)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

- HIGHLIGHTS OF THIS ISSUE

- Part I

- Part III

- Reference Price for Section 45I Credit for Production of Natural Gas from Marginal Wells During Taxable Years Beginning in Calendar Year 2023

- Guidance on Requirements for Home Energy Audits for Purposes of the Energy Efficient Home Improvement Credit under Section 25C

- Part IV

- Notice of Proposed Rulemaking

- Definition of Terms

- Numerical Finding List1

- Finding List of Current Actions on Previously Published Items1

- How to get the Internal Revenue Bulletin

Internal Revenue Bulletin: 2023-34

August 21, 2023

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

The Office of Professional Responsibility (OPR) announces recent disciplinary sanctions involving attorneys, certified public accountants, enrolled agents, enrolled actuaries, enrolled retirement plan agents, and appraisers. These individuals are subject to the regulations governing practice before the Internal Revenue Service (IRS), which are set out in Title 31, Code of Federal Regulations, Part 10, and which are published in pamphlet form as Treasury Department Circular No. 230. The regulations prescribe the duties and restrictions relating to such practice and prescribe the disciplinary sanctions for violating the regulations.

The notice announces the inflation adjustment factor and phase-out amount for the enhanced oil recovery credit for taxable years beginning in the 2023 calendar year. The format of the notice is identical to the format of previously published notices on this issue. The notice concludes that because the reference price for the 2022 calendar year ($93.97) exceeds $28 multiplied by the inflation adjustment factor for the 2023 calendar year ($28 multiplied by 1.9998 = $55.99) by $37.98, the enhanced oil recovery credit for qualified costs paid or incurred in 2023 is phased-out completely.

The notice provides the applicable reference price for qualified natural gas production from qualified marginal wells during taxable years beginning in calendar year 2023 for the purpose of determining the marginal well production credit under § 45I. The applicable reference price for taxable years beginning in calendar year 2023 is $5.57 per 1,000 cubic feet. The notice also provides the credit amount used for the purpose of determining the marginal well production credit. The credit amount for taxable years beginning in calendar year 2023 is $0.00 per 1,000 cubic feet.

The notice announces forthcoming proposed regulations and provides interim guidance regarding Home Energy Audits for purposes of the § 25C energy efficient home improvement credit, as well as a transition rule for certain Home Energy Audits conducted during taxable years ending in calendar year 2023.

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

This revenue ruling contains a list of the average annual effective interest rates on new loans under the Farm Credit System. This revenue ruling also contains a list of the states within each Farm Credit System Bank Territory.

Under § 2032A(e)(7)(A)(ii) of the Internal Revenue Code, rates on new Farm Credit System Bank loans are used in computing the special use value of real property used as a farm for which an election is made under § 2032A. The rates in Table 1 of this revenue ruling may be used by estates that value farmland under § 2032A as of a date in 2023.

Average annual effective interest rates, calculated in accordance with § 2032A(e)(7)(A) and § 20.2032A-4(e) of the Estate Tax Regulations, to be used under § 2032A(e)(7)(A)(ii), are set forth in the accompanying Table of Interest Rates (Table 1). The states within each Farm Credit System Bank Territory are set forth in the accompanying Table of Farm Credit System Bank Territories (Table 2).

Rev. Rul. 81-170, 1981-1 C.B. 454, contains an illustrative computation of an average annual effective interest rate. The rates applicable for valuation in 2022 are in Rev. Rul. 2022-16, 2022-35 I.R.B. 171. For rate information for years prior to 2022, see Rev. Rul. 2021-15, 2021-35 I.R.B. 331, and other revenue rulings that are referenced therein.

The principal author of this revenue ruling is Lane Damazo of the Office of the Associate Chief Counsel (Passthroughs and Special Industries). For further information regarding this revenue ruling, contact Lane Damazo at (202) 317-4628 (not a toll-free number).

REV. RUL. 2023-15 TABLE 1

| TABLE OF INTEREST RATES (Year of Valuation 2023) | |

| Farm Credit System Bank Servicing State in Which Property is Located | Rate |

| AgFirst, FCB | 5.33 |

| AgriBank, FCB | 4.83 |

| CoBank, ACB | 4.83 |

| Texas, FCB | 5.22 |

REV. RUL. 2023-15 TABLE 2

| TABLE OF FARM CREDIT SYSTEM BANK TERRITORIES | |

| Farm Credit System Bank | Location of Property |

| AgFirst, FCB | Delaware, District of Columbia, Florida, Georgia, Maryland, North Carolina, Pennsylvania, South Carolina, Virginia, West Virginia. |

| AgriBank, FCB | Arkansas, Illinois, Indiana, Iowa, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Tennessee, Wisconsin, Wyoming. |

| CoBank, ACB | Alaska, Arizona, California, Colorado, Connecticut, Hawaii, Idaho, Kansas, Maine, Massachusetts, Montana, New Hampshire, New Jersey, New Mexico, New York, Nevada, Oklahoma, Oregon, Rhode Island, Utah, Vermont, Washington. |

| Texas, FCB | Alabama, Louisiana, Mississippi, Texas. |

Section 43(a) of the Internal Revenue Code provides that for purposes of section 38, the enhanced oil recovery credit for any taxable year is an amount equal to 15 percent of the taxpayer’s qualified enhanced oil recovery costs for such taxable year.

Section 43(b)(1) provides that the amount of the credit determined under subsection (a) for any taxable year shall be reduced by an amount which bears the same ratio to the amount of such credit (determined without regard to this paragraph) as — (A) the amount by which the reference price for the calendar year preceding the calendar year in which the taxable years begins exceeds $28, bears to (B) $6.

Section 43(b)(3)(B) requires the Secretary to publish an inflation adjustment factor. The enhanced oil recovery credit under § 43 for any taxable year is reduced if the “reference price,” determined under § 45K(d)(2)(C), for the calendar year preceding the calendar year in which the taxable year begins is greater than $28 multiplied by the inflation adjustment factor the current calendar year.

The term “inflation adjustment factor” means, with respect to any calendar year, a fraction the numerator of which is the GNP implicit price deflator for the preceding calendar year and the denominator of which is the GNP implicit price deflator for 1990.

Because the reference price for the 2022 calendar year ($93.97) exceeds $28 multiplied by the inflation adjustment factor for the 2023 calendar year ($28 multiplied by 1.9998 = $55.99) by $37.98, the enhanced oil recovery credit for qualified costs paid or incurred in 2023 is phased out completely.

Table 1 contains the GNP implicit price deflator used for the 2022 calendar year, as well as the previously published GNP implicit price deflators used for the 1991 through 2021 calendar years.

Notice 2023-57 TABLE 1 GNP IMPLICIT PRICE DEFLATORS

| Calendar Year | GNP Implicit Price Deflator |

|---|---|

| 1990 | 112.9 (used for 1991) |

| 1991 | 117.0 (used for 1992) |

| 1992 | 120.9 (used for 1993) |

| 1993 | 124.1 (used for 1994) |

| 1994 | 126.0 (used for 1995)* |

| 1995 | 107.5 (used for 1996) |

| 1996 | 109.7 (used for 1997)** |

| 1997 | 112.35 (used for 1998) |

| 1998 | 112.64 (used for 1999)*** |

| 1999 | 104.59 (used for 2000) |

| 2000 | 106.89 (used for 2001) |

| 2001 | 109.31 (used for 2002) |

| 2002 | 110.63 (used for 2003) |

| 2003 | 105.67 (used for 2004)**** |

| 2004 | 108.23 (used for 2005) |

| 2005 | 112.129 (used for 2006) |

| 2006 | 116.036 (used for 2007) |

| 2007 | 119.656 (used for 2008) |

| 2008 | 122.407 (used for 2009) |

| 2009 | 109.764 (used for 2010)***** |

| 2010 | 110.654 (used for 2011) |

| 2011 | 113.347 (used for 2012)****** |

| 2012 | 115.387 (used for 2013) |

| 2013 | 106.710 (used for 2014)******* |

| 2014 | 108.407 (used for 2015)******** |

| 2015 | 109.868 (used for 2016) |

| 2016 | 111.528 (used for 2017) |

| 2017 | 113.500 (used for 2018) |

| 2018 | 110.308 (used for 2019)********* |

| 2019 | 112.257 (used for 2020) |

| 2020 | 113.586 (used for 2021) |

| 2021 | 118.586 (used for 2022)********** |

| 2022 | 127.194 (used for 2023) |

* Beginning in 1995, the GNP implicit price deflator was rebased relative to 1992. The 1990 GNP implicit price deflator used to compute the 1996 § 43 inflation adjustment factor is 93.6.

