month Term Secured Overnight Financing Rate published by the Chicago Mercantile Exchange Group Benchmark Administration, Ltd. (or any successor administrator) (“Term SOFR”) for the taxable year, plus a static spread adjustment of 0.11448%, rather than the interest rate provided in paragraph (d)(5)(ii)(A) of this section. A taxpayer may elect to apply the rate provided in this paragraph (d)(5)(ii)(B) on an annual basis and does not require the consent of the Commissioner to change this election in a subsequent taxable year. If a taxpayer that is eligible to make the published rate election either does not file a timely return or files a calculation with no excess U.S.-connected liabilities and it is later determined by the Director of Field Operations that the taxpayer has excess U.S.-connected liabilities, then the Director of Field Operations will apply the interest rate provided under this paragraph (d)(5)(ii)(B) to the taxpayer’s excess U.S.-connected liabilities in determining interest expense.

(2) Transitional rule for taxable years including June 30, 2023. For a taxable year that includes June 30, 2023, a taxpayer that makes the annual published rate election must compute the interest expense attributable to excess U.S.-connected liabilities by ratably using the average 30-day U.S. dollar London Interbank Offered Rate for the portion of its taxable year ending on June 30, 2023, and the average one-month Term SOFR, plus a static spread adjustment of 0.11448%, for the portion of its taxable year beginning on July 1, 2023.

* * * * *

(f) Applicability date—(1) General rule. Except as provided in paragraph (f)(3) of this section, this section is applicable for tax years ending on or after August 15, 2009. A taxpayer, however, may choose to apply § 1.882-5T, rather than applying the regulations in this section, for any taxable year beginning on or after August 16, 2008, but before August 15, 2009.

(2) [Reserved]

(3) Applicability date for published rate election. Paragraphs (a)(7)(i) and (d)(5)(ii)(B) of this section apply to taxable years ending after June 30, 2023. For taxable years ending before July 1, 2023, see § 1.882-5(d)(5)(ii)(B) (as contained in 26 CFR part 1, revised as of April 1, 2023).

Douglas W. O’Donnell,

Deputy Commissioner for Services and Enforcement.

Approved: June 19, 2023.

Lily Batchelder,

Assistant Secretary of the Treasury (Tax Policy).

(Filed by the Office of the Federal Register June 29, 2023, 8:45 a.m., and published in the issue of the Federal Register for June 30, 2023, 88 FR 42231)

1 The synthetic USD LIBOR will be the Term SOFR of the same tenor (published by the Chicago Mercantile Exchange Group Benchmark Administration, Ltd.), plus a fixed spread adjustment of 0.11448%, 0.26161%, or 0.42826% for the one-, three-, and six-month tenors, respectively. Financial Conduct Authority, Article 23D Benchmarks Regulation Draft Notice of Requirements (April 3, 2023), https://www.fca.org.uk/publication/libor-notices/article-23d-benchmarks-regulation-usd-draft-notice-requirements.pdf. This rate is not considered representative because it uses a synthetic methodology to determine rates instead of the panel bank methodology that has historically been used to determine IBORs.

2 For an explanation of the SOFR averaging calculation, see Federal Reserve Bank of New York, Additional Information About the Reference Rates Administered by the New York Fed, https://www.newyorkfed.org/markets/reference-rates/additional-information-about-reference-rates.

In response to the end of the Coronavirus Disease 2019 (COVID-19) public health emergency (referred to in this document as the PHE) and the National Emergency Concerning the Novel Coronavirus Disease 2019 Pandemic1 (referred to in this document as the COVID-19 National Emergency), this notice modifies prior guidance regarding benefits relating to testing for and treatment of COVID-19 that can be provided by a health plan that otherwise satisfies the requirements to be a high deductible health plan (HDHP) under section 223(c)(2)(A) of the Internal Revenue Code (Code). Specifically, this notice provides that the relief described in Notice 2020-15, 2020-14 IRB 559, applies only with respect to plan years ending on or before December 31, 2024.

This notice also clarifies whether certain items and services are treated as preventive care under section 223(c)(2)(C). Specifically, this notice clarifies that the preventive care safe harbor, as described in Notice 2004-23, 2004-15 IRB 725, does not include screening (i.e., testing) for COVID-19, effective as of the date of publication of this notice.2 This notice also provides that items and services recommended with an “A” or “B” rating by the United States Preventive Services Task Force (USPSTF) on or after March 23, 2010, are treated as preventive care for purposes of section 223(c)(2)(C), regardless of whether these items and services must be covered, without cost sharing, under Public Health Service Act3 (PHS Act) section 2713.

Section 223 of the Code permits eligible individuals to deduct contributions to Health Savings Accounts (HSAs).4 Among the requirements for an individual to qualify as an eligible individual under section 223(c)(1) is that the individual be covered under an HDHP and have no disqualifying health coverage. As defined in section 223(c)(2), an HDHP is a health plan that satisfies certain requirements, including requirements with respect to minimum deductibles and maximum out-of-pocket expenses.

