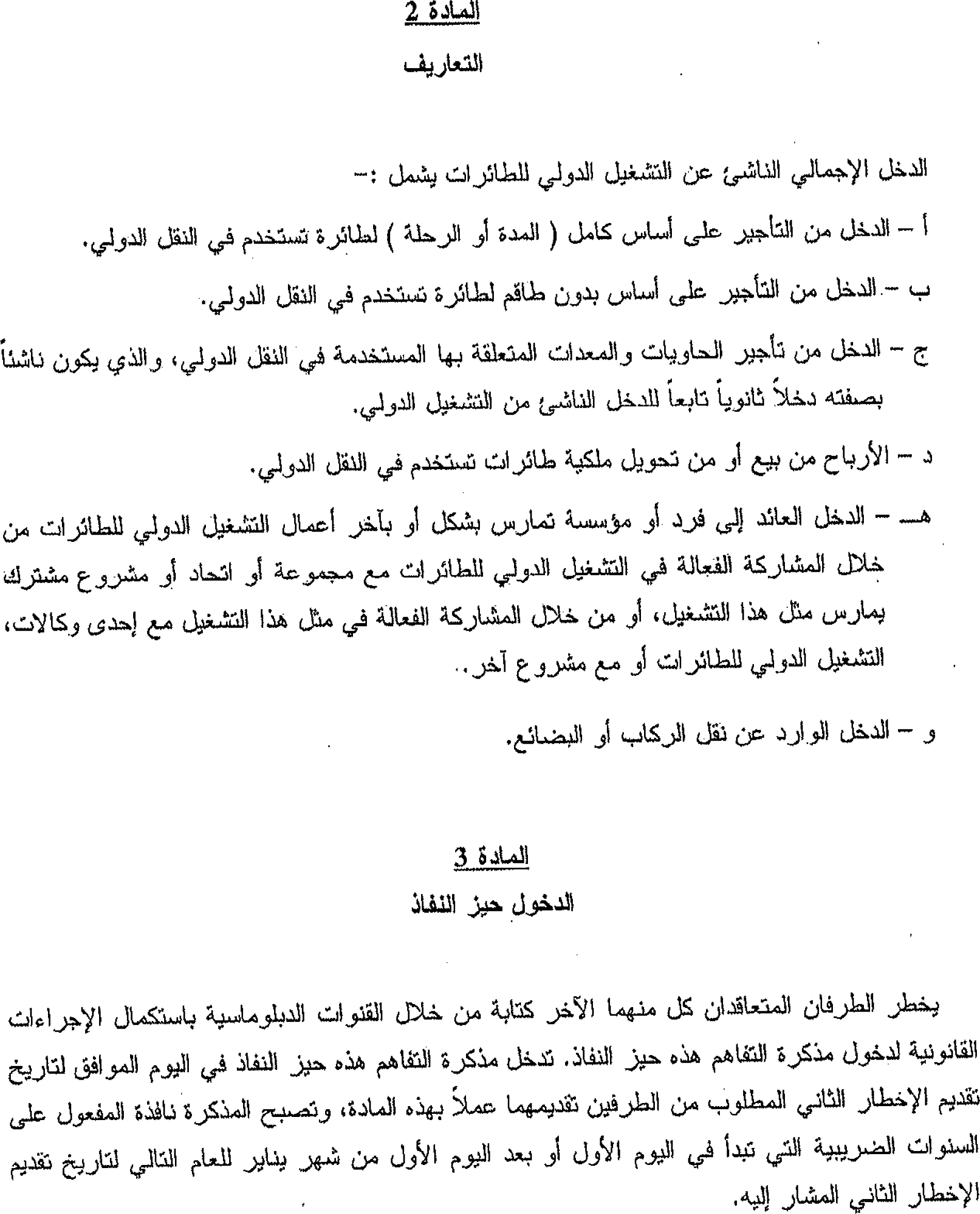

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

Internal Revenue Bulletin: 2014-23

June 2, 2014

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

REG–150760–13 REG–150760–13

Section 1.856–10 – Definition of Real Estate Investment Trust Real Property. Real estate investment trusts (REITs) have certain REIT qualification requirements. At least 75 percent of a REIT’s assets must be in real estate assets, cash and cash items, and Government securities. A real estate asset includes real property and interests in real property. These proposed regulations define real property for REIT purposes. Written or electronic comments must be received by August 12, 2014. Requests to speak and outlines of topics to be discussed at the public hearing scheduled for September 18, 2014 must be received by August 12, 2014.

Rev. Proc. 2014–32 Rev. Proc. 2014–32

This revenue procedure establishes a pilot program providing administrative relief to plan administrators and plan sponsors of certain retirement plans from the penalties otherwise applicable under §§ 6652(e) and 6692 of the Internal Revenue Code (the “Code”) for a failure to timely comply with the annual reporting requirements imposed under §§ 6047(e), 6058, and 6059 of the Code. The administrative relief provided under this revenue procedure applies only to plan administrators (as defined in § 414(g) of the Code) and plan sponsors of retirement plans that are subject to the reporting requirements of §§ 6047(e), 6058, and 6059 of the Code, but that are not subject to the reporting requirements of Title I of the Employee Retirement Income Security Act of 1974 (ERISA”). This is a one year pilot program.

Notice 2014–34 Notice 2014–34

This notice contains updates for the corporate bond weighted average interest rate for plan years beginning in May 2014; the 24-month average segment rates; the funding segment rates applicable for May 2014; and the minimum present value rates for April 2014. The rates in this notice reflect certain changes implemented by the Moving Ahead for Progress in the 21st Century Act, Public Law 112–141 (MAP–21).

Notice 2014–35 Notice 2014–35

This notice provides administrative relief from the penalties under §§ 6652(d), 6652(e), and 6692 of the Code for a failure to timely comply with certain annual reporting requirements under §§ 6047(e), 6057, 6058, and 6059. This relief applies to late filers who satisfy the requirements of this notice and the Delinquent Filer Voluntary Compliance (“DFVC”) Program administered by the Department of Labor (“DOL”) Employee Benefits Security Administration. The relief provided under this notice supersedes the relief previously provided in Notice 2002–23, 2002–1 C.B. 742.