** Beginning in 1997, two digits follow the decimal point in the GNP implicit price deflator. The 1990 GNP price deflator used to compute the 1998 § 43 inflation adjustment factor is 93.63.

*** Beginning in 1999, the GNP implicit price deflator was rebased relative to 1996. The 1990 GNP implicit price deflator used to compute the 2000 § 43 inflation adjustment factor is 86.53.

**** Beginning in 2003, the GNP implicit price deflator was rebased, and the 1990 GNP implicit price deflator used to compute the 2004 § 43 inflation adjustment factor is 81.589.

***** Beginning in 2009, the GNP implicit price deflator was rebased, and the 1990 GNP implicit price deflator used to compute the 2010 § 43 inflation adjustment factor is 72.199.

****** Beginning in 2011, the 1990 GNP implicit price deflator used to compute the 2012 § 43 inflation adjustment factor is 72.260.

******* Beginning in 2013, the GNP implicit price deflator was rebased, and the 1990 GNP implicit price deflator used to compute the 2014 § 43 inflation adjustment factor is 66.803.

******** Beginning in 2014, the 1990 GNP implicit price deflator used to compute the 2015 § 43 inflation adjustment factor is 66.732.

********* Beginning in 2018, the 1990 GNP implicit price deflator used to compute the 2019 § 43 inflation adjustment factor is 63.637.

********** Beginning in 2021, the 1990 GNP implicit price deflator used to compute the 2022 § 43 inflation adjustment factor is 63.604.

Table 2 contains the inflation adjustment factor and the phase-out amount for taxable years beginning in the 2023 calendar year as well as the previously published inflation adjustment factors and phase-out amounts for taxable years beginning in the 1991 through 2022 calendar years.

Notice 2023-57 TABLE 2 INFLATION ADJUSTMENT FACTORS AND PHASE-OUT AMOUNTS

| Calendar Year | Inflation Adjustment Factor | Phase-out Amount |

|---|---|---|

| 1991 | 1.0000 | 0 |

| 1992 | 1.0363 | 0 |

| 1993 | 1.0708 | 0 |

| 1994 | 1.0992 | 0 |

| 1995 | 1.1160 | 0 |

| 1996 | 1.1485 | 0 |

| 1997 | 1.1720 | 0 |

| 1998 | 1.1999 | 0 |

| 1999 | 1.2030 | 0 |

| 2000 | 1.2087 | 0 |

| 2001 | 1.2353 | 0 |

| 2002 | 1.2633 | 0 |

| 2003 | 1.2785 | 0 |

| 2004 | 1.2952 | 0 |

| 2005 | 1.3266 | 0 |

| 2006 | 1.3743 | 100 percent |

| 2007 | 1.4222 | 100 percent |

| 2008 | 1.4666 | 100 percent |

| 2009 | 1.5003 | 100 percent |

| 2010 | 1.5203 | 100 percent |

| 2011 | 1.5326 | 100 percent |

| 2012 | 1.5686 | 100 percent |

| 2013 | 1.5968 | 100 percent |

| 2014 | 1.5974 | 100 percent |

| 2015 | 1.6245 | 100 percent |

| 2016 | 1.6464 | 0 |

| 2017 | 1.6713 | 0 |

| 2018 | 1.7008 | 1.069 percent |

| 2019 | 1.7334 | 100 percent |

| 2020 | 1.7640 | 100 percent |

| 2021 | 1.7849 | 0 |

| 2022 | 1.8607 | 100 percent |

| 2023 | 1.9998 | 100 percent |

This notice provides the applicable reference price for qualified natural gas production from qualified marginal wells during taxable years beginning in calendar year 2023 for the purpose of determining the marginal well production credit (MWC) under § 45I of the Internal Revenue Code. The applicable reference price for taxable years beginning in calendar year 2023 is $5.57 per 1,000 cubic feet (Mcf).

This notice also provides the credit amount used for the purpose of determining the MWC for taxable years beginning in calendar year 2023. The credit amount is determined using the 2023 inflation adjustment factor of 1.4993 and the applicable reference price of $5.57 per Mcf. The credit amount for taxable years beginning in calendar year 2023 is $0.00 per Mcf.

Section 45I(a), as it relates to qualified natural gas production, provides that, for purposes of § 38, the MWC for any taxable year is an amount equal to the product of (1) the credit amount and (2) the qualified natural gas production that is attributable to the taxpayer.

Section 45I(c)(1) provides that “qualified natural gas production” means domestic natural gas produced from a qualified marginal well. Section 45I(c)(3)(A) provides that a qualified marginal well is a domestic well (i) the production from which during the taxable year is treated as marginal production under § 613A(c)(6), or (ii) which, during the taxable year (I) has average production of not more than 25 barrel-of-oil equivalents per day, and (II) produces water at a rate not less than 95 percent of total well effluent.

Section 613A(c)(6)(D) and (E) provide that “marginal production” means domestic natural gas produced during any taxable year from a property which is a stripper well property for the calendar year in which the taxable year begins. A “stripper well property” is, with respect to any calendar year, any property producing not more than 15 barrel equivalents per day, determined by dividing the average daily production of domestic crude oil and domestic natural gas from producing wells on the property for such calendar year by the number of such wells.

Section 45I(c)(2)(A) provides that generally only the first 1,095 barrels or barrel-of-oil equivalents (as defined in § 45K(d)(5)) produced during the taxable year qualify for the MWC. This limitation is proportionately reduced in the case of a short taxable year or in the case of a well that is not capable of production each day of a taxable year. See § 45I(c)(2)(B). The number of wells on which a taxpayer may claim the MWC is not limited.

Section 45I(d)(2) provides that to claim the credit a taxpayer must hold an operating interest in the qualified marginal well producing the natural gas to which the credit relates. Under § 45I(d)(1) if a well is owned by more than one owner and the natural gas production exceeds the limitation under § 45I(c)(2), the qualifying natural gas production attributable to the taxpayer is determined on the basis of the ratio which the taxpayer’s revenue interest in the production bears to the aggregate of the revenue interests of all operating interest owners in the production. Finally, § 45I(d)(3) provides that the MWC is not allowable if the taxpayer is also eligible to claim the § 45K nonconventional sources credit for the taxable year, unless the taxpayer elects not to claim the credit under § 45K for the well.

For purposes of § 45I(a)(1), the credit amount is 50 cents (adjusted for inflation) per Mcf of qualified natural gas production (tentative credit amount). See § 45I(b)(1)(B) and (b)(2)(B).

Section 45I(b)(2)(A) and (B) provide that the tentative credit amount (adjusted for inflation) is reduced (but not below zero) to the extent that the applicable reference price exceeds $1.67 (adjusted for inflation). More specifically, § 45I(b)(2)(A) provides that the tentative credit amount (adjusted for inflation) is reduced by an amount which bears the same ratio to the tentative credit amount (adjusted for inflation) as the excess (if any) of the applicable reference price over $1.67 (adjusted for inflation), bears to $0.33 (adjusted for inflation). As a result, the MWC is not available if the applicable reference price for qualified natural gas production is $2.00 (adjusted for inflation) or more.

Section 45I(b)(2)(A) also provides that the applicable reference price for a taxable year is the reference price for the calendar year preceding the calendar year in which the taxable year begins. Section 45I(b)(2)(C)(ii) provides that the term “reference price” means, with respect to any calendar year, in the case of qualified natural gas production, the Secretary’s estimate of the annual average wellhead price per Mcf for all domestic natural gas.

Section 45I(b)(2)(B) provides that in the case of any taxable year beginning in a calendar year after 2005, each of the dollar amounts contained in § 45I(b)(2)(A) will be increased to an amount equal to such dollar amount multiplied by the inflation adjustment factor for such calendar year (determined under § 43(b)(3)(B) by substituting “2004” for “1990”).

.1 Inflation Adjustment. The inflation adjustment factor under § 45I(b)(2)(B) for calendar year 2023 is 1.4993.