Generally, under section 223(c)(2)(A), an HDHP is not permitted to provide benefits for any year until the minimum deductible for that year is satisfied. However, section 223(c)(2)(C) provides a safe harbor for the absence of a deductible for preventive care. Under section 223(c)(2)(C), “[a] plan shall not fail to be treated as a high deductible health plan by reason of failing to have a deductible for preventive care (within the meaning of section 1861 of the Social Security Act, except as otherwise provided by the Secretary).” Therefore, an HDHP may provide preventive care benefits without a deductible, or with a deductible below the minimum annual deductible otherwise required by section 223(c)(2)(A). To be a preventive care benefit as defined for purposes of section 223, the benefit must either be described as preventive care for purposes of section 1861 of the Social Security Act (SSA) or be determined to be preventive care in guidance issued by the Department of the Treasury (Treasury Department) and the Internal Revenue Service (IRS).5 Notice 2013-57, 2013-40 IRB 293, provides that a health plan will not fail to qualify as an HDHP under section 223(c)(2) merely because it provides without a deductible the preventive care health services required under section 2713 of the PHS Act to be covered without cost sharing by a group health plan or a health insurance issuer offering group or individual health insurance coverage.

In March 2020, the Treasury Department and the IRS issued Notice 2020-15. The notice provides that due to the unprecedented public health emergency posed by COVID-19, and the need to eliminate potential administrative and financial barriers to testing for and treatment of COVID-19, a health plan that otherwise satisfies the requirements to be an HDHP under section 223(c)(2)(A) will not fail to be an HDHP merely because the health plan provides benefits for medical care services and items purchased related to testing for and treatment of COVID-19 prior to the satisfaction of the applicable minimum deductible.6 As a result, individuals covered by such a plan will not fail to be eligible individuals under section 223(c)(1) merely because of the provision of those health benefits prior to the satisfaction of the applicable minimum deductible.

On January 31, 2020, the Secretary of Health and Human Services (HHS) declared that a nationwide PHE existed as of January 27, 2020, as a result of COVID-19.7 This declaration was continually renewed by the HHS Secretary, most recently effective February 11, 2023.8 On January 30 and February 9, 2023, respectively, the President and the HHS Secretary announced their intent to end the COVID-19 National Emergency and the PHE on May 11, 2023.9 On February 10, 2023, the Federal Emergency Management Agency gave notice in the Federal Register that the national emergency under the Stafford Act would end on May 11, 2023.10 On April 10, 2023, the President signed H.J. Res. 7 ending the national emergency under the National Emergencies Act on April 10, 2023.11

On March 29, 2023, the Departments of Labor, HHS, and the Treasury (the Departments) issued Frequently Asked Questions (FAQs) under the heading, FAQs About Families First Coronavirus Response Act, Coronavirus Aid, Relief, and Economic Security Act, and Health Insurance Portability and Accountability Act Implementation Part 58 (FAQs Part 58), which address changes in various rules as the result of the end of the COVID-19 National Emergency and the PHE.12 Question and Answer 8 of FAQs Part 58 states that, while Notice 2020-15 applies until further guidance is issued, the Treasury Department and the IRS are reviewing the appropriateness of continuing the relief in Notice 2020-15 given the anticipated end of the COVID-19 National Emergency and the PHE and anticipate issuing additional guidance in the near future.

The Treasury Department and the IRS have determined that, with the end of the COVID-19 National Emergency and the PHE, the relief described in Notice 2020-15 is no longer needed. Accordingly, this notice modifies Notice 2020-15 to provide that the relief described in Notice 2020-15 applies only with respect to plan years ending on or before December 31, 2024. For subsequent plan years, an HDHP is not permitted to provide health benefits associated with testing for and treatment of COVID-19 without a deductible, or with a deductible below the minimum deductible (for self-only or family coverage) for an HDHP, except as otherwise provided in this notice.

The Treasury Department and the IRS note that Notice 2004-23 provides that preventive care under section 223(c)(2)(C) includes, but is not limited to, screening services as specified in the Appendix to Notice 2004-23. However, preventive care does not generally include any service or benefit intended to treat an existing illness, injury, or condition. As part of the preventive care safe harbor, the Appendix to Notice 2004-23 includes Infectious Diseases Screening Services for the following infections: Bacteriuria, Chlamydial Infection, Gonorrhea, Hepatitis B Virus Infection, Hepatitis C, Human Immunodeficiency Virus (HIV) Infection, Syphilis, and Tuberculosis Infection. Screenings for common and episodic illnesses, such as the flu, are not included on the list. Accordingly, the Treasury Department and the IRS are of the view that COVID-19 differs from the types of infectious diseases included in the preventive care safe harbor as specified in Notice 2004-23, and this notice clarifies that the preventive care safe harbor as described in Notice 2004-23 does not include screening (i.e., testing) for COVID-19, effective as of the date of publication of this notice.

In addition, the Treasury Department and the IRS note that on April 13, 2023, the Departments issued FAQs entitled, FAQs About Affordable Care Act and Coronavirus Aid, Relief, and Economic Security Act Implementation Part 59 (FAQs Part 59), which provide initial guidance on how the decision in Braidwood Management Inc. v. Becerra13 affects the requirement to cover preventive services without cost sharing under PHS Act section 2713.14 Question and Answer 7 of FAQs Part 59 states that, until further guidance is issued, items and services recommended with an “A” or “B” rating by the USPSTF on or after March 23, 2010, will be treated as preventive care for purposes of section 223(c)(2)(C) of the Code, regardless of whether these items and services must be covered, without cost sharing, under PHS Act section 2713.