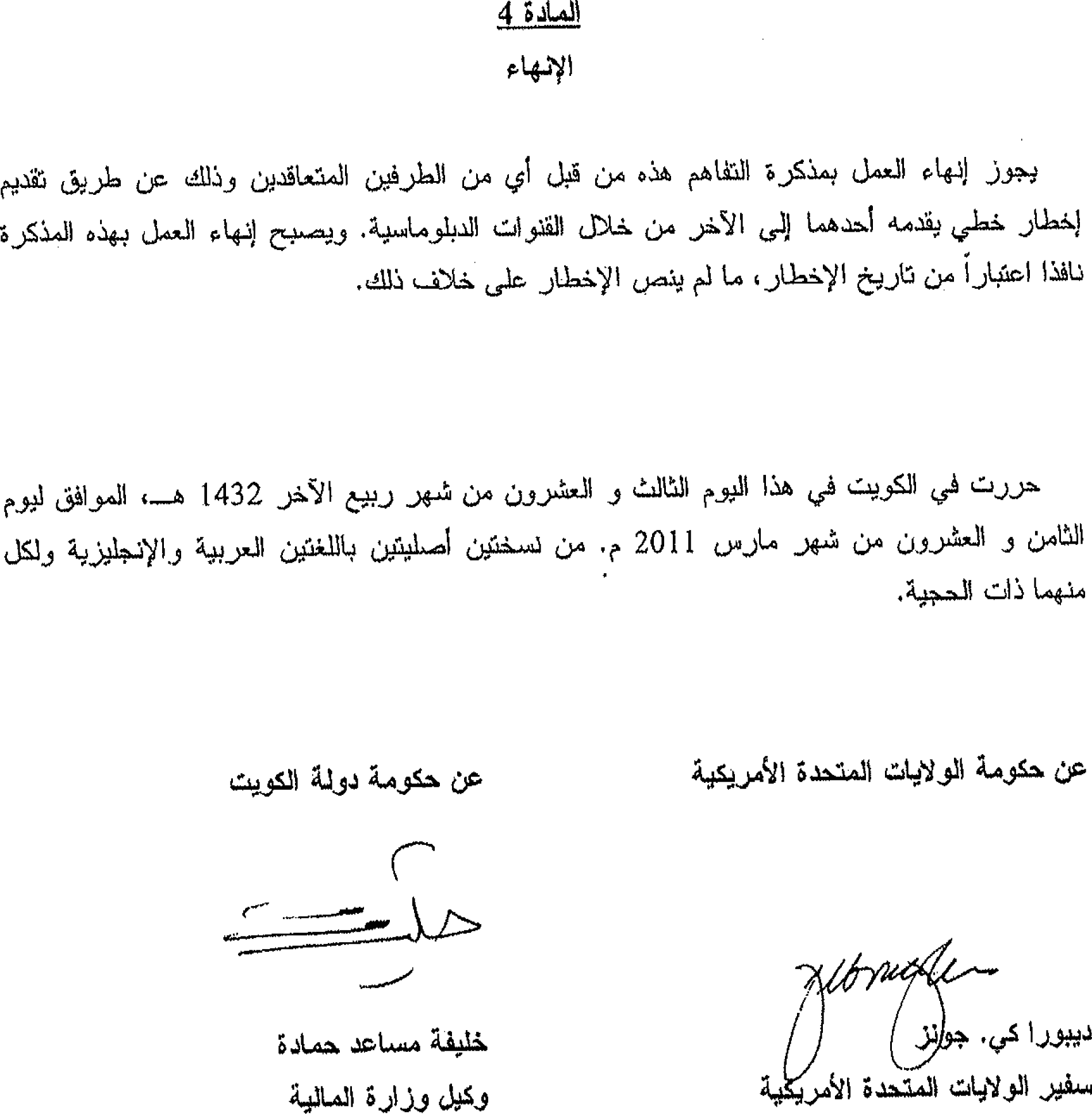

Announcement 2014–24 Announcement 2014–24

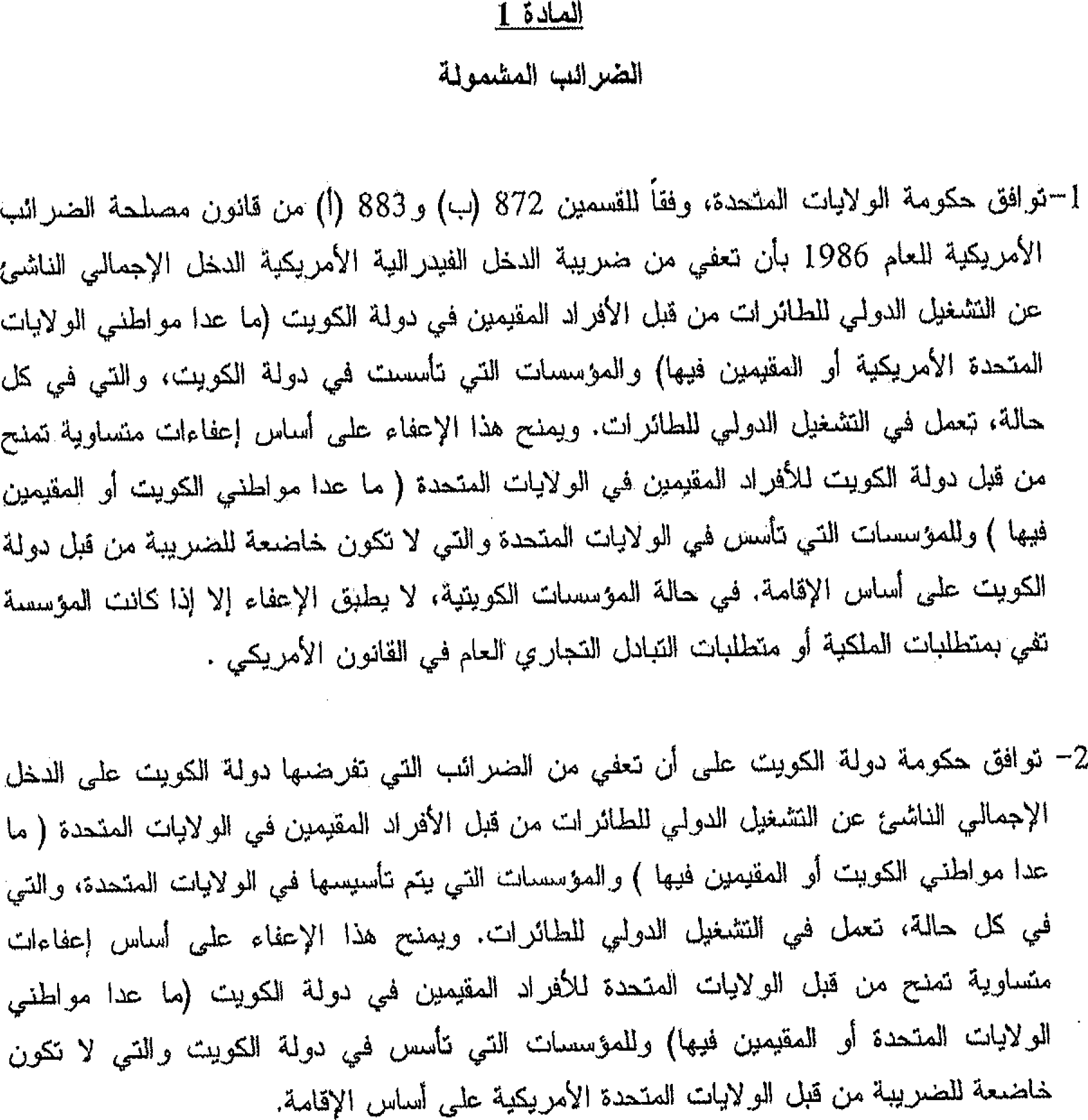

Announcement of the Memorandum of Understanding between the Government of United States of America and the Government of the State of Kuwait for the reciprocal tax exemption on income derived from the operation of aircraft and the effective date of the exemption.

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

This notice provides guidance on the corporate bond monthly yield curve (and the corresponding spot segment rates), and the 24-month average segment rates under § 430(h)(2) of the Internal Revenue Code. In addition, this notice provides guidance as to the interest rate on 30-year Treasury securities under § 417(e)(3)(A)(ii)(II) as in effect for plan years beginning before 2008, the 30-year Treasury weighted average rate under § 431(c)(6)(E)(ii)(I), and the minimum present value segment rates under § 417(e)(3)(D) as in effect for plan years beginning after 2007. These rates reflect certain changes implemented by the Moving Ahead for Progress in the 21st Century Act, Public Law 112–141 (MAP–21). MAP–21 provides that for purposes of § 430(h)(2), the segment rates are limited by the applicable maximum percentage or the applicable minimum percentage based on the average of segment rates over a 25 year period.

Generally, except for certain plans under sections 104 and 105 of the Pension Protection Act of 2006, § 430 of the Code specifies the minimum funding requirements that apply to single employer plans pursuant to § 412. Section 430(h)(2) specifies the interest rates that must be used to determine a plan’s target normal cost and funding target. Under this provision, present value is generally determined using three 24-month average interest rates (“segment rates”), each of which applies to cash flows during specified periods. To the extent provided under § 430(h)(2)(C)(iv), these segment rates are adjusted by the applicable percentage of the 25-year average segment rates for the period ending September 30 of the year preceding the calendar year in which the plan year begins. However, an election may be made under § 430(h)(2)(D)(ii) to use the monthly yield curve in place of the segment rates.

Notice 2007–81, 2007–44 I.R.B. 899, provides guidelines for determining the monthly corporate bond yield curve, and the 24-month average corporate bond segment rates used to compute the target normal cost and the funding target. Pursuant to Notice 2007–81, the monthly corporate bond yield curve derived from April 2014 data is in Table I at the end of this notice. The spot first, second, and third segment rates for the month of April 2014 are, respectively, 1.24, 4.13, and 5.15. For plan years beginning on or after January 1, 2012, the 24-month average segment rates determined under § 430(h)(2)(C)(iv) must be adjusted by the applicable percentage of the corresponding 25-year average segment rates. The 25-year average segment rates for plan years beginning in 2012, 2013, and 2014 were published in Notice 2012–55, 2012–36 I.R.B. 332, Notice 2013–11, 2013–11 I.R.B. 610, and Notice 2013–58, 2013–40 I.R.B. 294, respectively. The three 24-month average corporate bond segment rates applicable for May 2014 without adjustment, and the adjusted 24-month average segment rates taking into account the applicable percentages of the corresponding 25-year average segment rates, are as follows:

| For Plan Years Beginning In | 24-Month Average Segment Rates Not Adjusted | Adjusted 24-Month Average Segment Rates, Based on Applicable Percentage of 25-Year Average Rates | ||||||

|---|---|---|---|---|---|---|---|---|

| Applicable Month | First Segment | Second Segment | Third Segment | First Segment | Second Segment | Third Segment | ||

| 2013 | May | 2014 | 1.18 | 4.05 | 5.11 | 4.94 | 6.15 | 6.76 |

| 2014 | May | 2014 | 1.18 | 4.05 | 5.11 | 4.43 | 5.62 | 6.22 |

Generally for plan years beginning after 2007, § 431 specifies the minimum funding requirements that apply to multiemployer plans pursuant to § 412. Section 431(c)(6)(B) specifies a minimum amount for the full-funding limitation described in section 431(c)(6)(A), based on the plan’s current liability. Section 431(c)(6)(E)(ii)(I) provides that the interest rate used to calculate current liability for this purpose must be no more than 5 percent above and no more than 10 percent below the weighted average of the rates of interest on 30-year Treasury securities during the four-year period ending on the last day before the beginning of the plan year. Notice 88–73, 1988–2 C.B. 383, provides guidelines for determining the weighted average interest rate. The rate of interest on 30-year Treasury securities for April 2014 is 3.52 percent. The Service has determined this rate as the average of the daily determinations of yield on the 30-year Treasury bond maturing in February 2044. The following rates were determined for plan years beginning in the month shown below.

| For Plan Years Beginning in | 30-Year Treasury Weighted Average | Permissible Range | |||

|---|---|---|---|---|---|

| Month | Year | 90% | to | 105% | |

| May | 2014 | 3.43 | 3.09 | 3.61 | |

In general, the applicable interest rates under § 417(e)(3)(D) are segment rates computed without regard to a 24-month average. Notice 2007–81 provides guidelines for determining the minimum present value segment rates. Pursuant to that notice, the minimum present value segment rates determined for April 2014 are as follows:

| First Segment | Second Segment | Third Segment |

|---|---|---|

| 1.24 | 4.13 | 5.15 |

The principal author of this notice is Tony Montanaro of the Employee Plans, Tax Exempt and Government Entities Division. Mr. Montanaro may be e-mailed at RetirementPlanQuestions@irs.gov.