.2 Reference Price. The Secretary’s estimate of the calendar year 2022 annual average wellhead price per Mcf for all domestic natural gas under § 45I(b)(2)(C)(ii) was calculated by applying the Producer Price Index commodity index for “Natural Gas from the Wellhead” (WPU053101051)1 published by the Bureau of Labor Statistics (BLS) as part of its Producer Price Index program, to the 2021 annual average wellhead price ($3.43) published in Notice 2023-41, 2023-23 I.R.B. 905. The annual Producer Price Index commodity index for natural gas published by the BLS was 106.8 in 2021 and 173.206 in 2022, which implies a ratio of 2022 to 2021 average wellhead prices of 1.622 (173.206/106.801). Therefore, the Secretary’s estimate of the calendar year 2022 annual average wellhead price per Mcf for all domestic natural gas is $5.57 per Mcf (1.622 × $3.43 per Mcf). The one cent difference is due to rounding.

For years after 2022, the Secretary intends to continue calculating the reference price by application of the Producer Price Index commodity index for “Natural Gas from the Wellhead” (WPU053101051) published by the BLS to the previous year’s reference price.

Under § 45I(b)(1)(B) and (2)(B), the tentative credit amount used to calculate the MWC for taxable years beginning in calendar year 2023 is $0.75 per Mcf ($0.50 × 1.4993 inflation adjustment factor). Pursuant to the reduction specified in § 45I(b)(2)(A), the tentative credit amount for taxable years beginning in calendar year 2023 is reduced to zero.

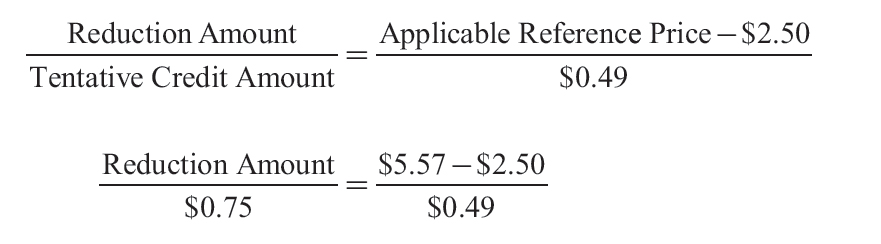

Specifically, pursuant § 45I(b)(2)(A), the tentative credit amount is reduced (but not below zero) by an amount (the Reduction Amount) which bears the same ratio to such amount as (i) the excess (if any) of the applicable reference price over $2.50 ($1.67 × 1.4993 inflation adjustment factor), bears to (ii) $0.49 ($0.33 × 1.4993 inflation adjustment factor). The Reduction Amount (as adjusted for inflation) is computed as follows:

The Reduction Amount is $4.70 (($5.57 - $2.50) ÷ $0.49 × $0.75) and it exceeds the tentative credit amount ($0.75). Therefore, the credit amount used to calculate the MWC for taxable years beginning in calendar year 2023 is $0.00 per Mcf.

This notice is effective for qualified natural gas production during taxable years beginning in calendar year 2023.

The principal author of this notice is Boris Kukso of the Office of Associate Chief Counsel (Passthroughs & Special Industries). For further information regarding this notice contact Mr. Kukso at (202) 317-6853 (not a toll-free number).

1 https://data.bls.gov/cgi-bin/srgate. The BLS publishes indexes and not actual or average prices.

This notice announces that the Department of the Treasury (the Treasury Department) and the Internal Revenue Service (IRS) intend to propose regulations (forthcoming proposed regulations) addressing the requirements for home energy audits with respect to the energy efficient home improvement credit under § 25C of the Internal Revenue Code (Code),1 as amended by § 13301 of Public Law 117-169, 136. Stat. 1818 (August 16, 2022), commonly known as the Inflation Reduction Act of 2022 (IRA). Sections 2 and 3 of this notice provide relevant background and definitions, respectively, with respect to the energy efficient home improvement credit allowed under § 25C (§ 25C credit). Section 4 of this notice specifies the requirements that the forthcoming proposed regulations would set forth for qualifying as a home energy auditor for purposes of the § 25C credit. Sections 5 and 6 of this notice specify the substantiation requirement and transition rule, respectively, that the forthcoming proposed regulations would establish for taxpayers claiming the § 25C credit with respect to home energy audits. Section 7 addresses the application of the Paperwork Reduction Act to this notice. The Treasury Department and the IRS also intend to propose that the forthcoming proposed regulations would apply to taxable years ending after December 31, 2022. Until the issuance of the forthcoming proposed regulations, taxpayers may rely on the rules described in sections 3 through 6 of this notice.

.01 Energy Efficient Home Improvement Credit

Section 25C was originally enacted by § 1333(a) of the Energy Policy Act of 2005, Pub. L. 109-58, 119 Stat. 594, 1026 (August 8, 2005), to provide a tax credit for the purchase and installation of certain energy efficient improvements in taxpayers’ principal residences. Congress has amended § 25C several times since its original enactment, most recently under § 13301 of the IRA, which renamed this provision the “energy efficient home improvement credit” and provided that § 25C, as amended by the IRA, applies to property placed in service prior to January 1, 2033.

Section 13301(b) and (f) of the IRA amended § 25C(a) to allow a credit amount equal to 30 percent of the sum of the amounts that individual taxpayers pay or incur during a taxable year for (1) qualified energy efficiency improvements installed during the year, (2) residential energy property expenditures, and (3) home energy audits.

As amended by § 13301(c) of the IRA, the § 25C credit is generally limited to an annual cap of $1,200. Within this $1,200 limitation, § 25C(b) sets forth further annual caps for certain categories of improvements. The caps and categories of improvements under these limitations are as follows: $600 for any item of qualified energy property, as defined in § 25C(d)(2); $600 for exterior windows and skylights; $250 for any single exterior door and $500 in the aggregate for all exterior doors; and $150 for home energy audits. Section 25C(b) also provides that residential energy property expenditures for heat pumps, heat pump water heaters, biomass stoves, and biomass boilers are not subject to the annual cap of $1,200 or to the $600 limitation for any item of qualified energy property. Instead, residential energy property expenditures for these items are subject to a separate aggregate annual limitation of $2,000. Section 25C(d) provides that the term “residential energy property expenditures” includes expenditures for labor costs properly allocable to the onsite preparation, assembly, or original installation of the property.

.02 Credit for Home Energy Audit Expenditures

Section 13301(f) of the IRA amended § 25C to expand the types of expenditures eligible for the § 25C credit to include expenditures for home energy audits. Section 25C(e) defines the term “home energy audit” as an inspection and written report with respect to a dwelling unit located in the United States and owned or used by the taxpayer as the taxpayer’s principal residence (within the meaning of § 121). The audit must (1) identify the most significant and cost-effective energy efficiency improvements with respect to such dwelling unit, including an estimate of the energy and cost savings with respect to each such improvement, and (2) be conducted and prepared by a home energy auditor that meets the certification or other requirements specified by the Secretary of the Treasury or her delegate (Secretary) in regulations or other guidance. The IRA also imposed two limitations on this credit. First, as described above, § 25C(b)(6)(A) limits the credit allowed for amounts paid or incurred by the taxpayer during the taxable year for home energy audits up to $150. Under this limit, for example, a taxpayer that pays $1000 for a home energy audit during the taxable year may only claim a $150 credit for such taxable year for this expenditure, and not the full 30 percent of the amount of the expenditure, even if the taxpayer does not have any other expenditures eligible for the § 25C credit during the taxable year. Second, § 25C(b)(6)(B) imposes a substantiation requirement, requiring taxpayers claiming the credit to include with their tax returns “such information or documentation as the Secretary may require”.

In Notice 2022-48, 2022-43 I.R.B. 305, the Treasury Department and the IRS requested comments on various questions arising from the IRA’s energy efficiency provisions. Among other questions, the notice requested comments on what certification or other requirements the Treasury Department and the IRS should require for home energy auditors that conduct the inspection and provide the written report that constitutes a “home energy audit” that qualifies for the § 25C credit.

The Treasury Department and the IRS published a Fact Sheet (FS-2022-40) on December 22, 2022, addressing “frequently asked questions about energy efficient home improvements and residential clean energy property credits.” This Fact Sheet provides that a qualifying home energy audit “must include an inspection of a dwelling, including condominiums and certain manufactured homes, located in the United States that is owned or used by the taxpayer as the taxpayer’s principal residence. The home energy auditor must provide a written report (to the taxpayer) that identifies the most significant and cost-effective energy efficiency improvements for that dwelling, including an estimate of the energy and cost savings for each such improvement. The auditor must meet the certification or other requirements specified by the Department of the Treasury and the Internal Revenue Service in forthcoming guidance.” The Fact Sheet also clarifies that the § 25C credit with respect to home energy audits may be claimed by a taxpayer renting a home as their principal residence provided such home is located in the United States.