Consistent with the position taken in Question and Answer 7 of FAQs Part 59, this notice provides that items and services recommended with an “A” or “B” rating by the USPSTF on or after March 23, 2010, are treated as preventive care for purposes of section 223(c)(2)(C) of the Code, regardless of whether these items and services must be covered, without cost sharing, under PHS Act section 2713. Accordingly, if COVID-19 testing were to be recommended with an “A” or “B” rating by the USPSTF, then that testing would be treated as preventive care under section 223(c)(2)(C) of the Code, regardless of whether it must be covered, without cost sharing, under PHS Act section 2713.

The principal author of this notice is Jennifer Friedman of the Office of Associate Chief Counsel (Employee Benefits, Exempt Organizations, and Employment Taxes), though other Treasury Department and IRS officials participated in its development. For further information on the provisions of this notice, contact Jennifer Friedman at (202) 317-5500 (not a toll-free number).

1 On March 13, 2020, by Proclamation 9994 (85 FR 15337 (March 18, 2020)), the President declared a national emergency concerning the COVID-19 pandemic beginning March 1, 2020, under both the National Emergencies Act (Pub. L. 94-412, 90 Stat. 1255 (1976)) and the Robert T. Stafford Disaster Relief and Emergency Assistance Act (Pub. L. 93-288, 88 Stat. 143 (1974)) (the Stafford Act). The national emergency has since been extended, with the last announcement of continuation made by the President on February 10, 2023. See The White House, Notice on the Continuation of the National Emergency Concerning the Coronavirus Disease 2019 (COVID-19) Pandemic (Feb. 10, 2023), available at https://www.whitehouse.gov/briefing-room/presidential-actions/2023/02/10/notice-on-the-continuation-of-the-national-emergency-concerning-the-coronavirus-disease-2019-covid-19-pandemic-3/. Subsequently, the President signed H.J. Res. 7 (Pub. L. 118-3, 137 Stat. 6), ending the national emergency under the National Emergencies Act on April 10, 2023, and the Federal Emergency Management Agency gave notice in the Federal Register that the national emergency under the Stafford Act would end on May 11, 2023. See https://www.govinfo.gov/content/pkg/FR-2023-02-10/pdf/2023-02964.pdf.

2 Although the preventive care safe harbor does not include testing for COVID-19, an HDHP may continue to provide benefits related to testing for COVID-19 before satisfaction of the applicable minimum deductible for plan years ending on or before December 31, 2024, pursuant to this notice.

3 See Pub. L. 111-148, 124 Stat. 119 (March 23, 2010).

4 Tax-favored contributions may also be made on behalf of eligible individuals by their employers. See Q&A 19 of Notice 2004-2 (2004-2 IRB 269).

5 The determination of whether an item or service is preventive care for these purposes is unrelated to the determination of whether an amount paid for an item or service is medical care under section 213(d) of the Code as an amount paid for the prevention of disease. See Rev. Rul. 79-66 (1979-1 CB 114); Daniels v. Commissioner, 41 T.C. 324 (1963); and Stringham v. Commissioner, 12 T.C. 580 (1949), (acq. 1950-2 CB 4), aff’d per curiam, 183 F.2d 579 (6th Cir. 1950).

6 Notice 2020-15 permitted, but not did require, an HDHP to provide these health benefits prior to the satisfaction of the applicable minimum deductible.

7 See HHS Office of the Assistant Secretary for Preparedness and Response, Determination of the HHS Secretary that a Public Health Emergency Exists (Jan. 31, 2020), available at https://www.phe.gov/emergency/news/healthactions/phe/Pages/2019-nCoV.aspx.

8 See HHS Office of the Assistant Secretary for Preparedness and Response, Renewal of Determination That A Public Health Emergency Exists (Feb. 9, 2023), available at https://aspr.hhs.gov/legal/PHE/Pages/COVID19-9Feb2023.aspx.

9 See Executive Office of the President, Office of Management and Budget, Statement of Administration Policy: H.R. 382 and H.J. Res. 7 (Jan. 30, 2023), available at https://www.whitehouse.gov/wp-content/uploads/2023/01/SAP-H.R.-382-H.J.-Res.-7.pdf; Letter to U.S. Governors from HHS Secretary Xavier Becerra on renewing COVID-19 Public Health Emergency (PHE) (Feb. 9, 2023), available at https://www.hhs.gov/about/news/2023/02/09/letter-us-governors-hhs-secretary-xavier-becerra-renewing-covid-19-public-health-emergency.html; Executive Office of the President, Notice on the Continuation of the National Emergency Concerning the Coronavirus Disease 2019 (COVID-19) Pandemic (Feb. 10, 2023), available at https://www.whitehouse.gov/briefing-room/presidential-actions/2023/02/10/notice-on-the-continuation-of-the-national-emergency-concerning-the-coronavirus-disease-2019-covid-19-pandemic-3/.

10 See https://www.govinfo.gov/content/pkg/FR-2023-02-10/pdf/2023-02964.pdf.

11 The April 10, 2023, end of the national emergency under the National Emergencies Act did not change the anticipated end date of the PHE or the end date of the national emergency under the Stafford Act.