| Table I | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Monthly Yield Curve for April 2014 | |||||||||

| Derived from April 2014 Data | |||||||||

| Maturity | Yield | Maturity | Yield | Maturity | Yield | Maturity | Yield | Maturity | Yield |

| 0.5 | 0.21 | 20.5 | 4.86 | 40.5 | 5.18 | 60.5 | 5.30 | 80.5 | 5.36 |

| 1.0 | 0.41 | 21.0 | 4.87 | 41.0 | 5.19 | 61.0 | 5.30 | 81.0 | 5.36 |

| 1.5 | 0.62 | 21.5 | 4.88 | 41.5 | 5.19 | 61.5 | 5.30 | 81.5 | 5.36 |

| 2.0 | 0.84 | 22.0 | 4.90 | 42.0 | 5.20 | 62.0 | 5.30 | 82.0 | 5.36 |

| 2.5 | 1.09 | 22.5 | 4.91 | 42.5 | 5.20 | 62.5 | 5.31 | 82.5 | 5.36 |

| 3.0 | 1.34 | 23.0 | 4.92 | 43.0 | 5.20 | 63.0 | 5.31 | 83.0 | 5.36 |

| 3.5 | 1.60 | 23.5 | 4.94 | 43.5 | 5.21 | 63.5 | 5.31 | 83.5 | 5.36 |

| 4.0 | 1.85 | 24.0 | 4.95 | 44.0 | 5.21 | 64.0 | 5.31 | 84.0 | 5.37 |

| 4.5 | 2.09 | 24.5 | 4.96 | 44.5 | 5.21 | 64.5 | 5.31 | 84.5 | 5.37 |

| 5.0 | 2.32 | 25.0 | 4.97 | 45.0 | 5.22 | 65.0 | 5.32 | 85.0 | 5.37 |

| 5.5 | 2.53 | 25.5 | 4.98 | 45.5 | 5.22 | 65.5 | 5.32 | 85.5 | 5.37 |

| 6.0 | 2.74 | 26.0 | 4.99 | 46.0 | 5.23 | 66.0 | 5.32 | 86.0 | 5.37 |

| 6.5 | 2.92 | 26.5 | 5.00 | 46.5 | 5.23 | 66.5 | 5.32 | 86.5 | 5.37 |

| 7.0 | 3.10 | 27.0 | 5.01 | 47.0 | 5.23 | 67.0 | 5.32 | 87.0 | 5.37 |

| 7.5 | 3.26 | 27.5 | 5.02 | 47.5 | 5.23 | 67.5 | 5.32 | 87.5 | 5.37 |

| 8.0 | 3.42 | 28.0 | 5.03 | 48.0 | 5.24 | 68.0 | 5.33 | 88.0 | 5.37 |

| 8.5 | 3.56 | 28.5 | 5.04 | 48.5 | 5.24 | 68.5 | 5.33 | 88.5 | 5.37 |

| 9.0 | 3.69 | 29.0 | 5.04 | 49.0 | 5.24 | 69.0 | 5.33 | 89.0 | 5.37 |

| 9.5 | 3.81 | 29.5 | 5.05 | 49.5 | 5.25 | 69.5 | 5.33 | 89.5 | 5.38 |

| 10.0 | 3.91 | 30.0 | 5.06 | 50.0 | 5.25 | 70.0 | 5.33 | 90.0 | 5.38 |

| 10.5 | 4.02 | 30.5 | 5.07 | 50.5 | 5.25 | 70.5 | 5.33 | 90.5 | 5.38 |

| 11.0 | 4.11 | 31.0 | 5.08 | 51.0 | 5.26 | 71.0 | 5.33 | 91.0 | 5.38 |

| 11.5 | 4.19 | 31.5 | 5.08 | 51.5 | 5.26 | 71.5 | 5.34 | 91.5 | 5.38 |

| 12.0 | 4.27 | 32.0 | 5.09 | 52.0 | 5.26 | 72.0 | 5.34 | 92.0 | 5.38 |

| 12.5 | 4.33 | 32.5 | 5.10 | 52.5 | 5.26 | 72.5 | 5.34 | 92.5 | 5.38 |

| 13.0 | 4.40 | 33.0 | 5.10 | 53.0 | 5.27 | 73.0 | 5.34 | 93.0 | 5.38 |

| 13.5 | 4.45 | 33.5 | 5.11 | 53.5 | 5.27 | 73.5 | 5.34 | 93.5 | 5.38 |

| 14.0 | 4.50 | 34.0 | 5.12 | 54.0 | 5.27 | 74.0 | 5.34 | 94.0 | 5.38 |

| 14.5 | 4.55 | 34.5 | 5.12 | 54.5 | 5.27 | 74.5 | 5.34 | 94.5 | 5.38 |

| 15.0 | 4.59 | 35.0 | 5.13 | 55.0 | 5.28 | 75.0 | 5.34 | 95.0 | 5.38 |

| 15.5 | 4.62 | 35.5 | 5.13 | 55.5 | 5.28 | 75.5 | 5.35 | 95.5 | 5.39 |

| 16.0 | 4.66 | 36.0 | 5.14 | 56.0 | 5.28 | 76.0 | 5.35 | 96.0 | 5.39 |

| 16.5 | 4.69 | 36.5 | 5.14 | 56.5 | 5.28 | 76.5 | 5.35 | 96.5 | 5.39 |

| 17.0 | 4.71 | 37.0 | 5.15 | 57.0 | 5.28 | 77.0 | 5.35 | 97.0 | 5.39 |

| 17.5 | 4.74 | 37.5 | 5.16 | 57.5 | 5.29 | 77.5 | 5.35 | 97.5 | 5.39 |

| 18.0 | 4.76 | 38.0 | 5.16 | 58.0 | 5.29 | 78.0 | 5.35 | 98.0 | 5.39 |

| 18.5 | 4.78 | 38.5 | 5.16 | 58.5 | 5.29 | 78.5 | 5.35 | 98.5 | 5.39 |

| 19.0 | 4.80 | 39.0 | 5.17 | 59.0 | 5.29 | 79.0 | 5.35 | 99.0 | 5.39 |

| 19.5 | 4.82 | 39.5 | 5.17 | 59.5 | 5.30 | 79.5 | 5.36 | 99.5 | 5.39 |

| 20.0 | 4.84 | 40.0 | 5.18 | 60.0 | 5.30 | 80.0 | 5.36 | 100.0 | 5.39 |

This notice provides administrative relief from the penalties under §§ 6652(d), 6652(e), and 6692 of the Internal Revenue Code (the “Code”) for a failure to timely comply with certain annual reporting requirements under §§ 6047(e), 6057, 6058, and 6059. This administrative relief applies to late filers that satisfy the requirements of this notice and the Delinquent Filer Voluntary Compliance (“DFVC”) Program administered by the Department of Labor (“DOL”) Employee Benefits Security Administration. The relief provided under this notice supersedes the relief previously provided in Notice 2002–23, 2002–1 C.B. 742.

Plan administrators who fail to timely file Form 5500 series annual returns/reports can be subject to penalties under both Title I of the Employee Retirement Income Security Act of 1974 (“ERISA”) and the Code. The Secretary of Labor has the authority under section 502(c)(2) of ERISA and 29 CFR 2575.502c–2 to assess civil penalties of up to $1,100 per day against plan administrators that fail or refuse to file complete and timely annual reports. In addition, the Internal Revenue Service (the “Service”) may impose penalties under § 6652(e) against plan administrators and employers that fail to file complete and timely annual returns, as required under §§ 6058 and 6047(e) (with respect to employee stock ownership plans). Section 6652(e) generally provides that in the case of any failure to file a return or statement required under § 6058 or 6047(e), the late filer shall pay, upon notice and demand, a penalty of $25 for each day the failure continues, up to $15,000 per return or statement.

The Service may also impose penalties under §§ 6652(d) and 6692 for a failure to satisfy the reporting requirements of §§ 6057 and 6059. Section 6652(d)(1) generally provides that in the case of any failure to file an annual registration statement under § 6057(a), the late filer shall pay, upon notice and demand, a penalty of $1 for each participant with respect to whom there is a failure to file for each day the failure continues, up to $5,000 for any plan year. Section 6652(d)(2) generally provides that in the case of any failure to file a notification of change of status under § 6057(b), the late filer shall pay, upon notice and demand, a penalty of $1 for each day the failure continues, up to $1,000 for each failure. Section 6692 generally provides that in the case of any failure to file an actuarial report required by § 6059, the late filer shall pay a penalty of $1,000 for each failure.

The DFVC Program was initially adopted by DOL in 1995 and was updated in a published Federal Register notice on March 28, 2002 (67 FR 15052) (2002 DOL Notice). In order to encourage voluntary compliance with the ERISA annual reporting requirements by late filers, the DFVC Program allows plan administrators who fail to file a timely annual report to pay reduced civil penalties. Following the issuance of the 2002 DOL Notice, the Service issued Notice 2002–23. Notice 2002–23 provides that the Service will not impose penalties under §§ 6652 and 6692 (as those sections relate to the filing of a Form 5500 series return) on a person who is eligible for and satisfies the requirements of the DFVC Program with respect to the filing of a Form 5500.