.01 Home Energy Audit Credit. The term “Home Energy Audit Credit” means the § 25C credit allowed to individuals by reason of § 25C(a)(3) equal to 30 percent of the amount paid or incurred for Home Energy Audits in the taxable year, up to $150 per taxable year.

.02 Home Energy Audit. The term “Home Energy Audit” means an inspection and written report (audit) with respect to a dwelling unit located in the United States and owned or used by the taxpayer as the taxpayer’s principal residence (within the meaning of § 121) that meets each of the following requirements.

(1) The audit identifies the most significant and cost-effective energy efficiency improvements with respect to such dwelling unit, including an estimate of the energy and cost savings with respect to each such improvement,

(2) The inspection is conducted either by a Qualified Home Energy Auditor or under the supervision of a Qualified Home Energy Auditor,

(3) The written report is prepared and signed by a Qualified Home Energy Auditor, and

(4) The audit is consistent with the most recent Department of Energy (DOE)-led and industry-validated Jobs Task Analysis.2

.03 Qualified Home Energy Auditor. The term “Qualified Home Energy Auditor” means an individual who is a home energy auditor that is certified by a Qualified Certification Program at the time of the Home Energy Audit.

.04 Qualified Certification Program. The term “Qualified Certification Program” means a certification program described in section 4.03 of this notice.

.01 In General. Except as otherwise provided in section 6 of this notice, the forthcoming proposed regulations would provide that a taxpayer may claim the Home Energy Audit Credit for a taxable year only if the taxpayer pays or incurs amounts for a Home Energy Audit.

.02 Written Report. The forthcoming proposed regulations would require the Qualified Home Energy Auditor to provide the following information in the written report:

(1) The Qualified Home Energy Auditor’s name and the relevant employer identification number (EIN) or other type of relevant taxpayer identifying number as referenced in § 301.6109-1(a)(1)(i) of the Procedure and Administration Regulations (26 CFR part 301) in lieu of an EIN,3

(2) An attestation that the Qualified Home Energy Auditor is certified by a Qualified Certification Program, and

(3) The name of such Qualified Certification Program.

.03 Qualified Certification Program. A Qualified Certification Program is a certification program that satisfies the criteria described in section 4.03(1) and (2) of this notice for certifying home energy auditors and that is included in the list described in section 4.04 of this notice.

(1) The certification program must be reviewed and evaluated through the most recent DOE-led and industry-validated Jobs Task Analysis, demonstrating substantial alignment with key duties, tasks, knowledge, skills, and abilities of home energy auditors.

(2) The certification program must satisfy one of following standards development processes:

(a) The credentials are developed and maintained in accordance with industry standards using criteria such as those cited in the Department of Labor (DOL) Training and Employment Notice No. 25-194, Attachment I, section b., or the most recent guidance from DOL on characteristics of credentials; or

(b) The program is accredited by the American National Standards Institute (ANSI), International Accreditation Service, or other qualified accreditation bodies that are in compliance with ISO/IEC 17024:2012, Conformity assessment – General requirements for bodies operating certification of persons.

.04 Qualified Certification Programs List. The list of Qualified Certification Programs is maintained by the DOE at the following web address: https://www.energy.gov/eere/buildings/25c-energy- efficient-home-improvement-credit. The listed Qualified Certification Programs are the exclusive certification programs through which an auditor can qualify as a Qualified Home Energy Auditor, and that will allow a taxpayer to claim the Home Energy Audit Credit. DOE intends to update the list on a rolling basis as it identifies additional Qualified Certification Programs.

The forthcoming proposed regulations would provide that taxpayers claiming the Home Energy Audit Credit would be in compliance with the substantiation requirement under § 25C(b)(6)(B) if they (1) maintain the written report signed by the Qualified Home Energy Auditor as a record, pursuant to the general recordkeeping and retention requirements under § 6001 and §1.6001-1, and (2) comply with the instructions for Form 5695, Residential Energy Credits, or any successor form required by the IRS.

With respect to home energy audits conducted during taxable years ending after December 31, 2022, and conducted on or before December 31, 2023, a home energy auditor is not required to be a Qualified Home Energy Auditor as defined in section 3.03 of this notice. Therefore, taxpayers that paid or incurred expenses for a home energy audit that meets the requirements of § 25C, and that was conducted during taxable years ending after December 31, 2022, and conducted on or before December 31, 2023, may claim a Home Energy Audit Credit for such audit even if the auditor who conducted the home energy audit was not a Qualified Home Energy Auditor, as defined in section 3.03 of this notice, at the time of the home energy audit. However, taxpayers may not claim a Home Energy Audit Credit for home energy audits conducted after December 31, 2023, that were not conducted by a Qualified Home Energy Auditor.

The Paperwork Reduction Act of 1995 (44 U.S.C. 3501-3520) (“PRA”) generally requires that a federal agency obtain the approval of the Office of Management and Budget (OMB) before collecting information from the public, whether such collection of information is mandatory, voluntary, or required to obtain or retain a benefit. An agency may not conduct or sponsor, and a person is not required to respond to, a collection of information unless the collection of information displays a valid OMB control number.

The collection of information contained in this notice includes recordkeeping requirements, as detailed in section 5 of this notice. These recordkeeping requirements are approved by OMB under 1545-0074.

Additionally, the notice includes a third-party disclosure requirement for Qualified Home Energy Auditors to provide a written report (to the taxpayer) that identifies the most significant and cost-effective energy efficiency improvements for that dwelling, including an estimate of the energy and cost savings for each such improvement. The disclosure of these reports is considered a usual and customary business practice provided during the normal course of business in conducting a Home Energy Audit. This customary business practice imposes no additional burden on respondents.

The principal author of this notice is the Office of Associate Chief Counsel (Passthroughs & Special Industries). For further information regarding this notice contact the Office of Associate Chief Counsel (Passthroughs & Special Industries) at (202) 317-6853 (not a toll-free number).

1 Unless otherwise specified, all “section” or “§” references are to sections of the Code or the Income Tax Regulations (26 CFR part 1).

2 The Single-Family Energy Auditor Job Task Analysis and a Multifamily Energy Auditor Job/Task Analysis and Report were developed by the National Renewable Energy Laboratory. Public comment informed the development of these documents. See Workforce Guidelines for Home Energy Upgrades, 75 FR 68781 (Nov. 9, 2010), available at: https://www.federalregister.gov/documents/2010/11/09/2010-28289/workforce-guidelines-for-home-energy-upgrades.

3 If the Qualified Home Energy Auditor is acting in his or her capacity as a partner in a partnership, or as an employee of any person, whether an individual, corporation, or partnership, the relevant EIN is the EIN of the partnership or the person who employs the Qualified Home Energy Auditor.

4 Employment & Training Administration Training and Employment Notice No. 25-19 (Jun. 08, 2020) available at: https://www.dol.gov/agencies/eta/advisories/training-and-employment- notice-no-25-19.

The Office of Professional Responsibility (OPR) announces recent disciplinary sanctions involving attorneys, certified public accountants, enrolled agents, enrolled actuaries, enrolled retirement plan agents, appraisers, and unenrolled/unlicensed return preparers (individuals who are not enrolled to practice and are not licensed as attorneys or certified public accountants). Licensed or enrolled practitioners are subject to the regulations governing practice before the Internal Revenue Service (IRS), which are set out in Title 31, Code of Federal Regulations, Subtitle A, Part 10, and which are released as Treasury Department Circular No. 230. The regulations prescribe the duties and restrictions relating to such practice and prescribe the disciplinary sanctions for violating the regulations. Unenrolled/unlicensed return preparers are subject to Revenue Procedure 81-38 and superseding guidance in Revenue Procedure 2014-42, which govern a preparer’s eligibility to represent taxpayers before the IRS in examinations of tax returns the preparer both prepared for the taxpayer and signed as the preparer. Additionally, unenrolled/unlicensed return preparers who voluntarily participate in the Annual Filing Season Program under Revenue Procedure 2014-42 agree to be subject to the duties and restrictions in Circular 230, including the restrictions on incompetent or disreputable conduct.