12 See https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/faqs/aca-part-58 and https://www.cms.gov/cciio/resources/fact-sheets-and-faqs/downloads/faqs-part-58.pdf. Question and Answer 5 of FAQs Part 58 states that the Treasury Department, the IRS, and the Department of Labor “anticipate that the Outbreak Period will end July 10, 2023 (60 days after the anticipated end of the COVID-19 National Emergency).” The Treasury Department and the IRS, in coordination with the Department of Labor, clarify that the Outbreak Period ends July 10, 2023, irrespective of the last day of the national emergency under the National Emergencies Act or the last day of the national emergency under the Stafford Act.

13 Civil Action No. 4:20-cv-00283-O (N.D. Tex. March 30, 2023). On May 15, 2023, the Fifth Circuit issued an administrative stay of the decision pending appeal, and the Fifth Circuit issued a further Order regarding the stay pending appeal on June 13, 2023.

14 See https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/faqs/aca-part-59 and https://www.cms.gov/files/document/faqs-part-59.pdf.

This notice announces the applicable percentage under § 613A of the Internal Revenue Code to be used in determining percentage depletion for marginal properties for the 2023 calendar year.

Section 613A(c)(6)(C) defines the term “applicable percentage” for purposes of determining percentage depletion for oil and gas produced from marginal properties. The applicable percentage is the percentage (not greater than 25 percent) equal to the sum of 15 percent, plus one percentage point for each whole dollar by which $20 exceeds the reference price (determined under § 45K(d)(2)(C)) for crude oil for the calendar year preceding the calendar year in which the taxable year begins. The reference price determined under § 45K(d)(2)(C) for the 2022 calendar year is $93.97.

The following table contains the applicable percentages for marginal production for taxable years beginning in calendar years 1991 through 2023.

Notice 2023-50 APPLICABLE PERCENTAGE FOR MARGINAL PRODUCTION

| Calendar Year | Applicable Percentage |

|---|---|

| 1991 | 15 percent |

| 1992 | 18 percent |

| 1993 | 19 percent |

| 1994 | 20 percent |

| 1995 | 21 percent |

| 1996 | 20 percent |

| 1997 | 16 percent |

| 1998 | 17 percent |

| 1999 | 24 percent |

| 2000 | 19 percent |

| 2001 | 15 percent |

| 2002 | 15 percent |

| 2003 | 15 percent |

| 2004 | 15 percent |

| 2005 | 15 percent |

| 2006 | 15 percent |

| 2007 | 15 percent |

| 2008 | 15 percent |

| 2009 | 15 percent |

| 2010 | 15 percent |

| 2011 | 15 percent |

| 2012 | 15 percent |

| 2013 | 15 percent |

| 2014 | 15 percent |

| 2015 | 15 percent |

| 2016 | 15 percent |

| 2017 | 15 percent |

| 2018 | 15 percent |

| 2019 | 15 percent |

| 2020 | 15 percent |

| 2021 | 15 percent |

| 2022 | 15 percent |

| 2023 | 15 percent |

The principal author of this notice is Elimelech Brander of the Office of Associate Chief Counsel (Passthroughs and Special Industries). For further information regarding this notice contact Mr. Brander at (202) 317-6853 (not a toll-free number).

This notice publishes the inflation adjustment factor and reference price for calendar year 2023 for the renewable electricity production credit under section 45 of the Internal Revenue Code (section 45 credit). The 2023 inflation adjustment factor and reference price are used in determining the availability of the credit and apply to calendar year 2023 sales of kilowatt hours of electricity produced in the United States or a possession thereof from qualified energy resources.

Section 45 was amended by section 13101 of Public Law 117-169, 136 Stat. 1818 (August 16, 2022), commonly known as the Inflation Reduction Act of 2022 (IRA). The IRA changed the manner in which the section 45 credit amounts are calculated for any qualified facility placed in service after December 31, 2021. The IRA also removed the one-half reduction of the credit amount under section 45(b)(4)(A) for qualified hydropower facilities and marine and hydrokinetic renewable energy facilities placed in service after December 31, 2022. In the case of any qualified facility placed in service before January 1, 2022, the section 45 credit amounts are determined under the calculation rules provided by the prior version of section 45.

As amended by the IRA, section 45(b)(6)(A) provides that, in the case of any qualified facility that satisfies the requirements of section 45(b)(6)(B), the credit amount determined under section 45(a) (determined after the application of section 45(b)(1) through (5) and without regard to section 45(b)(6)) is equal to such amount multiplied by 5. A qualified facility satisfies the requirements of section 45(b)(6)(B) if it is placed in service after December 31, 2021, and it is one of the following: (i) a facility with a maximum net output of less than 1 megawatt (as measured in alternating current); (ii) a facility the construction of which began prior to January 29, 2023, which is the date that is 60 days after the publication of the guidance with respect to the requirements of section 45(b)(7)(A) (prevailing wage requirements) and section 45(b)(8) (apprenticeship requirements);1 or (iii) a facility that satisfies the requirements of section 45(b)(7)(A) and (8). The IRA also added bonus credit amounts with respect to qualified facilities placed in service after December 31, 2022, that meet domestic content requirements under section 45(b)(9)2 or energy community requirements under section 45(b)(11).3

The IRA amended the phaseout of the section 45 credit for wind facilities under section 45(b)(5) such that it does not apply to facilities placed in service after December 31, 2021. The IRA also added a new phaseout of the section 45 credit under section 45(b)(10) in the case of qualified facilities placed in service after December 31, 2022, for taxpayers making an elective payment election under section 6417. The IRA also amended the credit amount reduction under section 45(b)(3) in the case of qualified facilities the construction of which began after August 16, 2022.