DOL updated the 2002 DOL Notice by a notice published in the Federal Register on January 29, 2013 (78 FR 6135) (2013 DOL Notice). The DFVC Program was updated to reflect DOL’s final regulations mandating electronic filing of annual reports as part of the transition to a wholly electronic ERISA Filing Acceptance System (EFAST2). As revised, the DFVC Program now requires that delinquent annual reports be submitted using EFAST2.

Prior to the 2009 plan year, information required to be reported under § 6057 regarding deferred vested participants was reported on Schedule SSA (Form 5500). As part of the transition to mandatory electronic filing, however, the Schedule SSA was replaced by Form 8955–SSA, Annual Registration Statement Identifying Separated Participants With Deferred Vested Benefits. The Form 8955–SSA is now filed instead of the Schedule SSA. The Form 8955–SSA is a stand-alone form that must be filed with the Service, but not DOL. In the 2013 DOL Notice, DOL noted that filers cannot submit a Schedule SSA or Form 8955–SSA under the DFVC Program to DOL, even for 2008 and prior plan years.

The Service will not impose penalties under §§ 6652(d) and 6652(e) (as those sections relate to the filing of Form 5500, Form 5500–SF, and Form 8955–SSA) or under § 6692 (relating to the filing of actuarial reports required by § 6059) with respect to a year for which filing of such a form is required on a person who (1) is eligible for and satisfies the requirements of the DFVC Program with respect to a delinquent Form 5500 series return for such year and (2) files separately with the Service, in the form and within the time prescribed by this notice, a Form 8955–SSA with any information required to be filed under § 6057 for the year to which the DFVC filing relates (to the extent that the information has not previously been provided to the Service). Thus, for example, this notice provides relief from the penalties applicable under the Code to the late filing of Forms 5500 and 5500–SF only if any applicable Form 8955–SSA is also filed for the year at issue.

Although the Service generally encourages filers to file electronically whenever possible, relief is provided under this notice only if a Form 8955–SSA is filed on paper with the Service (including a fillable Form 8955–SSA completed online and then printed and filed on paper). The systems needed to provide relief for a delinquent Form 8955–SSA filed electronically are not currently in place. In contrast, Form 5500 series returns must be filed electronically using EFAST2 in accordance with the requirements of the DFVC Program. If a Form 8955–SSA is filed pursuant to this notice, the filer must check the box on Line C, Part I (Special extension) of the Form 8955–SSA and enter “DFVC” in the space provided on Line C.

Any Form 8955–SSA required to be filed with the Service pursuant to this notice must be filed on paper by the later of 30 calendar days after the filer completes the DFVC filing or December 1, 2014. This requirement applies with respect to any DFVC filing submitted through EFAST2 (generally, all DFVC filings after December 31, 2009), regardless of whether the filing was submitted before the issuance of this notice. For example, if a DFVC filing for a delinquent 2008 Form 5500 was submitted in 2012 and information required to be filed under § 6057 was never filed for 2008, a paper Form 8955–SSA must be filed with the Service for the 2008 plan year by no later than December 1, 2014 to qualify for the relief provided under this notice.

The relief provided under this notice applies upon a late filer’s satisfaction of the conditions of this notice. Accordingly, the late filer need not file a separate application for relief with the Service. The Service will coordinate with the DOL in determining which late filers are eligible for the relief provided under this notice.

Consistent with Section 5.04 of the 2013 DOL Notice, neither the acceptance of a filing and payment of a penalty under DFVC nor the granting of relief under this notice represents a determination by the Service as to the status of a plan or plan sponsor under the Code.

The relief under this notice is available only to the extent that a Form 5500 series return is required to be filed under Title I of ERISA. Therefore, for example, Form 5500–EZ and Form 5500–SF filers for plans without employees (as described in 29 CFR 2510.3–3(b) and (c)) are not eligible for the relief in this notice. In Rev. Proc. 2014–32, 2014–23 I.R.B. 1073, the Service has established a temporary pilot program to afford penalty relief under the Code for delinquent Form 5500 series filers that are not covered under Title I of ERISA (and has requested comments on whether the program should be permanent).

This revenue procedure establishes a temporary one-year pilot program providing administrative relief to plan administrators and plan sponsors of certain retirement plans from the penalties otherwise applicable under §§ 6652(e) and 6692 of the Internal Revenue Code (the “Code”) for a failure to timely comply with the annual reporting requirements imposed under §§ 6047(e), 6058, and 6059 of the Code. The administrative relief provided under this revenue procedure applies only to plan administrators (as defined in § 414(g) of the Code) and plan sponsors of retirement plans that are subject to the reporting requirements of §§ 6047(e), 6058, and 6059 of the Code, but that are not subject to the reporting requirements of Title I of the Employee Retirement Income Security Act of 1974 (“ERISA”). This revenue procedure also requests comments as to whether a permanent relief program should be established and, if so, how fees should be determined.

Both the Code and Title I of ERISA impose reporting requirements with respect to certain retirement plans. To minimize the filing burden on plan sponsors and plan administrators of employee benefit plans, the Internal Revenue Service (the “Service”) and the Department of Labor (the “DOL”) (as well as the Pension Benefit Guaranty Corporation) have consolidated various annual reporting requirements in the Form 5500 Series Annual Return/Report. The Form 5500 Series includes: the Form 5500, Annual Return/Report of Employee Benefit Plan; the Form 5500–SF, Short Form Annual Return/Report of Employee Benefit Plan; and the Form 5500–EZ, Annual Return of One-Participant (Owners and Their Spouses) Retirement Plan.

Plan sponsors and plan administrators who fail to file timely Form 5500 series annual returns/reports for their retirement plans may be subject to civil penalties under the Code (or under both Title I of ERISA and the Code). In particular, the Service may assess penalties under §§ 6652(e) and 6692 of the Code for the failure to satisfy the requirements for annual returns. Section 6652(e) generally provides, in part, that in the case of any failure to timely file a return or statement required under § 6058 (annual return of employee benefit plans) or § 6047(e) (returns and reports for employee stock ownership plans), the late filer shall pay, upon notice and demand, a penalty of $25 for each day the failure continues, up to $15,000 per return or statement. Section 6692 generally provides that, in the case of any failure to timely file a report required by § 6059 (actuarial report for employee benefit plans), the late filer shall pay a penalty of $1,000 for each failure. No penalty is imposed under these sections if it is shown that such failure to timely file is due to reasonable cause.

In 1995, the DOL established the Delinquent Filer Voluntary Compliance (“DFVC”) program to reduce ERISA late-filing penalties on filers of delinquent annual reports. In Notice 2002–23, 2002–1 C.B. 742, the Service determined that it would not impose the penalties under §§ 6652(c)(1), (d), (e) and 6692 (to the extent applicable) on a person who is eligible for, and satisfies the requirements of, the DFVC program with respect to the filing of a Form 5500. The relief under Notice 2002–23 was available only to filers who are required to file under both Title I of ERISA and the Code. Notice 2002–23 has been superseded by Notice 2014–35, 2014–23 I.R.B. 1072. As under Notice 2002–23, the penalty relief provided by Notice 2014–35 does not apply to a delinquent filing of a Form 5500–EZ for retirement plans that do not cover any common law employees (such as a plan under which a business owner and the owner’s spouse are the only participants). See 29 C.F.R. 2510.3–3(b) and (c).

Certain retirement plans that are not subject to Title I of ERISA are exempt from some of the annual reporting requirements if they satisfy certain criteria specified by statute or by the Service in published guidance. For example, for years beginning after 2006, section 1103 of the Pension Protection Act of 2006 (Pub. L. No. 109–280, 120 Stat. 780, 1057) provides that “one-participant plans” with assets of $250,000 or less at the end of the plan year are not required to file a Form 5500 series return/report. (The Service has determined that such plans must, however, file an annual return/report when the plan is terminated and all assets have been distributed.)

This revenue procedure provides administrative relief from the penalties imposed under §§ 6652(e) and 6692 of the Code for a failure to timely comply with the annual reporting requirements under §§ 6047(e), 6058, and 6059 of the Code. The relief applies to filers who are eligible to participate under Section 4 of this revenue procedure and who satisfy the requirements of Section 5 of this revenue procedure by no later than June 2, 2015. However, in lieu of the relief provided under this revenue procedure, filers may continue to file for the relief currently available for a failure to timely file that is due to reasonable cause.[1]

.01. General rule. The relief provided by this revenue procedure is only available to the plan administrator or plan sponsor of a retirement plan that is subject to the filing requirements of §§ 6047(e), 6058, and 6059 of the Code but is not subject to Title I of ERISA for the plan year that is delinquent. Thus, the relief under this revenue procedure is only available to the plan administrator or plan sponsor of (1) certain small business (owner-spouse) plans and plans of business partnerships (together, “one-participant plans”) and (2) certain foreign plans.

.02. One-participant plans. For purposes of this revenue procedure, a one-participant plan is a retirement plan with one or more participants that:

-

Covers only the owner of the entire business (or the owner and the owner’s spouse); or

-

Covers only one or more partners (or partners and their spouses) in a business partnership; and

-

Does not provide benefits for anyone except the owner (or the owner and the owner’s spouse) or one or more partners (or partners and their spouses).