The disciplinary sanctions to be imposed for violation of the applicable standards are:

Disbarred from practice before the IRS—An individual who is disbarred is not eligible to practice before the IRS as defined at 31 C.F.R. § 10.2(a)(4) for a minimum period of five (5) years.

Suspended from practice before the IRS—An individual who is suspended is not eligible to practice before the IRS as defined at 31 C.F.R. § 10.2(a)(4) during the term of the suspension.

Censured in practice before the IRS—Censure is a public reprimand. Unlike disbarment or suspension, censure does not affect an individual’s eligibility to practice before the IRS, but OPR may subject the individual’s future practice rights to conditions designed to promote high standards of conduct.

Monetary penalty—A monetary penalty may be imposed on an individual who engages in conduct subject to sanction, or on an employer, firm, or entity if the individual was acting on its behalf and it knew, or reasonably should have known, of the individual’s conduct.

Disqualification of appraiser—An appraiser who is disqualified is barred from presenting evidence or testimony in any administrative proceeding before the Department of the Treasury or the IRS.

Ineligible for limited practice—An unenrolled/unlicensed return preparer who fails to comply with the requirements in Revenue Procedure 81-38 or to comply with Circular 230 as required by Revenue Procedure 2014-42 may be determined ineligible to engage in limited practice as a representative of any taxpayer.

Under the regulations, individuals subject to Circular 230 may not assist, or accept assistance from, individuals who are suspended or disbarred with respect to matters constituting practice (i.e., representation) before the IRS, and they may not aid or abet suspended or disbarred individuals to practice before the IRS.

Disciplinary sanctions are described in these terms:

Disbarred by decision, Suspended by decision, Censured by decision, Monetary penalty imposed by decision, and Disqualified after hearing—An administrative law judge (ALJ) issued a decision imposing one of these sanctions after the ALJ either (1) granted the government’s summary judgment motion or (2) conducted an evidentiary hearing upon OPR’s complaint alleging violation of the regulations. After 30 days from the issuance of the decision, in the absence of an appeal, the ALJ’s decision becomes the final agency decision.

Disbarred by default decision, Suspended by default decision, Censured by default decision, Monetary penalty imposed by default decision, and Disqualified by default decision—An ALJ, after finding that no answer to OPR’s complaint was filed, granted OPR’s motion for a default judgment and issued a decision imposing one of these sanctions.

Disbarment by decision on appeal, Suspended by decision on appeal, Censured by decision on appeal, Monetary penalty imposed by decision on appeal, and Disqualified by decision on appeal—The decision of the ALJ was appealed to the agency appeal authority, acting as the delegate of the Secretary of the Treasury, and the appeal authority issued a decision imposing one of these sanctions.

Disbarred by consent, Suspended by consent, Censured by consent, Monetary penalty imposed by consent, and Disqualified by consent—In lieu of a disciplinary proceeding being instituted or continued, an individual offered a consent to one of these sanctions and OPR accepted the offer. Typically, an offer of consent will provide for: suspension for an indefinite term; conditions that the individual must observe during the suspension; and the individual’s opportunity, after a stated number of months, to file with OPR a petition for reinstatement affirming compliance with the terms of the consent and affirming current fitness and eligibility to practice (i.e., an active professional license or active enrollment status, with no intervening violations of the regulations).

Suspended indefinitely by decision in expedited proceeding, Suspended indefinitely by default decision in expedited proceeding, Suspended by consent in expedited proceeding—OPR instituted an expedited proceeding for suspension (based on certain limited grounds, including loss of a professional license for cause, and criminal convictions).

Determined ineligible for limited practice—There has been a final determination that an unenrolled/unlicensed return preparer is not eligible for limited representation of any taxpayer because the preparer violated standards of conduct or failed to comply with any of the requirements to act as a representative.

A practitioner who has been disbarred or suspended under 31 C.F.R. § 10.60, or suspended under § 10.82, or a disqualified appraiser may petition for reinstatement before the IRS after the expiration of 5 years following such disbarment, suspension, or disqualification (or immediately following the expiration of the suspension or disqualification period if shorter than 5 years). Reinstatement will not be granted unless the IRS is satisfied that the petitioner is not likely to engage thereafter in conduct contrary to Circular 230, and that granting such reinstatement would not be contrary to the public interest.

Reinstatement decisions are published at the individual’s request, and described in these terms:

Reinstated to practice before the IRS—The individual’s petition for reinstatement has been granted. The agent, and eligible to practice before the IRS, or in the case of an appraiser, the individual is no longer disqualified.

Reinstated to engage in limited practice before the IRS—The individual’s petition for reinstatement has been granted. The individual is an unenrolled/unlicensed return preparer and eligible to engage in limited practice before the IRS, subject to requirements the IRS has prescribed for limited practice by tax return preparers.

OPR has authority to disclose the grounds for disciplinary sanctions in these situations: (1) an ALJ or the Secretary’s delegate on appeal has issued a final decision; (2) the individual has settled a disciplinary case by signing OPR’s “consent to sanction” agreement admitting to one or more violations of the regulations and consenting to the disclosure of the admitted violations (for example, failure to file Federal income tax returns, lack of due diligence, conflict of interest, etc.); (3) OPR has issued a decision in an expedited proceeding for indefinite suspension; or (4) OPR has made a final determination (including any decision on appeal) that an unenrolled/unlicensed return preparer is ineligible to represent any taxpayer before the IRS.

Announcements of disciplinary sanctions appear in the Internal Revenue Bulletin at the earliest practicable date. The sanctions announced below are alphabetized first by state and second by the last names of the sanctioned individuals.

| City & State | Name | Professional Designation | Disciplinary Sanction | Effective Date(s) |

|---|---|---|---|---|

| Alabama | ||||

| Sumner, Elizabeth, see Mississippi | ||||

| Arizona | ||||

| Goodyear | Plimley, Rise H. | Enrolled Agent | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from May 30, 2023 |

| California | ||||

| Larkspur | Blecka, John C. | CPA | Reinstated to practice before the IRS, effective 04/19/2023 | |

| Colorado | ||||

| Erie | Devaney, Cathleen A. | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from May 30, 2023 |

| Illinois | ||||

| Kingston | Jensen, Cynthia (Cyndi) | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from May 30, 2023 |

| Louisiana | ||||

| Baton Rouge | Triche, Wayne A. | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from June 6, 2023 |

| Maryland | ||||

| Baltimore | Dailey, Mitzi E. | Attorney | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from May 3, 2023 |

| Massachusetts | ||||

| Wrentham | Hubbell, Scott C. | Attorney | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from May 30, 2023 |

| Mississippi | ||||

| Meridian | Sumner, Elizabeth R. | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from June 27, 2023 |

| New Hampshire | ||||

| Manchester | Dunn, David C. | Attorney | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from June 21, 2023 |

| North Carolina | ||||

| Charlotte | Caviness, Elizabeth J. | Attorney | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from June 21, 2023 |

| James, Andre, see Virginia | ||||

| Lexington | Rives, II, Leon L. | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from June 27, 2023 |

| Virginia | ||||

| Fairfax | James, Andre | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from April 17, 2023 |

| Washington | ||||

| Bellevue | Shimizu, Steven G. | CPA | Suspended by default decision in expedited proceeding under 31 C.F.R. § 10.82(b) | Indefinite from May 30, 2023 |

AGENCY: Internal Revenue Service (IRS), Treasury.

ACTION: Notice of proposed rulemaking; withdrawal of notices of proposed rulemaking; partial withdrawal of notices of proposed rulemaking; and proposed withdrawal of temporary regulations.

SUMMARY: This document contains proposed amendments to regulations applicable to affiliated groups of corporations that file consolidated Federal income tax returns. The proposed regulations would modify those regulations to reflect statutory changes, update language to remove antiquated or regressive terminology, and enhance clarity. Additionally, this document partially or completely withdraws certain notices of proposed rulemaking and proposes to withdraw certain temporary regulations. The proposed regulations would affect corporations filing consolidated returns.

