)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

- HIGHLIGHTS OF THIS ISSUE

- Part III

- Section 45J Credit for Production of Electricity from Advanced Nuclear Power Facilities

- Determination of Housing Cost Amounts Eligible for Exclusion or Deduction for 2023

- Definition of Terms

- Numerical Finding List1

- Finding List of Current Actions on Previously Published Items1

- How to get the Internal Revenue Bulletin

Internal Revenue Bulletin: 2023-13

March 27, 2023

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

Notice 2023-23 provides guidance to financial institutions on reporting required minimum distributions (RMD) for 2023 after the amendment to section 401(a)(9) of the Internal Revenue Code made by Section 107, Division T of the Consolidated Appropriations Act, 2023, P.L. 117-328 (the SECURE 2.0 Act). Pursuant to Notice 2002-27, if an IRA owner has an RMD due for 2023, the financial institution that maintains the IRA must provide a statement by January 31, 2023, informing the IRA owner of the amount due (or an offer to calculate such amount) and the date by which the RMD must be distributed. Prior to the SECURE 2.0 Act, this statement would have been required for all IRA owners who will attain age 72 in 2023 (the year for which the first RMD is due). However, after the Act, the first RMD will be due for the year in which the IRA owner attains age 73. This notice provides that if the RMD statement is provided in the year in which the IRA owner attains age 72, the IRS will not consider such statement to be incorrect provided the financial institution notifies the IRA owner no later than April 28, 2023, that no RMD is due for 2023.