.03. Foreign plans. The plan administrator or plan sponsor of a foreign plan (i.e., a retirement plan maintained outside the United States primarily for nonresident aliens) is eligible for relief under this revenue procedure if the employer that maintains the plan is a domestic employer or a foreign employer with income derived from sources within the United States (including foreign subsidiaries of domestic employers) that deducts contributions to the plan on its U.S. income tax return.

.04. Title I plans ineligible. A plan administrator or plan sponsor is not eligible for penalty relief under this revenue procedure if the affected retirement plan is subject to Title I of ERISA for the plan year for which a filing is delinquent. Instead, a plan administrator or plan sponsor of a Title I retirement plan may request relief from penalties under ERISA and the Code in accordance with the DFVC Program’s procedures and Notice 2014–35. Please refer to http://www.dol.gov/ebsa/ for more information regarding the DFVC Program.

.05. Penalty assessment notices. The relief provided by this revenue procedure is not available if a penalty has been assessed (i.e., if a CP 283 Notice, Penalty Charged on Your Form 5500 Return, has been issued by the Service to a plan sponsor or administrator) with respect to a delinquent return.

.01. No payment required. No penalty or other payment is required to be paid under this pilot program. However, if this temporary pilot program is replaced with a permanent program, a fee or other payment will be required. See Section 7 of this revenue procedure.

.02. Filing contents. The applicant must submit the following information to the Service in order to receive penalty relief:

(1) A complete Form 5500 Series return. The submission must include a complete Form 5500 Series Annual Return/Report, including all required schedules and attachments, for each plan year for which the applicant is seeking penalty relief under this revenue procedure. All returns submitted in accordance with this revenue procedure must be sent to the Service at the address listed in Section 5.04 below and cannot be filed through the DOL’s EFAST2 filing system. Filings sent to the DOL’s EFAST2 filing system will not be treated as submissions under this program and will continue to be subject to applicable penalties under the Code. It should be noted that, for plan years prior to 2009, some plans that were not subject to Title I of ERISA were required to file Form 5500 rather than Form 5500–EZ.

For purposes of this revenue procedure:

(a) A complete return consists of a signed, filled-out paper version of the applicable Form 5500 Series return for the specific plan year that is delinquent.

-

For returns for 2008 plan years and earlier, the specific Form 5500 Series return that was required for the plan year must be submitted. For example, if a 2005 Form 5500 should have been filed for the 2005 plan year but was not, a 2005 Form 5500 must be submitted under this program.

-

For returns for 2009 plan years and later, only the Form 5500–EZ appropriate for the plan year may be submitted. Thus, a delinquent Form 5500–SF cannot be filed for the plan year, either on paper with the Service or electronically through the EFAST2 system (even if a Form 5500–SF could have been timely filed for the plan year through EFAST2).

(b) A complete return includes all schedules applicable to the plan for the year for which the return is delinquent. For example,

-

For plan years prior to 2005, a Schedule B (Actuarial Information) was required to be included with the Form 5500 Series return for non-Title I defined benefit pension plans and certain money purchase pension plans. Accordingly, a submission for these plans for these plan years must include a Schedule B.

-

For 2005 and subsequent plan years, a Schedule B (or the successor Schedule SB (Single Employer Defined Benefit Plan Actuarial Information)) was not required to be submitted to the Service with the annual Form 5500 Series return for one-participant plans and foreign plans subject to filing under the Code and not under Title I of ERISA. Accordingly, a submission for these plans for these plan years need not include a Schedule B (or Schedule SB). However, an applicant must include in the submission a representation that the applicable annual actuarial report has been prepared (even though it is not being submitted to the Service). This statement should be attached to the applicable return in lieu of a Schedule B (or Schedule SB).

-

For plan years prior to 2005, a Schedule E (ESOP Annual Information) must be included with the Form 5500 Series return for an ESOP. Accordingly, a submission for these plans for these plan years must include a Schedule E.

(c) Applicants can obtain Form 5500 Series returns, plus required schedules, for any plan year by calling 1-800-TAX Form (1-800-829-3676). Alternatively, applicants can print out electronic versions of these forms on www.irs.gov/retirement or http://www.dol.gov/ebsa/5500main.html.

(2) Delinquent returns must be marked. For each delinquent Form 5500 Series return submitted to the Service under this revenue procedure, the applicant must mark in red letters in the top margin of the first page (above the title of the form): “Delinquent return submitted under Rev. Proc. 2014–32, Eligible for Penalty Relief.” Failure to properly mark the submitted delinquent return may cause the Service to treat the return as ineligible for the relief provided under this revenue procedure and assess all applicable penalties (unless the plan administrator or plan sponsor can establish that the failure to timely file was attributable to reasonable cause).

(3) Required Transmittal Schedule. For each delinquent return being submitted, the applicant must complete a paper copy of the Transmittal Schedule provided in the Appendix of this revenue procedure (also available at http://www.irs.gov/pub/irs-tege/appendix_a_transmittal_schedule.pdf). A completed Transmittal Schedule must be attached to the front of each delinquent return. For example, if three delinquent returns are included in the same submission, a separate Transmittal Schedule must be completed and attached to the front of each of the three returns. Failure to include a completed Transmittal Schedule as directed may cause the Service to treat the return as ineligible for the relief provided under this revenue procedure and assess all applicable penalties (unless the plan administrator or plan sponsor can establish that the failure to timely file was attributable to reasonable cause).

.03. Multiple returns. Multiple returns may be included in a single submission. Thus, if a plan has delinquent returns for more than one plan year, the returns may be included in a single submission. Similarly, delinquent returns for more than one plan may be included in a single submission. For example, if an employer maintains a defined contribution plan and a defined benefit plan, and each plan is delinquent for three plan years, the employer may include the six delinquent returns (three for each plan) in a single submission. In all cases, the requirements of Section 5.02 of this revenue procedure must be satisfied for each such return (including the attachment of a separate Transmittal Schedule to the front of each return included in the submission).

.04. Mailing address. Submissions under this revenue procedure must be mailed to different addresses depending on whether the applicant is submitting a Form 5500 or a Form 5500–EZ. In general, applicants will submit Form 5500–EZ under this program. As provided under section 5.02(1) of this Revenue Procedure, however, some applicants will be required to submit Form 5500 for 2008 and earlier plan years because these applicants were required to file Form 5500 for those years rather than Form 5500–EZ. For example, foreign plans, as defined in Section 4.03 of this Revenue Procedure, were generally required to file Form 5500 for 2008 and earlier plan years rather than the Form 5500–EZ.

Submissions of Forms 5500–EZ under this revenue procedure should be mailed to:

Internal Revenue Service

1973 North Rulon White Blvd.

Ogden, UT 84404-0020

Submissions of Forms 5500 under this revenue procedure should be mailed to:

Internal Revenue Service

Employee Plans Delinquent Filer Program

EP Classification

9350 Flair Drive

El Monte, CA 91731-2828

.05. Private delivery services. Certain private delivery services designated by the Service can be used to meet the rule that timely mailing is treated as timely filing/paying. The private delivery service can provide information on how to get written proof of the mailing date.

These eligible private delivery services include only the following:

-

DHL Express (DHL): DHL Same Day Service.

-

Federal Express (FedEx): FedEx Priority Overnight, FedEx Standard Overnight, FedEx 2 Day, FedEx International Priority, and FedEx International First.

-

United Parcel Service (UPS): UPS Next Day Air, UPS Next Day Air Saver, UPS 2nd Day Air, UPS 2nd Day Air A.M., UPS Worldwide Express Plus, and UPS Worldwide Express.

The relief provided under this revenue procedure is effective June 2, 2014 and will remain in effect until June 2, 2015. Returns submitted after June 2, 2015 will not be entitled to the relief provided by this revenue procedure. If filers are not eligible for relief under this revenue procedure, they may request relief for reasonable cause as provided in Section 3.

After this temporary pilot program ends, the Service will consider whether the pilot program should be replaced with a permanent program. The Service has determined that any permanent program that is offered will include a fee or other payment. The Service invites the public to submit comments on whether such a permanent program should be established and, if so, how fees should be determined.

Comments should be submitted to: CC:PA:LPD:PR (Rev. Proc. 2014–32), Room 5203, Internal Revenue Service, POB 7604 Ben Franklin Station, Washington, D.C. 20044. Comments may be hand delivered Monday through Friday between the hours of 8 a.m. and 4 p.m. to CC:PA:LPD:PR (Rev. Proc. 2014–32), Courier’s Desk, Internal Revenue Service, 1111 Constitution Ave., N.W., Washington, D.C. Alternatively, comments may be submitted via the Internet at Notice.comments@irscounsel.treas.gov. Please include “Rev. Proc. 2014–32” in the subject line of any electronic communication. All materials submitted will be available for public inspection and copying.

The collection of information contained in this revenue procedure has been reviewed and approved by the Office of Management and Budget in accordance with the Paperwork Reduction Act (44 U.S.C 3507) under control number 1545-0956.

An agency may not conduct or sponsor, and a person is not required to respond to, a collection of information unless the collection of information displays a valid OMB control number.

The collection of information in this revenue procedure is in the Transmittal Schedule in the Appendix. This information is required to enable the Commissioner, Tax Exempt and Government Entities Division, to evaluate this pilot program and to determine if this pilot program will be made permanent. The likely respondents are individuals and small businesses or organizations.

The estimated total annual reporting recordkeeping burden is 167 hours.