DATES: As of August 7, 2023, the notices of proposed rulemaking published on November 14, 2001 (66 FR 57021), March 12, 2002 (67 FR 11070), May 31, 2002 (67 FR 38039), May 31, 2002 (67 FR 38040), March 14, 2003 (68 FR 12324), May 7, 2003 (68 FR 24404), March 18, 2004 (69 FR 12811), August 18, 2004 (69 FR 51209), August 26, 2004 (69 FR 52462), April 10, 2007 (72 FR 17814), and June 23, 2010 (75 FR 35710) are withdrawn. As of August 7, 2023, the notices of proposed rulemaking published on December 30, 1992 (57 FR 62251-01), March 18, 2004 (69 FR 12281), and June 11, 2015 (80 FR 33211) are partially withdrawn (see SUPPLEMENTARY INFORMATION for specific details). Written or electronic comments as well as requests for a public hearing must be received by November 6, 2023. Requests for a public hearing must be submitted as prescribed in the “Comments and Requests for a Public Hearing” section.

ADDRESSES: Commenters are strongly encouraged to submit public comments electronically. Submit electronic submissions via the Federal eRulemaking Portal at https://www.regulations.gov (indicate IRS and REG-134420-10). Once submitted to the Federal eRulemaking Portal, comments cannot be edited or withdrawn. The Department of the Treasury (Treasury Department) and the IRS will publish for public availability any comment submitted to its public docket.

Send paper submissions to: CC:PA:LPD:PR (REG-134420-10), Room 5203, Internal Revenue Service, P.O. Box 7604, Ben Franklin Station, Washington, DC 20044.

FOR FURTHER INFORMATION CONTACT: Concerning the proposed regulations, William W. Burhop at (202) 317-5363 or Kelton P. Frye at (202) 317-5135 (not toll-free numbers); concerning the submission of comments and/or requests for a public hearing, Vivian Hayes by email at publichearings@irs.gov or by phone at (202) 317-5306 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

This notice of proposed rulemaking (NPRM) contains proposed regulations under sections 1502, 1503, 1552, and 1563 of the Internal Revenue Code of 1986 (Code). These proposed regulations primarily would revise the Income Tax Regulations (26 CFR part 1) under section 1502 (consolidated return regulations). Section 1502 authorizes the Secretary of the Treasury or the Secretary’s delegate (Secretary) to prescribe consolidated return regulations for an affiliated group of corporations that join in filing (or that are required to join in filing) a consolidated return (consolidated group) to clearly reflect the Federal income tax liability of the consolidated group and to prevent avoidance of such tax liability. See §1.1502-1(h) (defining the term “consolidated group”). For purposes of carrying out those objectives, section 1502 also permits the Secretary to prescribe rules that may be different from the provisions of chapter 1 of the Code (chapter 1) that would apply if the corporations composing the consolidated group filed separate returns. Terms used in the consolidated return regulations generally are defined in §1.1502-1.

The proposed regulations also would revise or propose to remove other regulations under the Code. These regulations are set forth in (i) the Income Tax Regulations (26 CFR part 1), (ii) the Temporary Income Tax Regulations under the Revenue Act of 1978 (26 CFR part 5), (iii) the Regulations on Procedure and Administration (26 CFR part 301), and (iv) the OMB Control Numbers under the Paperwork Reduction Act Regulations (26 CFR part 602).

In this NPRM, the Treasury Department and the IRS have proposed revisions to the consolidated return regulations to (i) eliminate obsolete or otherwise outdated provisions, (ii) modernize the language and improve the clarity of the regulations, and (iii) facilitate taxpayer compliance. As an initial matter, the proposed regulations would update the consolidated return regulations to reflect statutory changes made by legislation enacted during the last 50-plus years and remove consolidated return regulations that have no practical applicability to taxpayers. The proposed regulations also would revise the consolidated return regulations to eliminate obsolete or otherwise incorrect terms and cross-references. Lastly, the proposed regulations generally would remove transition rules for transactions occurring in or before 2009 because the taxable years affected by such transition rules generally are closed and the rules have no practical applicability to taxpayers.

The proposed regulations also would update the consolidated return regulations and the regulations under section 1563 to eliminate antiquated or regressive terminology. For example, the proposed regulations would replace all gender-specific pronouns and other identifiers in the consolidated return regulations with gender-neutral pronouns and identifiers. The proposed regulations also would revise the consolidated regulations to identify (i) American Samoa, (ii) the Commonwealth of the Northern Mariana Islands, (iii) the Commonwealth of Puerto Rico, (iv) Guam, and (v) the U.S. Virgin Islands as “territories” of the United States rather than “possessions.” Each of those jurisdictions has its own government and its own tax system. These revisions are consistent with, and in furtherance of, the Treasury Department’s Equity Action Plan, as well as Executive Order 13985 of January 20, 2021, Advancing Racial Equity and Support for Underserved Communities Through the Federal Government, 86 FR 7009 (January 25, 2021).

The proposed regulations also withdraw or partially withdraw numerous NPRMs. These NPRMs include: (i) NPRMs that are incorporated, in revised form, into these proposed regulations or that were incorporated into final regulations in revised form; (ii) a NPRM that became obsolete when proposed regulations provided in a subsequent, discrete NPRM were adopted as final regulations; and (iii) NPRMs that cross-referenced temporary regulations (the text of which served as the text for those proposals) that were removed, have expired, or otherwise have become obsolete. Additionally, the proposed regulations propose to withdraw temporary regulations that (i) no longer have practical applicability to taxpayers, or (ii) would be replaced by final regulations proposed by this document.

With regard to each provision of the consolidated return regulations that these proposed regulations would remove, the Treasury Department and the IRS generally have proposed to reserve the affected provision. This approach is intended solely to avoid cascading changes to cross-references throughout the consolidated return regulations, thereby preserving historical citations and reducing potential confusion for taxpayers. Accordingly, the reserving of those provisions does not indicate in any manner that the Treasury Department and the IRS are studying, or intend to study, any of the one or more topics addressed by the reserved provision.

Lastly, the proposed regulations would remove numerous provisions that cross-reference prior-law editions of the Code of Federal Regulations (CFR). Following adoption of the proposed regulations as final regulations, taxpayers may consult the CFR for a particular year to determine the rules applicable to that year.

The Treasury Department and the IRS request comments on whether any aspect of the proposed regulations would effectuate a substantive revision of the consolidated return regulations, as opposed to a mere update or similar modification. Additionally, comments are requested on whether any provision proposed to be removed or revised by this document should be retained in its form as of August 4, 2023. Lastly, the Treasury Department and the IRS request comments identifying any other provision of the consolidated return regulations that should be revised consistent with the scope of the proposed regulations, such as additional provisions of the consolidated return regulations that are obsolete or otherwise outdated.

A. Removal of regulations that implement repealed statutory provisions

The proposed regulations would remove provisions of the consolidated return regulations that have been rendered obsolete by enacted legislation.

1. Section 1.1502-1 (definitions)

Sections 1.1502-1(f)(2) and (3) currently reference section 1562 of the Internal Revenue Code of 1954 (1954 Code), which allowed controlled groups of corporations (as defined in section 1563(a) of the 1954 Code) to elect multiple surtax exemptions. Section 1562 of the 1954 Code was repealed by section 401(a)(2) of the Tax Reform Act of 1969, Public Law 91-172, 83 Stat. 487 (December 30, 1969). The proposed regulations would remove from §1.1502-1(f)(2) and (3) all references to section 1562 of the 1954 Code.

2. Section 1.1502-11 (consolidated taxable income)

The proposed regulations would remove §1.1502-11(a)(6), which provides that consolidated taxable income for a consolidated return year is determined by taking into account any “consolidated section 922 deduction.” Section 922 of the 1954 Code (providing a deduction for Western Hemisphere trade corporations) was repealed for taxable years beginning after December 31, 1979, by section 1052(b) of the Tax Reform Act of 1976, Public Law 94-455, 90 Stat. 1520 (October 4, 1976). In 1984, a subsequent section 922 (relating to foreign sales corporations) was added to the 1954 Code by section 801(a) of the Deficit Reduction Act of 1984, Public Law 98-369, 98 Stat. 494 (July 18, 1984), which defined the term “FSC” for purposes of statutory provisions regarding the taxation of foreign sales corporations. This subsequent section 922 of the 1954 Code was redesignated as section 922 of the Code (by section 2(a) of the Tax Reform Act of 1986, Public Law 99-514, 100 Stat. 2085 (October 22, 1986)) before its repeal by section 2 of the FSC Repeal and Extraterritorial Income Exclusion Act of 2000, Public Law 106-519, 114 Stat. 2423 (November 15, 2000). This repeal applies to transactions after September 30, 2000. See section 5(a) of the FSC Repeal and Extraterritorial Income Exclusion Act of 2000.