The IRA amended section 45(d)(4) to restore the section 45 credit for electricity produced in solar energy facilities in the case of qualified facilities placed in service after December 31, 2021, and the construction of which begins before January 1, 2025. Effective for facilities placed in service after December 31, 2022, the IRA amended the definition of marine and hydrokinetic renewable energy under section 45(c)(10) and the definition of a marine and hydrokinetic renewable energy facility under section 45(d)(11). The IRA extended certain deadlines in the definitions under section 45(d) for wind facilities, closed-loop biomass facilities, open-loop biomass facilities, geothermal facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic renewable energy facilities.

Section 45(a) provides that the renewable electricity production credit for any tax year is an amount equal to the product of the kilowatt hours of specified electricity produced by the taxpayer and sold to an unrelated person during the tax year multiplied by 1.5 cents (in the case of a qualified facility placed in service before January 1, 2022) or 0.3 cents (in the case of a qualified facility placed in service after December 31, 2021). This electricity must be produced from qualified energy resources and at a qualified facility during the 10-year period beginning on the date the facility was originally placed in service.

Section 45(b)(1) provides that the amount of the credit determined under section 45(a) is reduced by an amount which bears the same ratio to the amount of the credit as the amount by which the reference price for the calendar year in which the sale occurs exceeds 8 cents, bears to 3 cents. Under section 45(b)(2), the 1.5 cent (or 0.3 cent) amount in section 45(a) and the 8 cent amount in section 45(b)(1) are each adjusted by multiplying such amount by the inflation adjustment factor for the calendar year in which the sale occurs. In the case of any qualified facility placed in service before January 1, 2022, if any amount as increased under section 45(b)(2) is not a multiple of 0.1 cent, such amount is rounded to the nearest multiple of 0.1 cent. In the case of any qualified facility placed in service after December 31, 2021, if the 0.3 cent amount as increased under section 45(b)(2) is not a multiple of 0.05 cent, such amount is rounded to the nearest multiple of 0.05 cent.

In the case of electricity produced in open-loop biomass facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic renewable energy facilities, section 45(b)(4)(A) requires the amount in effect under section 45(a)(1) (determined before rounding as required by section 45(b)(2)) to be reduced by one-half. As amended by the IRA, the one-half reduction under section 45(b)(4)(A) no longer applies to qualified hydropower facilities and marine and hydrokinetic renewable energy facilities placed in service after December 31, 2022.

Section 45(b)(5) provides that in the case of any qualified wind facility placed in service before January 1, 2022, the amount of the credit determined under section 45(a) (determined after the application of section 45(b)(1), (2), and (3) and without regard to section 45(b)(5)) shall be reduced by (A) in the case of any facility the construction of which began after December 31, 2016, and before January 1, 2018, 20 percent, (B) in the case of any facility the construction of which began after December 31, 2017, and before January 1, 2019, 40 percent, (C) in the case of any facility the construction of which began after December 31, 2018, and before January 1, 2020, 60 percent, and (D) in the case of any facility the construction of which began after December 31, 2019, and before January 1, 2022, 40 percent.

Section 45(c)(1) defines qualified energy resources as wind, closed-loop biomass, open-loop biomass, geothermal energy, solar energy, small irrigation power,4 municipal solid waste, qualified hydropower production, and marine and hydrokinetic renewable energy.

Section 45(d)(1) defines a qualified facility using wind to produce electricity as any facility owned by the taxpayer that is originally placed in service after December 31, 1993, and the construction of which begins before January 1, 2025. See section 45(e)(7) for rules relating to the inapplicability of the credit to electricity sold to utilities under certain contracts.

Section 45(d)(2)(A) defines a qualified facility using closed-loop biomass to produce electricity as any facility owned by the taxpayer that is originally placed in service after December 31, 1992, and the construction of which begins before January 1, 2025, or owned by the taxpayer which before January 1, 2025, is originally placed in service and modified to use closed-loop biomass to co-fire with coal, with other biomass, or with both, but only if the modification is approved under the Biomass Power for Rural Development Programs or is part of a pilot project of the Commodity Credit Corporation as described in 65 FR 63052. For purposes of section 45(d)(2)(A)(ii), a facility shall be treated as modified before January 1, 2025, if the construction of such modification begins before such date. Section 45(d)(2)(C) provides that in the case of a qualified facility described in section 45(d)(2)(A)(ii), the 10-year period referred to in section 45(a) is treated as beginning no earlier than the date of the enactment of section 45(d)(2)(C)(i) (October 22, 2004), and if the owner of such facility is not the producer of the electricity, the person eligible for the credit allowable under section 45(a) is the lessee or the operator of such facility. A qualified facility using closed-loop biomass includes a new unit placed in service after the date of the enactment of section 45(d)(2)(B) (October 3, 2008) in connection with a qualified facility using closed-loop biomass, but only to the extent of the increased amount of electricity produced at the facility by reason of such new unit.