The estimated annual burden per respondent/recordkeeper is five minutes. The estimated number of respondents/recordkeepers is 2000.

The estimated frequency of responses is occasional.

Books or records relating to a collection of information must be retained as long as their contents may become material in the administration of any internal revenue law. Generally, tax returns and tax return information are confidential as required by 26 U.S.C. § 6103.

The principal drafters of this revenue procedure are Paul C. Hogan and Robert M. Walsh of the Employee Plans, Tax Exempt and Government Entities Division, and William Gibbs of the Office of the Division Counsel/Associate Chief Counsel (Tax Exempt and Government Entities). For further information regarding this revenue procedure, please e-mail Mr. Hogan or Mr. Walsh at RetirementPlanQuestions@irs.gov. For questions regarding submissions under this revenue procedure, please contact the Employee Plans’ taxpayer assistance telephone service at 1-877-829-5500 (a toll-free number).

|

[1] A request for relief due to reasonable cause may be attached to the delinquent return when the return is filed or may be filed separately. The request should state the reason why the return was late and be signed by a person in authority. See §§ 301.6652–3(b) and 301.6692–1(c) of the regulations. The request (with the delinquent return, if applicable) should be mailed to the filing address provided in the instructions for the most current Form 5500–EZ available to taxpayers.

This document contains proposed regulations that clarify the definition of real property for purposes of the real estate investment trust provisions of the Internal Revenue Code (Code). These proposed regulations provide guidance to real estate investment trusts and their shareholders. This document also provides notice of a public hearing on these proposed regulations.

Written or electronic comments must be received by August 12, 2014. Requests to speak and outlines of topics to be discussed at the public hearing scheduled for September 18, 2014 must be received by August 12, 2014.

Send submissions to: CC:PA:LPD:PR (REG–150760–13), room 5203, Internal Revenue Service, P.O. Box 7604, Ben Franklin Station, Washington, DC 20044. Submissions may be hand-delivered Monday through Friday between the hours of 8 a.m. and 4 p.m. to CC:PA:LPD:PR (REG–150760–13), Courier’s Desk, Internal Revenue Service, 1111 Constitution Avenue, N.W., Washington, DC, or sent electronically, via the Federal eRulemaking Portal at www.regulations.gov (IRS REG–150760–13). The public hearing will be held in the IRS Auditorium, Internal Revenue Building, 1111 Constitution Avenue, N.W., Washington, DC.

Concerning the proposed regulations, Andrea M. Hoffenson, (202) 317-7053, or Julanne Allen, (202) 317-6945; concerning submissions of comments, the hearing, and/or to be placed on the building access list to attend the hearing, Oluwafunmilayo (Funmi) Taylor, (202) 317-6901 (not toll-free numbers).

This document contains amendments to the Income Tax Regulations (26 CFR part 1) relating to real estate investment trusts (REITs). Section 856 of the Code defines a REIT by setting forth various requirements. One of the requirements for a taxpayer to qualify as a REIT is that at the close of each quarter of the taxable year at least 75 percent of the value of its total assets is represented by real estate assets, cash and cash items (including receivables), and Government securities. See section 856(c)(4). Section 856(c)(5)(B) defines real estate assets to include real property and interests in real property. Section 856(c)(5)(C) indicates that real property means “land or improvements thereon.” Section 1.856–3(d) of the Income Tax Regulations, promulgated in 1962, defines real property for purposes of the regulations under sections 856 through 859 as—

land or improvements thereon, such as buildings or other inherently permanent structures thereon (including items which are structural components of such buildings or structures). In addition, the term “real property” includes interests in real property. Local law definitions will not be controlling for purposes of determining the meaning of the term “real property” as used in section 856 and the regulations thereunder. The term includes, for example, the wiring in a building, plumbing systems, central heating, or central air-conditioning machinery, pipes or ducts, elevators or escalators installed in the building, or other items which are structural components of a building or other permanent structure. The term does not include assets accessory to the operation of a business, such as machinery, printing press, transportation equipment which is not a structural component of the building, office equipment, refrigerators, individual air-conditioning units, grocery counters, furnishings of a motel, hotel, or office building, etc., even though such items may be termed fixtures under local law.

The IRS issued revenue rulings between 1969 and 1975 addressing whether certain assets qualify as real property for purposes of section 856. Specifically, the published rulings describe assets such as railroad properties,[2] mobile home units permanently installed in a planned community,[3] air rights over real property,[4] interests in mortgage loans secured by total energy systems,[5] and mortgage loans secured by microwave transmission property,[6] and the rulings address whether the assets qualify as either real property or interests in real property under section 856. Since these published rulings were issued, REITs have sought to invest in various types of assets that are not directly addressed by the regulations or the published rulings, and have asked for and received letter rulings from the IRS addressing certain of these assets. Because letter rulings are limited to their particular facts and may not be relied upon by taxpayers other than the taxpayer that received the ruling, see section 6110(k)(3), letter rulings are not a substitute for published guidance. The IRS and the Treasury Department recognize the need to provide additional published guidance on the definition of real property under sections 856 through 859. This document proposes regulations that define real property for purposes of sections 856 through 859 by providing a framework to analyze the types of assets in which REITs seek to invest. These proposed regulations provide neither explicit nor implicit guidance regarding whether various types of income are described in section 856(c)(3).[7]

Consistent with section 856, the existing regulations, and published guidance interpreting those regulations, these proposed regulations define real property to include land, inherently permanent structures, and structural components. In determining whether an item is land, an inherently permanent structure, or a structural component, these proposed regulations first test whether the item is a distinct asset, which is the unit of property to which the definitions in these proposed regulations apply.

In addition, these proposed regulations identify certain types of intangible assets that are real property or interests in real property for purposes of sections 856 through 859. These proposed regulations include examples to illustrate the application of the principles of these proposed regulations to determine whether certain distinct assets are real property for purposes of sections 856 through 859.

These proposed regulations provide that each distinct asset is tested individually to determine whether the distinct asset is real or personal property. Items that are specifically listed in these proposed regulations as types of buildings and other inherently permanent structures are distinct assets. Assets and systems specifically listed in these proposed regulations as types of structural components also are treated as distinct assets. Other distinct assets are identified using the factors provided by these proposed regulations. All listed factors must be considered, and no one factor is determinative.

These proposed regulations define land to include not only a parcel of ground, but the air and water space directly above the parcel. Therefore, water space directly above the seabed is land, even though the water itself flows over the seabed and does not remain in place. Land includes crops and other natural products of land until the crops or other natural products are detached or removed from the land.

Inherently permanent structures and their structural components are real property for purposes of sections 856 through 859. These proposed regulations clarify that inherently permanent structures are structures, including buildings, that have a passive function. Therefore, if a distinct asset has an active function, such as producing goods, the distinct asset is not an inherently permanent structure under these proposed regulations. In addition to serving a passive function, a distinct asset must be inherently permanent to be an inherently permanent structure. For this purpose, permanence may be established not only by the method by which the structure is affixed but also by the weight of the structure alone.

These proposed regulations supplement the definition of inherently permanent structure by providing a safe harbor list of distinct assets that are buildings, as well as a list of distinct assets that are other inherently permanent structures. If a distinct asset is on one of these lists, either as a building or as an inherently permanent structure, the distinct asset is real property for purposes of sections 856 through 859, and a facts and circumstances analysis is not necessary. If a distinct asset is not listed as either a building or an inherently permanent structure, these proposed regulations provide facts and circumstances that must be considered in determining whether the distinct asset is either a building or other inherently permanent structure. All listed factors must be considered, and no one factor is determinative.

One distinct asset that these proposed regulations list as an inherently permanent structure is an outdoor advertising display subject to an election to be treated as real property under section 1033(g)(3). Section 1033(g)(3) provides taxpayers with an election to treat certain outdoor advertising displays[8] as real property for purposes of Chapter 1 of the Code.

These proposed regulations define a structural component as a distinct asset that is a constituent part of and integrated into an inherently permanent structure, that serves the inherently permanent structure in its passive function, and does not produce or contribute to the production of income other than consideration for the use or occupancy of space. An entire system is analyzed as a single distinct asset and, therefore, as a single structural component, if the components of the system work together to serve the inherently permanent structure with a utility-like function, such as systems that provide a building with electricity, heat, or water.[9] For a structural component to be real property under sections 856 through 859, the taxpayer’s interest in the structural component must be held by the taxpayer together with the taxpayer’s interest in the inherently permanent structure to which the structural component is functionally related. Additionally, if a distinct asset that is a structural component is customized in connection with the provision of rentable space in an inherently permanent structure, the customization of that distinct asset does not cause it to fail to be a structural component.

Under these proposed regulations, an asset or system that is treated as a distinct asset is a structural component, and thus real property for purposes of sections 856 through 859, if the asset or system is included on the safe harbor list of assets that are structural components. If an asset or system that is treated as a distinct asset is not specifically listed as a structural component, these proposed regulations provide a list of facts and circumstances that must be considered in determining whether the distinct asset or system qualifies as a structural component. No one factor is determinative.