The proposed regulations also would revise §1.1502-11 to make other minor updates. Specifically, the proposed regulations would remove references to rules applicable to taxable years beginning before January 1, 1977, because those rules no longer have practical applicability to taxpayers. In addition, the proposed regulations would remove references to prior law regulations proposed to be withdrawn by this document.

3. Section 1.1502-12 (separate taxable income)

The proposed regulations would remove §1.1502-12(m), which provides that no deduction under now-repealed section 922 of the 1954 Code is taken into account in determining taxable income of separate corporations (that is, separate taxable income). See part II.A.2 of this Explanation of Provisions (describing the repeal of section 922 of the 1954 Code). The proposed regulations also would revise §1.1502-12(n) to remove references to section 244 of the Code, which related to a special dividends-received deduction (DRD) for dividends received on certain preferred stock, and former section 247 of the Code, which related to a special DRD for dividends paid on certain preferred stock of public utilities. Sections 244 and 247 of the Code were repealed by section 221(a)(41)(A) of Division A of the Tax Increase Prevention Act of 2014, Public Law 113-295, 128 Stat. 4010 (December 19, 2014). Although section 13821(b)(1) of Public Law 115-97, 131 Stat. 2054 (December 22, 2017), commonly referred to as the “Tax Cuts and Jobs Act” (TCJA), added a new section 247 to the Code, that statutory provision allows deductions for certain contributions to Alaska Native Settlement Trusts and therefore is not applicable with regard to DRDs.

4. Section 1.1502-13 (intercompany transactions)

The proposed regulations would revise §1.1502-13(c)(5) to remove a reference to section 595 of the Code, which provided nonrecognition treatment for foreclosure on property that secured the payment of indebtedness. Section 595 of the Code was repealed by section 1616(b)(8) of the Small Business Jobs Protection Act of 1996, Public Law 104-188, 110 Stat. 1755 (August 20, 1996).

5. Section 1.1502-24 (consolidated charitable contributions deduction)

Section 1.1502-24(a) sets forth a rule to determine the amount of the consolidated charitable contributions deduction for a consolidated group. The proposed regulations would revise §1.1502-24(c) to remove the reference to section 242 of the 1954 Code, which allowed for a deduction for partially tax-exempt interest for C corporations. Section 242 of the 1954 Code was repealed by section 1901(a)(33) of the Tax Reform Act of 1976.

6. Section 1.1502-26 (consolidated dividends received deduction)

The proposed regulations would revise §1.1502-26 by removing paragraphs (a)(2) through (6) of that section, which provide rules to calculate a consolidated DRD by taking into account thrift institution members of the group (including such members that compute a deduction based on the “percentage of taxable income method” under section 593(b)(2) of the Code). Section 1616(a) of the Small Business Jobs Protection Act of 1996 added section 593(f) to the Code. Section 593(f) provides that sections 593(a) through (d) of the Code do not apply to any taxable year beginning after December 31, 1995.

7. Section 1.1502-27 (consolidated section 247 deduction) and related provisions

As discussed in part II.A.3 of this Explanation of Provisions, (i) section 247 of the Code was repealed by section 221(a)(41)(A) of Division A of the Tax Increase Prevention Act of 2014; and (ii) section 13821(b)(1) of the TCJA added to the Code a new section 247, which allows deductions for certain contributions to Alaska Native Settlement Trusts. Accordingly, the proposed regulations would remove §1.1502-27, which provides rules under the version of section 247 of the Code repealed by the Tax Increase Prevention Act of 2014. The proposed regulations also would (i) remove §1.1502-11(a)(8), which solely provides a reference to a consolidated section 247 deduction computed under §1.1502-27, and (ii) revise §§1.1502-24(c) and 1.1502-43(b)(2)(iii), to remove a cross-reference to §1.1502-27 in each respective section.

8. Section 1.1502-42 (consolidated returns including thrift institutions) and related provisions

The proposed regulations would remove §1.1502-42, which provides rules for members of a consolidated group that are thrift institutions (that is, any member that is described in section 593(a) of the Code). Section 1.1502-42 became obsolete as a result of the enactment of section 593(f) of the Code by section 1616(a) of the Small Business Jobs Protection Act of 1996, which provides that sections 593(a) through (d) of the Code do not apply to any taxable year beginning after December 31, 1995. The proposed regulations also would remove §1.1502-12(q), which provides solely that a thrift institution’s deduction under section 593(b)(2) of the Code is determined under §1.1502-42.

9. Section 5.1502-45 (at-risk limitation temporary regulations)

The Treasury Department and the IRS published §5.1502-45 as temporary regulations relating to the application of the at-risk limitations under section 465 of the 1954 Code to corporations that join with their subsidiaries in filing a consolidated return. See TD 7685, published in the Federal Register (45 FR 16484) on March 14, 1980 (at-risk limitation temporary regulations). Prior to the publication of §5.1502-45, the Treasury Department determined that consolidated groups were actively considering transactions or plans to avoid the at-risk limitations. See preamble to the at-risk limitation temporary regulations, 45 FR 16484. Under the temporary regulations, if a parent meets the stock ownership test for a personal holding company, a subsidiary’s loss from an activity to which section 465 of the Code (as redesignated by section 2(a) of the Tax Reform Act of 1986) applies will be allowed as a deduction on a consolidated return only to the extent that the parent is at risk in the activity of a subsidiary, under the principles of section 465 of the Code, as of the close of the subsidiary’s taxable year. See id.

Section 5.1502-45(a)(4) refers to section 465(c)(3)(D) of the 1954 Code, which was repealed by section 503(a) of the Tax Reform Act of 1986. The Treasury Department and the IRS understand that no proposed regulations ever were published with regard to §5.1502-45. Therefore, in addition to addressing the reference to repealed section 465(c)(3)(D) of the 1954 Code, this document proposes the entire text of §5.1502-45 as proposed §1.1502-45 and proposes to withdraw §5.1502-45. The Treasury Department and the IRS request comments on proposed §1.1502-45.

B. Updates to reflect amended statutory provisions

The proposed regulations would remove or revise regulations under section 1502 and other provisions of the Code that implement statutory provisions that have been substantially revised since those regulations were promulgated.

1. Section 1.167(c)-1 (limitations on methods of computing depreciation under section 167(b)(2), (3), and (4))

Section 1.167(c)-1(a)(5) provides a reference to certain provisions of the consolidated return regulations that address depreciation of property received by a member of an affiliated group from another member of the group during a consolidated return period. To implement amendments made by the TCJA to section 168(k) of the Code, the Department of the Treasury and the Internal Revenue Service published final regulations under §1.1502-68 that provide guidance regarding the additional first-year depreciation deduction under section 168(k). See TD 9916, published in the Federal Register (85 FR 71734) on November 10, 2020. See also sections 12001(b)(13), 13201, and 13204 of the TCJA. Accordingly, the proposed regulations would revise §1.167(c)-1(a)(5) to include a reference to §1.1502-68.

2. Section 1.1502-1(g) (definition of “consolidated return change of ownership”)

The proposed regulations would remove paragraph (g) of §1.1502-1, which provides rules to determine the occurrence of a consolidated return change of ownership (CRCO). The CRCO rules generally paralleled the ownership change rules of section 382 of the 1954 Code, as that section existed prior to enactment of the Tax Reform Act of 1986. See preamble to the NPRM published in the Federal Register (56 FR 4228, 4232) on February 4, 1991. Following the complete revision of section 382 of the 1954 Code by the Tax Reform Act of 1986, the Treasury Department and the IRS determined that the policies underlying the CRCO rules were subsumed by the single-entity approach to the application of section 382 of the Code to consolidated groups. See section 621(a) of the Tax Reform Act of 1986. See also 56 FR at 4232. Accordingly, the Treasury Department and the IRS replaced the CRCO rules with the consolidated section 382 rules set forth in §§1.1502-90 through 1.1502-99. See TD 8679, published in the Federal Register (61 FR 33313) on June 27, 1996.

3. Section 1.1502-3 (consolidated tax credits)

The proposed regulations would remove §1.1502-3(e), which applies only to a CRCO that occurred during a consolidated return year for which the due date of the Federal income tax return (without extensions) is on or before March 13, 1998. See §1.1502-3(e)(3).