Section 45(d)(3)(A) defines a qualified facility using open-loop biomass to produce electricity as any facility owned by the taxpayer which in the case of a facility using agricultural livestock waste nutrients, is originally placed in service after the date of the enactment of section 45(d)(3)(A)(i)(I) (October 22, 2004) and the construction of which begins before January 1, 2025, and the nameplate capacity rating of which is not less than 150 kilowatts, and in the case of any other facility, the construction of which begins before January 1, 2025. In the case of any facility described in section 45(d)(3)(A), if the owner of such facility is not the producer of the electricity, section 45(d)(3)(C) provides that the person eligible for the credit allowable under section 45(a) is the lessee or the operator of such facility. A qualified facility using open-loop biomass includes a new unit placed in service after the date of the enactment of section 45(d)(3)(B) (October 3, 2008) in connection with a qualified facility using open-loop biomass, but only to the extent of the increased amount of electricity produced at the facility by reason of such new unit.

Section 45(d)(4) defines a qualified facility using geothermal energy to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(4) (October 22, 2004) and the construction of which begins before January 1, 2025. A qualified facility using geothermal energy does not include any property described in section 48(a)(3) the basis of which is taken into account by the taxpayer for purposes of determining the energy credit under section 48.

As amended by the IRA and effective for solar energy facilities placed in service after December 31, 2021, section 45(d)(4) also defines a qualified facility using solar energy to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(4) (October 22, 2004) and the construction of which begins before January 1, 2025. A qualified facility using solar energy does not include any property described in section 48(a)(3) the basis of which is taken into account by the taxpayer for purposes of determining the energy credit under section 48.

Section 45(d)(6) defines a qualified facility using gas derived from the biodegradation of municipal solid waste to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(6) (October 22, 2004) and the construction of which begins before January 1, 2025.

Section 45(d)(7) defines a qualified facility (other than a facility described in section 45(d)(6)) that uses municipal solid waste to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(7) (October 22, 2004) and the construction of which begins before January 1, 2025. A qualified facility using municipal solid waste includes a new unit placed in service in connection with a facility placed in service on or before the date of the enactment of section 45(d)(7), but only to the extent of the increased amount of electricity produced at the facility by reason of such new unit.

Section 45(d)(9) defines a qualified facility producing qualified hydroelectric production described in section 45(c)(8) as (i) any facility producing incremental hydropower production, but only to the extent of its incremental hydropower production attributable to efficiency improvements or additions to capacity described in section 45(c)(8)(B) placed in service after the date of the enactment of section 45(d)(9) (August 8, 2005) and before January 1, 2025, and (ii) any other facility placed in service after the date of the enactment of section 45(d)(9) (August 8, 2005) and the construction of which begins before January 1, 2025. Section 45(d)(9)(B) provides that, in the case of a qualified facility described in section 45(d)(9)(A), the 10-year period referred to in section 45(a) shall be treated as beginning on the date the efficiency improvements or additions to capacity are placed in service. Section 45(d)(9)(C) provides that for purposes of section 45(d)(9)(A)(i), an efficiency improvement or addition to capacity shall be treated as placed in service before January 1, 2025, if the construction of such improvement or addition begins before such date.

As amended by the IRA, section 45(d)(11) provides in the case of a facility producing electricity from marine and hydrokinetic renewable energy, the term “qualified facility” means any facility owned by the taxpayer which has a nameplate capacity rating of at least 150 kilowatts (or at least 25 kilowatts in the case of a facility placed in service after December 31, 2022), and is originally placed in service on or after the date of the enactment of section 45(d)(11) (October 3, 2008) and the construction of which begins before January 1, 2025.

Section 45(e)(2)(A) requires the Secretary to determine and publish in the Federal Register each calendar year the inflation adjustment factor and the reference price for such calendar year. The inflation adjustment factor and the reference price for the 2023 calendar year were published in the Federal Register at 88 FR 40400 on June 21, 2023.

Section 45(e)(2)(B) defines the inflation adjustment factor for a calendar year as a fraction the numerator of which is the GDP implicit price deflator for the preceding calendar year and the denominator of which is the GDP implicit price deflator for the calendar year 1992. The term “GDP implicit price deflator” means the most recent revision of the implicit price deflator for the gross domestic product as computed and published by the Department of Commerce before March 15 of the calendar year.

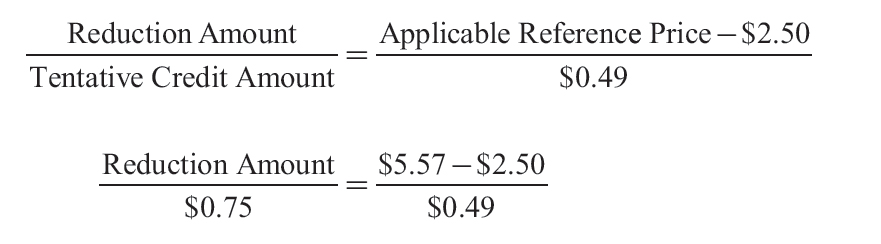

Section 45(e)(2)(C) provides that the reference price with respect to a calendar year is the Secretary’s determination of the annual average contract price per kilowatt hour of electricity generated from the same qualified energy resource and sold in the previous year in the United States. Only contracts entered into after December 31, 1989 are taken into account.

The inflation adjustment factor for calendar year 2023 for qualified energy resources is 1.8909.

The reference price for calendar year 2023 for facilities producing electricity from wind (based upon information provided by the Department of Energy) is 3.74 cents per kilowatt hour. The reference prices for facilities producing electricity from closed-loop biomass, open-loop biomass, geothermal energy, solar energy, municipal solid waste, qualified hydropower production, and marine and hydrokinetic energy have not been determined for calendar year 2023.