These proposed regulations do not retain the phrase “assets accessory to the operation of a business,” which the existing regulations use to describe an asset with an active function that is not real property for purposes of the regulations under sections 856 through 859. The IRS and the Treasury Department believe that the phrase “assets accessory to the operation of a business” has created uncertainty because the existing regulations are unclear whether certain assets that are permanent structures or components thereof nevertheless fail to be real property because they are used in the operation of a business. Instead, these proposed regulations adopt an approach that considers whether the distinct asset in question either serves a passive function common to real property or serves the inherently permanent structure to which it is constituent in that structure’s passive function. On the other hand, if an asset has an active function, such as a distinct asset that produces, manufactures, or creates a product, then the asset is not real property unless the asset is a structural component that serves a utility-like function with respect to the inherently permanent structure of which it is a constituent part. Similarly, if an asset produces or contributes to the production of income other than consideration for the use or occupancy of space, then that asset is not real property. Thus, items that were assets accessory to the operation of a business under the existing regulations will continue to be excluded from the definition of real property for purposes of sections 856 through 859 either because they are not inherently permanent or because they serve an active function. These distinct assets include, for example, machinery; office, offshore drilling, testing, and other equipment; transportation equipment that is not a structural component of a building; printing presses; refrigerators; individual air-conditioning units; grocery counters; furnishings of a motel, hotel, or office building; antennae; waveguides; transmitting, receiving, and multiplex equipment; prewired modular racks; display racks and shelves; gas pumps; and hydraulic car lifts.

These proposed regulations also provide that certain intangible assets are real property for purposes of sections 856 through 859. To be real property, the intangible asset must derive its value from tangible real property and be inseparable from the tangible real property from which the value is derived. Under § 1.856–2(d)(3) the assets of a REIT are its gross assets determined in accordance with generally accepted accounting principles (GAAP). Intangibles established under GAAP when a taxpayer acquires tangible real property may meet the definition of real property intangibles. A license or permit solely for the use, occupancy, or enjoyment of tangible real property may also be an interest in real property because it is in the nature of an interest in real property (similar to a lease or easement). If an intangible asset produces, or contributes to the production of, income other than consideration for the use or occupancy of space, then the asset is not real property or an interest in real property. Thus, for example, a permit allowing a taxpayer to engage in or operate a particular business is not an interest in real property.

The terms “real property” and “personal property” appear in numerous Code provisions that have diverse contexts and varying legislative purposes. In some cases, certain types of assets are specifically designated as real property or as personal property by statute, while in other cases the statute is silent as to the meaning of those terms. Ordinarily, under basic principles of statutory construction, the use of the same term in multiple Code provisions would imply (absent specific statutory modifications) that Congress intended the same meaning to apply to that term for each of the provisions in which it appears. In the case of the terms “real property” and “personal property,” however, both the regulatory process and decades of litigation have led to different definitions of these terms, in part because taxpayers have advocated for broader or narrower definitions in different contexts.

For example, in the depreciation and (prior) investment tax credit contexts, a broad definition of personal property (and a narrow definition of real property) is ordinarily more favorable to taxpayers. A tangible asset may generally be depreciated faster if it is personal property than if it is considered real property, see section 168(c) and (g)(2)(C), and (prior) section 38 property primarily included tangible personal property and excluded a building and its structural components, see § 1.48–1(c) and (d). During decades of controversy, taxpayers sought to broaden the meaning of tangible personal property and to narrow the meanings of building and structural component in efforts to qualify for the investment tax credit or for faster depreciation. That litigation resulted in courts adopting a relatively broad definition of tangible personal property (and correspondingly narrow definition of real property) for depreciation and investment tax credit purposes.

Similarly, in the context of the Foreign Investment in Real Property Tax Act (FIRPTA), codified at section 897 of the Code, a narrower definition of real property is generally more favorable to taxpayers. Enacted in 1980, FIRPTA is intended to subject foreign investors to the same U.S. tax treatment on gains from the disposition of interests in U.S. real property that applies to U.S. investors. Accordingly, foreign investors can more easily avoid U.S. tax to the extent that the definition of real property is narrow for FIRPTA purposes. As in the depreciation and investment tax credit contexts, this situation has led to vigorous debate over the appropriate characterization of certain types of assets (such as intangible assets) that may have characteristics associated with real property but do not fall within the traditional categories of buildings and structural components. See, for example, Advance Notice of Proposed Rulemaking, Infrastructure Improvements Under Section 897, published in the Federal Register (REG–130342–08, 73 FR 64901) on October 31, 2008 (noting that taxpayers may be taking the position that a governmental permit to operate a toll bridge or toll road is not a United States real property interest for purposes of section 897 and stating that the IRS and the Treasury Department are of the view that such a permit may properly be characterized as a United States real property interest in certain circumstances). In the case of FIRPTA, however, Congress modified the definition of real property to include items of personal property that are associated with the use of real property. See section 897(c)(6)(B) (including as real property movable walls, furnishings, and other personal property associated with the use of the real property). Consequently, it is explicitly contemplated in section 897 that an item of property may be treated as a United States real property interest for FIRPTA purposes, notwithstanding that it is characterized as personal property for other purposes of the Code.

In the REIT context, taxpayers ordinarily benefit from a relatively broad definition of real property. Consequently, taxpayers have generally advocated in the REIT context for a more expansive definition of real property than applies in the depreciation and (prior) investment tax credit contexts. In drafting these regulations, the Treasury Department and the IRS have sought to balance the general principle that common terms used in different provisions should have common meanings with the particular policies underlying the REIT provisions. These proposed regulations define real property only for purposes of sections 856 through 859. The IRS and the Treasury Department request comments, however, on the extent to which the various meanings of real property that appear in the Treasury regulations should be reconciled, whether through modifications to these proposed regulations or through modifications to the regulations under other Code provisions.

The IRS and the Treasury Department view these proposed regulations as a clarification of the existing definition of real property and not as a modification that will cause a significant reclassification of property. As such, these proposed regulations are proposed to be effective for calendar quarters beginning after these proposed regulations are published as final regulations in the Federal Register. The IRS and the Treasury Department solicit comments regarding the proposed effective date.

It has been determined that this notice of proposed rulemaking is not a significant regulatory action as defined in Executive Order 12866, as supplemented by Executive Order 13653. Therefore, a regulatory assessment is not required. It also has been determined that section 553(b) of the Administrative Procedure Act (5 U.S.C. chapter 5) does not apply to these regulations, and because the regulations do not impose a collection of information on small entities, the Regulatory Flexibility Act (5 U.S.C. chapter 6) does not apply. Pursuant to section 7805(f) of the Code, this notice of proposed rulemaking has been submitted to the Chief Counsel for Advocacy of the Small Business Administration for comment on its impact on small business.

Before these proposed regulations are adopted as final regulations, consideration will be given to any written (a signed original and eight (8) copies) or electronic comments that are submitted timely to the IRS. The IRS and the Treasury Department request comments on all aspects of these proposed rules. All comments will be available for public inspection and copying at http://www.regulations.gov, or upon request.

A public hearing has been scheduled for September 18, 2014, at 10:00 a.m., in the IRS Auditorium, Internal Revenue Building, 1111 Constitution Avenue, N.W., Washington, DC. Due to building security procedures, visitors must enter at the Constitution Avenue entrance. In addition, all visitors must present photo identification to enter the building. Because of access restrictions, visitors will not be admitted beyond the immediate entrance area more than 15 minutes before the hearing starts. For information about having your name placed on the building access list to attend the hearing, see the “FOR FURTHER INFORMATION CONTACT” section of this preamble.

The rules of 26 CFR 601.601(a)(3) apply to the hearing. Persons who wish to present oral comments at the hearing must submit written or electronic comments and an outline of the topics to be discussed and the time to be devoted to each topic (signed original and eight (8) copies) by August 12, 2014. A period of ten minutes will be allotted to each person for making comments. An agenda showing the scheduling of the speakers will be prepared after the deadline for receiving outlines has passed. Copies of the agenda will be available free of charge at the hearing.

The principal authors of these regulations are Andrea M. Hoffenson and Julanne Allen, Office of Associate Chief Council (Financial Institutions and Products). However, other personnel from the IRS and the Treasury Department participated in their development.

*****

Accordingly, 26 CFR part 1 is proposed to be amended as follows:

Paragraph 1. The authority citation for part 1 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *

Par. 2. In § 1.856–3, paragraph (d) is revised to read as follows:

* * * * *

(d) Real property. See § 1.856–10 for the definition of real property.

* * * * *

Par. 3. Section 1.856–10 is added to read as follows:

(a) In general. This section provides definitions for purposes of part II, subchapter M, chapter 1 of the Internal Revenue Code (Code). Paragraph (b) of this section defines real property, which includes land as defined under paragraph (c) of this section, and improvements to land as defined under paragraph (d) of this section. Improvements to land include inherently permanent structures as defined under paragraph (d)(2) of this section, and structural components of inherently permanent structures as defined under paragraph (d)(3) of this section. Paragraph (e) of this section provides rules for determining whether an item is a distinct asset for purposes of applying the definitions in paragraphs (b), (c), and (d) of this section. Paragraph (f) of this section identifies intangible assets that are real property or interests in real property. Paragraph (g) of this section provides examples illustrating the rules of paragraphs (b) through (f) of this section.

(b) Real property. The term real property means land and improvements to land. Local law definitions are not controlling for purposes of determining the meaning of the term real property.

(c) Land. Land includes water and air space superjacent to land and natural products and deposits that are unsevered from the land. Natural products and deposits, such as crops, water, ores, and minerals, cease to be real property when they are severed, extracted, or removed from the land. The storage of severed or extracted natural products or deposits, such as crops, water, ores, and minerals, in or upon real property does not cause the stored property to be recharacterized as real property.