4. Section 1.1502-5 (consolidated estimated tax)

The Treasury Department and the IRS published proposed regulations in the Federal Register (57 FR 62251) on December 30, 1992, regarding the computation of the former alternative minimum tax (Former AMT) by consolidated groups and the allocation of related items (consolidated Former AMT proposed regulations). The proposed regulations would incorporate in revised form part of the consolidated Former AMT proposed regulations that proposed to amend the consolidated estimated tax provisions in §1.1502-5. The Treasury Department and the IRS received no comments on §1.1502-5 as proposed in the consolidated Former AMT proposed regulations.

The proposed regulations would revise §1.1502-5 to reflect the amendments to section 6655, which provides penalties for corporations failing to pay estimated income tax, made by section 10301(a) of the Omnibus Budget Reconciliation Act of 1987, Public Law 100-203, 101 Stat. 1330 (December 22, 1987). The proposed regulations also would remove references to section 6154 of the Code, which provided special rules for installment payments of estimated tax by corporations prior to the repeal of section 6154 of the Code by section 10301(b)(1) of the Omnibus Budget Reconciliation Act of 1987, and would add a reference to section 59A, which was added to section 6655(g)(1) by section 14401(d)(4)(A) of the TCJA.

The consolidated Former AMT proposed regulations provided guidance on consolidated estimated taxes under the Former AMT in section 55 of the Code and the environmental tax under former section 59A of the Code. The Former AMT was made inapplicable to corporations by section 12001(a) of the TCJA, and former section 59A of the Code was repealed by section 221(a)(12)(A), Division A, of the Tax Increase Prevention Act of 2014. Current section 59A of the Code (as added by section 14401(a) of the TCJA) imposes the base erosion and anti-abuse tax, commonly referred to as the “BEAT.”

As a result of those amendments to the Code, the proposed regulations would make the following revisions to §1.1502-5. First, the proposed regulations would not incorporate provisions from the consolidated Former AMT proposed regulations that addressed these issues. However, section 10101 of Public Law 117-169, 136 Stat. 1818 (August 16, 2022), commonly referred to as the Inflation Reduction Act of 2022, amended section 55 of the Code to impose a new corporate alternative minimum tax based on adjusted financial statement income. This new corporate alternative minimum tax is commonly referred to as the corporate alternative minimum tax, or CAMT. Therefore, the proposed regulations would modify the definition of the term “tax” in §1.1502-5(b)(5) to add a reference to section 55(a). In addition, the proposed regulations would add a reference to section 59A (that is, the BEAT).

The Treasury Department and the IRS are actively working on guidance to implement the CAMT, including guidance on the application of the CAMT to consolidated groups. Accordingly, issues regarding the substantive operation of the CAMT will be addressed in that guidance. However, these proposed regulations would provide guidance regarding the computation of consolidated estimated taxes to take into account the CAMT liability of the consolidated group.

5. Section 1.1502-9 (consolidated overall foreign losses, separate limitation losses, and overall domestic losses)

The proposed regulations would revise §1.1502-9 to account for changes made by final foreign tax credit regulations (TD 9882) published in the Federal Register (84 FR 69022) on December 17, 2019. The final foreign tax credit regulations provide guidance relating to the determination of the foreign tax credit under the Code, implementing statutory changes made by the TCJA. In particular, the proposed regulations would revise §1.1502-9 to remove references to the fair market value method option for interest expense apportionment, which was repealed by section 14502 of the TCJA. Relatedly, the proposed regulations would (1) update citations set forth in §§1.1502-9(a) and 1.1502-9(c)(2)(ii) and (iii), and (2) add a reference to §1.861-13. In addition, the proposed regulations would update an internal cross-reference in §1.1502-9(b)(1).

6. Section 1.1502-12(g) (deductions under section 167 of the 1954 Code) and related provisions

Section 1.1502-12(g) was added to the consolidated return regulations by final regulations (TD 7246) published in the Federal Register (38 FR 758) on January 4, 1973. Section 1.1502-12(g) provides that, in the computation of the deduction under section 167 of the 1954 Code, property does not lose its character as new property as a result of a transfer from one member to another member during a consolidated return year if certain conditions are satisfied. Since the date of those final regulations, extensive changes to the depreciation rules of the Code have made §1.1502-12(g) obsolete. See, for example, section 201 of the Economic Recovery Tax Act of 1981, Public Law 97-34, 95 Stat. 172 (August 13, 1981) (enacting section 168 of the 1954 Code, which provided the accelerated cost recovery system); section 201(a) of the Tax Reform Act of 1986 (amending section 168 of the Code, as redesignated by section 2(a) of the Tax Reform Act of 1986, to replace generally the accelerated cost recovery system with the modified accelerated cost recovery system).

As a result of the obsolescence of §1.1502-12(g) due to the above-described enacted legislation, the proposed regulations would remove that provision. Relatedly, the proposed regulations would revise §§1.57-1(b)(4)(ii) and 1.167(c)-1(a)(5) to remove cross-references to §1.1502-12(g). The proposed regulations also would remove the second sentence of §1.1502-17(a), which refers the reader to §1.1502-12(g) for the treatment of depreciable property after a transfer within the group.

7. Section 1.1502-24 (consolidated charitable contributions deduction)

As noted in part II.A.5 of this Explanation of Provisions, §1.1502-24(a) sets forth a rule to determine the amount of the consolidated charitable contributions deduction for a group. Section 1.1502-24(a)(2) includes a reference to “five percent” of the adjusted consolidated taxable income of a group, which is based on section 170(b)(2) of the 1954 Code, as that section existed prior to enactment of the Economic Recovery Tax Act of 1981. Section 263(a) of the Economic Recovery Tax Act of 1981 amended section 170(b)(2) of the 1954 Code to increase the deduction limitation for corporations from 5 percent of the taxpayer’s total income for a taxable year to 10 percent of that income.

The proposed regulations would revise §1.1502-24(a)(2) to replace the reference to “five percent” with a reference to the “percentage limitation on the total charitable contribution deduction provided in section 170(b)(2)(A).” The Treasury Department and the IRS have proposed this revision, as opposed to a reference to “10 percent” (as currently set forth in section 170(b)(2)(A) of the Code), to reduce the need to provide future statutory updates to §1.1502-24. See paragraph 9 of the Proposed Amendments to the Regulations, set forth in the NPRM (REG-101652-10) published in the Federal Register (80 FR 33211) on June 11, 2015.

8. Section 1.1502-26 (consolidated dividends received deduction)

Section 1.1502-26 provides rules for determining the consolidated DRD for the taxable year of a group. On several occasions since the publication of the original version of §1.1502-26 in 1966, Congress has enacted legislation that amended the corporate DRD sections of the 1954 Code and the Code – most recently by section 13002 of the TCJA. To update §1.1502-26 to reflect the corporate DRD provisions of the Code, the proposed regulations would revise §1.1502-26(a) to replace the reference to the 85-percent DRD (reflecting the rate set forth in section 246(b)(1) of the 1954 Code, prior to the enactment of section 611(a)(3) of the Tax Reform Act of 1986) with a reference to the limitation on the aggregate amount of dividends-received deductions described in section 246(b) of the Code.

In addition, the proposed regulations would strike the reference to section 244 of the Code in §1.1502-26(a), and the reference to section 247 of the Code in §1.1502-26(b), both of which were repealed by section 221(a)(41)(A) of Division A of the Tax Increase Prevention Act of 2014. The proposed regulations also would revise the examples in §1.1502-26(c) to reflect the updates made to §1.1502-26.

9. Section 1.1502-34 (special aggregate stock ownership rules)

Section 1.1502-34 provides that, for purposes of §§1.1502-1 through 1.1502-80, in determining the stock ownership of a member of a group in another corporation (issuing corporation) for purposes of determining the application of now-repealed section 333(b) of the 1954 Code, section 165(g)(3)(A) of the Code, section 332(b)(1) of the Code, section 351(a) of the Code, section 732(f) of the Code, or section 904(f) of the Code, in a consolidated return year, there is included stock owned by all other members of the group in the issuing corporation. Section 1.1502-34 also provides that the special rule for minority shareholders in now-repealed section 337(d) of the 1954 Code does not apply with respect to amounts received by applicable member shareholders in a liquidation of the issuing member.