Because the 2023 reference price for electricity produced from wind (3.74 cents per kilowatt hour) does not exceed 8 cents multiplied by the inflation adjustment factor (1.8909), the phaseout of the credit provided in section 45(b)(1) does not apply to such electricity sold during calendar year 2023. However, section 45(b)(5) provides an additional phaseout of the credit for wind facilities placed in service before January 1, 2022, and the construction of which began after December 31, 2016. For electricity produced from closed-loop biomass, open-loop biomass, geothermal energy, solar energy, municipal solid waste, qualified hydropower production, and marine and hydrokinetic energy, the phaseout of the credit provided in section 45(b)(1) does not apply to such electricity sold during calendar year 2023.

As required by section 45(b)(2), the 1.5 cent amount provided in section 45(a)(1) is adjusted by multiplying such amount by the inflation adjustment factor for the calendar year in which the sale occurs. If any amount as increased under section 45(b)(2) is not a multiple of 0.1 cent, such amount is rounded to the nearest multiple of 0.1 cent. In the case of electricity produced in open-loop biomass facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic renewable energy facilities, section 45(b)(4)(A) requires the amount in effect under section 45(a)(1) (before rounding to the nearest 0.1 cent as required by section 45(b)(2)) to be reduced by one-half.

Under the calculation required by section 45(b)(2), the credit for renewable electricity production for calendar year 2023 determined under section 45(a) is 2.8 cents per kilowatt hour on the sale of electricity produced in any qualified facility placed in service before January 1, 2022, from the qualified energy resources of wind, closed-loop biomass, and geothermal energy, and 1.4 cents per kilowatt hour on the sale of electricity produced in any qualified facility placed in service before January 1, 2022, from the qualified energy resources of open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic energy.

As required by section 45(b)(2), the 0.3 cent amount provided in section 45(a)(1) is adjusted by multiplying such amount by the inflation adjustment factor for the calendar year in which the sale occurs. If the 0.3 cent amount as adjusted for inflation is not a multiple of 0.05 cent, the amount is rounded to the nearest multiple of 0.05 cent. In the case of electricity produced in open-loop biomass facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic renewable energy facilities, section 45(b)(4)(A) requires the amount in effect under section 45(a)(1) (determined before rounding as required by section 45(b)(2)) to be reduced by one-half.

Under the calculation required by section 45(b)(2), the credit for renewable electricity production for calendar year 2023 determined under section 45(a) is 0.55 cents per kilowatt hour on the sale of electricity produced in any qualified facility placed in service after December 31, 2021, from the qualified energy resources of wind, closed-loop biomass, geothermal energy, and solar energy, and 0.3 cents per kilowatt hour on the sale of electricity produced in any qualified facility placed in service after December 31, 2021, from the qualified energy resources of open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic renewable energy.

Under the calculation required by section 45(b)(2), the credit for renewable electricity production for calendar year 2023 determined under section 45(a) is 0.55 cents per kilowatt hour on the sale of electricity produced in any qualified facility placed in service after December 31, 2022, from the qualified energy resources of qualified hydropower and marine and hydrokinetic renewable energy.

The principal author of this notice is Charles Hyde of the Office of Associate Chief Counsel (Passthroughs & Special Industries). For further information regarding this notice contact Mr. Hyde at (202) 317-6853 (not a toll-free number).

1 See Notice 2022-61, 2022-52 I.R.B. 560 (Dec. 27, 2022), for additional information regarding the prevailing wage and apprenticeship requirements.

2 See Notice 2023-38, 2023-22 I.R.B. 872 (May 12, 2023), for additional information regarding the domestic content bonus credit.

3 See Notice 2023-45, 2023-29 I.R.B. 317 (July 17, 2023), for additional information regarding the energy community bonus credit.

4 The section 45 credit is expired for small irrigation power facilities.

This announcement confirms that no taxpayer is required to report the new excise tax imposed by section 4501 of the Internal Revenue Code (Code) on repurchases of corporate stock during a covered corporation’s taxable year (stock repurchase excise tax) on any returns filed with the Internal Revenue Service (IRS), or to make any payments of such tax, before the time specified in forthcoming regulations.

The stock repurchase excise tax applies to repurchases made after December 31, 2022. On January 17, 2023, the Department of the Treasury (Treasury Department) and the IRS published Notice 2023-2, 2023-3 I.R.B. 374, to provide initial guidance regarding the application of the stock repurchase excise tax. The notice announced that the Treasury Department and the IRS intend to issue forthcoming regulations addressing the application of the stock repurchase excise tax. The notice describes certain rules for determining the amount of stock repurchase excise tax owed that the Treasury Department and the IRS intend to include in the forthcoming regulations and provides that taxpayers may rely on these rules until the publication of the forthcoming regulations.

Additionally, the notice describes anticipated procedures for reporting and paying any liability for the stock repurchase excise tax that the Treasury Department and the IRS intend to include in the forthcoming regulations. Specifically, the notice states that the forthcoming regulations are expected to provide that (i) the stock repurchase excise tax will be reported once per taxable year on the Form 720, Quarterly Federal Excise Tax Return, that is due for the first full quarter after the close of the taxpayer’s taxable year, (ii) the deadline for payment of the stock repurchase excise tax will be the same as the filing deadline, and (iii) no extensions will be permitted for reporting or paying the stock repurchase excise tax.