(d) Improvements to land—(1) In general. The term improvements to land means inherently permanent structures and their structural components.

(2) Inherently permanent structure—(i) In general. The term inherently permanent structure means any permanently affixed building or other structure. Affixation may be to land or to another inherently permanent structure and may be by weight alone. If the affixation is reasonably expected to last indefinitely based on all the facts and circumstances, the affixation is considered permanent. A distinct asset that serves an active function, such as an item of machinery or equipment, is not a building or other inherently permanent structure.

(ii) Building—(A) In general. A building encloses a space within its walls and is covered by a roof.

(B) Types of buildings. Buildings include the following permanently affixed distinct assets: houses; apartments; hotels; factory and office buildings; warehouses; barns; enclosed garages; enclosed transportation stations and terminals; and stores.

(iii) Other inherently permanent structures—(A) In general. Other inherently permanent structures serve a passive function, such as to contain, support, shelter, cover, or protect, and do not serve an active function such as to manufacture, create, produce, convert, or transport.

(B) Types of other inherently permanent structures. Other inherently permanent structures include the following permanently affixed distinct assets: microwave transmission, cell, broadcast, and electrical transmission towers; telephone poles; parking facilities; bridges; tunnels; roadbeds; railroad tracks; transmission lines; pipelines; fences; in-ground swimming pools; offshore drilling platforms; storage structures such as silos and oil and gas storage tanks; stationary wharves and docks; and outdoor advertising displays for which an election has been properly made under section 1033(g)(3).

(iv) Facts and circumstances determination. If a distinct asset (within the meaning of paragraph (e) of this section) does not serve an active function as described in paragraph (d)(2)(iii)(A) of this section, and is not otherwise listed in paragraph (d)(2)(ii)(B) or (d)(2)(iii)(B) of this section or in guidance published in the Internal Revenue Bulletin (see § 601.601(d)(2)(ii) of this chapter), the determination of whether that asset is an inherently permanent structure is based on all the facts and circumstances. In particular, the following factors must be taken into account:

(A) The manner in which the distinct asset is affixed to real property;

(B) Whether the distinct asset is designed to be removed or to remain in place indefinitely;

(C) The damage that removal of the distinct asset would cause to the item itself or to the real property to which it is affixed;

(D) Any circumstances that suggest the expected period of affixation is not indefinite (for example, a lease that requires or permits removal of the distinct asset upon the expiration of the lease); and

(E) The time and expense required to move the distinct asset.

(3) Structural components—(i) In general. The term structural component means any distinct asset (within the meaning of paragraph (e) of this section) that is a constituent part of and integrated into an inherently permanent structure, serves the inherently permanent structure in its passive function, and, even if capable of producing income other than consideration for the use or occupancy of space, does not produce or contribute to the production of such income. If interconnected assets work together to serve an inherently permanent structure with a utility-like function (for example, systems that provide a building with electricity, heat, or water), the assets are analyzed together as one distinct asset that may be a structural component. Structural components are real property only if the interest held therein is included with an equivalent interest held by the taxpayer in the inherently permanent structure to which the structural component is functionally related. If a distinct asset is customized in connection with the rental of space in or on an inherently permanent structure to which the asset relates, the customization does not affect whether the distinct asset is a structural component.

(ii) Types of structural components. Structural components include the following distinct assets and systems: wiring; plumbing systems; central heating and air-conditioning systems; elevators or escalators; walls; floors; ceilings; permanent coverings of walls, floors, and ceilings; windows; doors; insulation; chimneys; fire suppression systems, such as sprinkler systems and fire alarms; fire escapes; central refrigeration systems; integrated security systems; and humidity control systems.

(iii) Facts and circumstances determination. If a distinct asset (within the meaning of paragraph (e) of this section) is not otherwise listed in paragraph (d)(3)(ii) of this section or in guidance published in the Internal Revenue Bulletin (see § 601.601(d)(2)(ii) of this chapter), the determination of whether the asset is a structural component is based on all the facts and circumstances. In particular, the following factors must be taken into account:

(A) The manner, time, and expense of installing and removing the distinct asset;

(B) Whether the distinct asset is designed to be moved;

(C) The damage that removal of the distinct asset would cause to the item itself or to the inherently permanent structure to which it is affixed;

(D) Whether the distinct asset serves a utility-like function with respect to the inherently permanent structure;

(E) Whether the distinct asset serves the inherently permanent structure in its passive function;

(F) Whether the distinct asset produces income from consideration for the use or occupancy of space in or upon the inherently permanent structure;

(G) Whether the distinct asset is installed during construction of the inherently permanent structure;

(H) Whether the distinct asset will remain if the tenant vacates the premises; and

(I) Whether the owner of the real property is also the legal owner of the distinct asset.

(e) Distinct asset—(1) In general. A distinct asset is analyzed separately from any other assets to which the asset relates to determine if the asset is real property, whether as land, an inherently permanent structure, or a structural component of an inherently permanent structure.

(2) Facts and circumstances. The determination of whether a particular separately identifiable item of property is a distinct asset is based on all the facts and circumstances. In particular, the following factors must be taken into account:

(i) Whether the item is customarily sold or acquired as a single unit rather than as a component part of a larger asset;

(ii) Whether the item can be separated from a larger asset, and if so, the cost of separating the item from the larger asset;

(iii) Whether the item is commonly viewed as serving a useful function independent of a larger asset of which it is a part; and

(iv) Whether separating the item from a larger asset of which it is a part impairs the functionality of the larger asset.

(f) Intangible assets—(1) In general. If an intangible asset, including an intangible asset established under generally accepted accounting principles (GAAP) as a result of an acquisition of real property or an interest in real property, derives its value from real property or an interest in real property, is inseparable from that real property or interest in real property, and does not produce or contribute to the production of income other than consideration for the use or occupancy of space, then the intangible asset is real property or an interest in real property.

(2) Licenses and permits. A license, permit, or other similar right solely for the use, enjoyment, or occupation of land or an inherently permanent structure that is in the nature of a leasehold or easement generally is an interest in real property. A license or permit to engage in or operate a business generally is not real property or an interest in real property because it produces or contributes to the production of income other than consideration for the use or occupancy of space.

(g) Examples. The following examples demonstrate the rules of this section. Examples 1 and 2 illustrate the definition of land as provided in paragraph (c) of this section. Examples 3 through 10 illustrate the definition of improvements to land as provided in paragraph (d) of this section. Finally, Examples 11 through 13 illustrate whether certain intangible assets are real property or interests in real property as provided in paragraph (f) of this section.

Example 1. Natural products of land. A is a real estate investment trust (REIT). REIT A owns land with perennial fruit-bearing plants. REIT A leases the fruit-bearing plants to a tenant on a long-term triple net lease basis and grants the tenant an easement on the land. The unsevered plants are natural products of the land and are land within the meaning of paragraph (c) of this section. Fruit from the plants is harvested annually. Upon severance from the land, the harvested fruit ceases to qualify as land. Storage of the harvested fruit upon or within real property does not cause the harvested fruit to be real property.

Example 2. Water space superjacent to land. REIT B leases a marina from a governmental entity. The marina is comprised of U-shaped boat slips and end ties. The U-shaped boat slips are spaces on the water that are surrounded by a dock on three sides. The end ties are spaces on the water at the end of a slip or on a long, straight dock. REIT B rents the boat slips and end ties to boat owners. The boat slips and end ties are water space superjacent to land that is land within the meaning of paragraph (c) of this section and, therefore, are real property.

Example 3. Indoor sculpture. (i) REIT C owns an office building and a large sculpture in the atrium of the building. The sculpture measures 30 feet tall by 18 feet wide and weighs five tons. The building was specifically designed to support the sculpture, which is permanently affixed to the building by supports embedded in the building’s foundation. The sculpture was constructed within the building. Removal would be costly and time consuming and would destroy the sculpture. The sculpture is reasonably expected to remain in the building indefinitely. The sculpture does not manufacture, create, produce, convert, transport, or serve any similar active function.

(ii) When analyzed to determine whether it is an inherently permanent structure using the factors provided in paragraph (d)(2)(iv) of this section, the sculpture—

(A) Is permanently affixed to the building by supports embedded in the building’s foundation;

(B) Is not designed to be removed and is designed to remain in place indefinitely;

(C) Would be damaged if removed and would damage the building to which it is affixed;

(D) Will remain affixed to the building after any tenant vacates the premises and will remain affixed to the building indefinitely; and

(E) Would require significant time and expense to move.

(iii) The factors described in this paragraph (g) Example 3 (ii)(A) through (ii)(E) all support the conclusion that the sculpture is an inherently permanent structure within the meaning of paragraph (d)(2) of this section and, therefore, is real property.

Example 4. Bus shelters. (i) REIT D owns 400 bus shelters, each of which consists of four posts, a roof, and panels enclosing two or three sides. REIT D enters into a long-term lease with a local transit authority for use of the bus shelters. Each bus shelter is prefabricated from steel and is bolted to the sidewalk. Bus shelters are disassembled and moved when bus routes change. Moving a bus shelter takes less than a day and does not significantly damage either the bus shelter or the real property to which it was affixed.

(ii) The bus shelters are not enclosed transportation stations or terminals and do not otherwise meet the definition of a building in paragraph (d)(2)(ii) of this section nor are they listed as types of other inherently permanent structures in paragraph (d)(2)(iii)(B) of this section.