For those taxpayers with a taxable year ending after December 31, 2022, but prior to publication of the forthcoming regulations, such regulations are expected to provide that any liability for the stock repurchase excise tax for such taxable year will be reported on the Form 720 that is due for the first full quarter after the date of publication of the forthcoming regulations, and that the deadline for payment of the stock repurchase excise tax is the same as the filing deadline. There will be no addition to tax under section 6651(a) of the Code (or any other provision of the Code) for failure to file a return reporting the stock repurchase excise tax, or for failure to pay the stock repurchase excise tax, before the time specified in the forthcoming regulations.

The Treasury Department and the IRS expect the forthcoming regulations will require covered corporations to keep complete and detailed records to establish accurately any amount of stock repurchases (including repurchases made after December 31, 2022, but before the forthcoming regulations are published) and to retain these records as long as their contents may become material.

The Internal Revenue Service has revoked its determination that the organizations listed below qualify as organizations described in sections 501(c)(3) and 170(c)(2) of the Internal Revenue Code of 1986.

Generally, the IRS will not disallow deductions for contributions made to a listed organization on or before the date of announcement in the Internal Revenue Bulletin that an organization no longer qualifies. However, the IRS is not precluded from disallowing a deduction for any contributions made after an organization ceases to qualify under section 170(c)(2) if the organization has not timely filed a suit for declaratory judgment under section 7428 and if the contributor (1) had knowledge of the revocation of the ruling or determination letter, (2) was aware that such revocation was imminent, or (3) was in part responsible for or was aware of the activities or omissions of the organization that brought about this revocation.

If on the other hand a suit for declaratory judgment has been timely filed, contributions from individuals and organizations described in section 170(c)(2) that are otherwise allowable will continue to be deductible. Protection under section 7428(c) would begin on July 24, 2023 and would end on the date the court first determines the organization is not described in section 170(c)(2) as more particularly set for in section 7428(c)(1). For individual contributors, the maximum deduction protected is $1,000, with a husband and wife treated as one contributor. This benefit is not extended to any individual, in whole or in part, for the acts or omissions of the organization that were the basis for revocation.

| NAME OF ORGANIZATION | Effective Date of Revocation | LOCATION |

|---|---|---|

| AMERICAN CANCER OF SOCIETY FLORIDA | 01/01/2018 | New York, NY |

| AMERICAN CANCER SOCIETY OF WASHINGTON | 01/01/2018 | New York, NY |

| AMERICAN CANCER SOCIETY OF MASSACHUSETTS | 01/01/2018 | New York NY |

| AMERICAN CANCER SOCIETY OF BALTIMORE | 01/01/2018 | New York, NY |

| AMERICAN CANCER SOCIETY OF CINNCINATI | 01/01/2018 | New York, NY |

| AMERICAN CANCER PF OF GEORGIA | 01/01/2018 | New York, NY |

| AMERICAN CANCER SOCIETY OF MARYLAND | 01/01/2018 | New York, NY |

| AMERICAN CANCER SOCIETY OF OHIO | 01/01/2018 | New York, NY |

| CHILDREN’S CANCER SOCIETY OF TEXAS | 01/01/2018 | New York, NY |

The Internal Revenue Service has revoked its determination that the organizations listed below qualify as organizations described in sections 501(c)(3) and 170(c)(2) of the Internal Revenue Code of 1986.

Generally, the IRS will not disallow deductions for contributions made to a listed organization on or before the date of announcement in the Internal Revenue Bulletin that an organization no longer qualifies. However, the IRS is not precluded from disallowing a deduction for any contributions made after an organization ceases to qualify under section 170(c)(2) if the organization has not timely filed a suit for declaratory judgment under section 7428 and if the contributor (1) had knowledge of the revocation of the ruling or determination letter, (2) was aware that such revocation was imminent, or (3) was in part responsible for or was aware of the activities or omissions of the organization that brought about this revocation.

If on the other hand a suit for declaratory judgment has been timely filed, contributions from individuals and organizations described in section 170(c)(2) that are otherwise allowable will continue to be deductible. Protection under section 7428(c) would begin on July 24, 2023 and would end on the date the court first determines the organization is not described in section 170(c)(2) as more particularly set for in section 7428(c)(1). For individual contributors, the maximum deduction protected is $1,000, with a husband and wife treated as one contributor. This benefit is not extended to any individual, in whole or in part, for the acts or omissions of the organization that were the basis for revocation.

| NAME OF ORGANIZATION | Effective Date of Revocation | LOCATION |

|---|---|---|

| AMERICAN CANCER SOCIETY OF GREEN BAY | 01/01/2021 | STATEN ISLAND, NY |

| AMERICAN CANCER SOCIETY OF DETROIT | 01/01/2021 | STATEN ISLAND, NY |

| AMERICAN CANCER SOCIETY FOR CHILDREN OF NEW YORK | 01/01/2021 | STATEN ISLAND, NY |

| COACHELLA VALLEY CHURCH | 01/01/2017 | SAN JOSE, CA |

| AMERICAN CANCER FDN OF BROOKLYN | 01/01/2021 | STATEN ISLAND, NY |

| AMERICAN CANCER FDN OF COLUMBUS INC. | 01/01/2021 | STATEN ISLAND, NY |