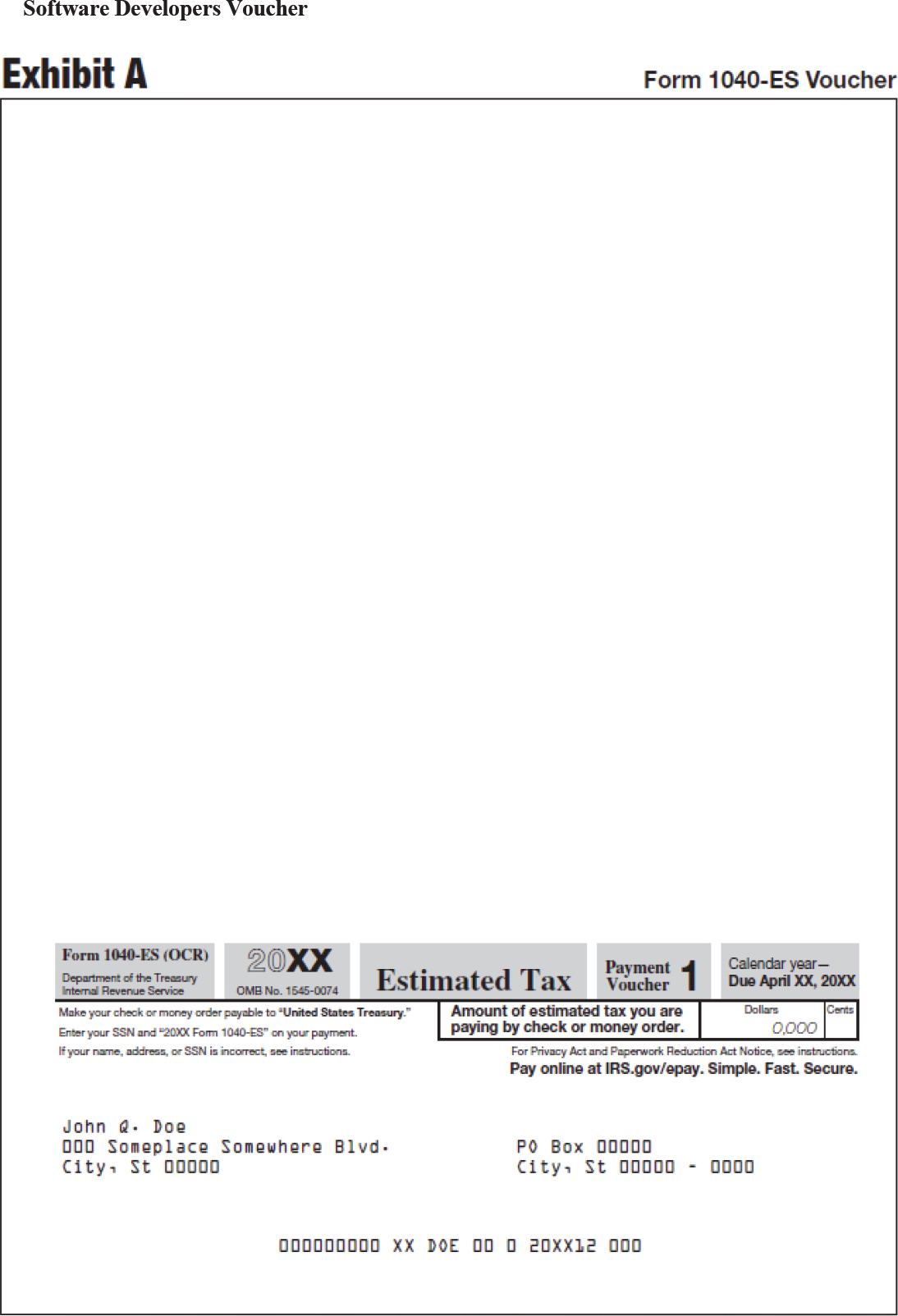

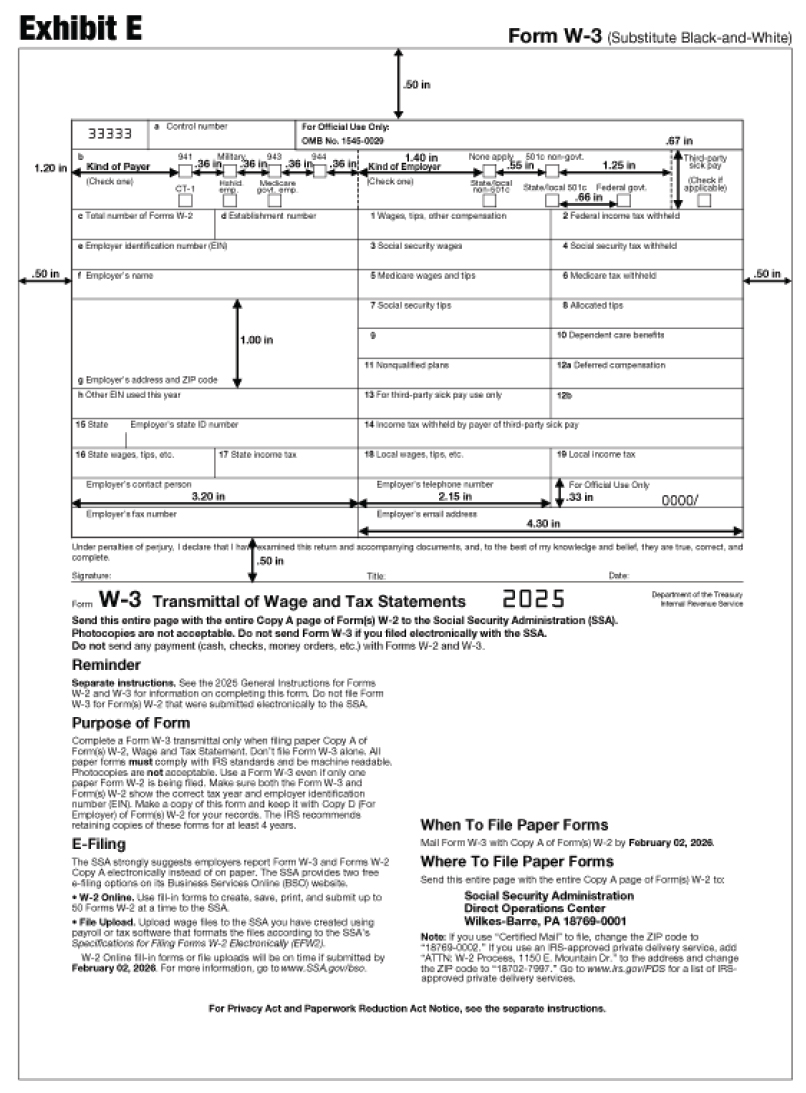

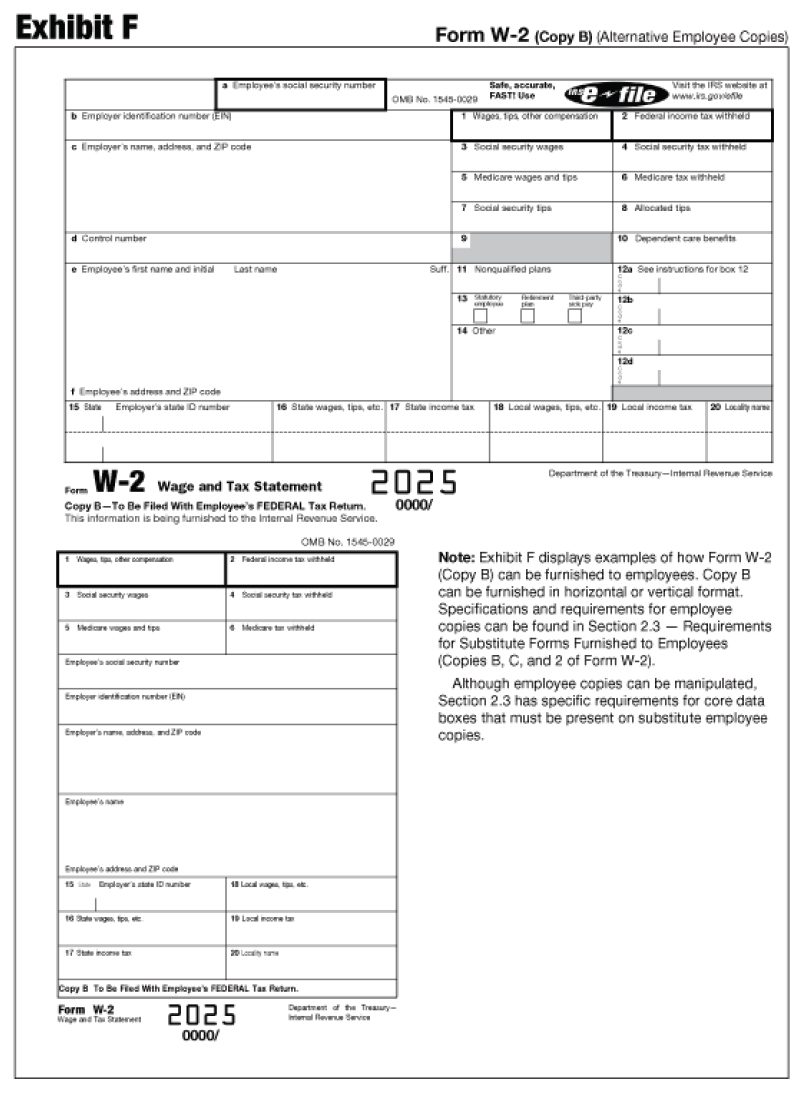

General Rules and Specifications for Substitute Form 941, Schedule B (Form 941), Schedule D (Form 941), Schedule R (Form 941), and Form 8974.

This revenue procedure provides general rules and specifications from the IRS for paper and computer-generated substitutes for Form 941; Schedule B (Form 941); Schedule D (Form 941); Schedule R (Form 941); and Form 8974. This revenue procedure supersedes Revenue Procedure 2022-15, 2022-13 I.R.B. 908.

NOTE. This revenue procedure will be reproduced as the next revision of IRS Publication 4436, General Rules and Specifications for Substitute Form 941, Schedule B (Form 941), Schedule D (Form 941), Schedule R (Form 941), and Form 8974.

This revenue procedure modifies and supersedes both Rev. Proc. 2016-33 and Rev. Proc. 2017-14. It addresses the procedures for applying to be certified as a Certified Professional Employer Organization (CPEO), the requirements for a CPEO to remain certified, and the procedures relating to suspension and revocation of CPEO certification.

26 CFR 301.7705: Applying for and maintaining certification as a certified professional employer organization.

This notice provides the general rules for determining the credit for production from advanced nuclear power facilities under § 45J (§ 45J credit) and that the amount of the unutilized national megawatt capacity limitation (NMCL) available for allocation is 6,000 megawatts. This notice also provides the procedures for taxpayers to apply for allocations of, and that the Internal Revenue Service (IRS) will use to allocate, the unutilized NMCL to facilities that the Department of Energy previously certified as an “advanced nuclear facility” under Notice 2013-68, 2013-46 I.R.B. 501. In addition, the notice provides the procedures for a “qualified public entity” to elect to transfer all or a portion of the § 45J credit to an “eligible project partner.” Finally, the notice requests comments on issues impacting the § 45J credit.

Notice 2023-26 provides for adjustments to the limitation on housing expenses for purposes of section 911 of the Internal Revenue Code for the 2023 tax year. These adjustments are made on the basis of geographic differences in housing costs relative to housing costs in the United States. If the limitation on housing expenses is higher for the 2023 tax year than the adjusted limitations on housing expenses provided in Notice 2022-10, qualified taxpayers may apply the adjusted limitations in this notice for the 2023 tax year to their 2022 tax year.

This revenue procedure provides indexing adjustments for the applicable dollar amounts under section 4980H(c)(1) and (b)(1) of the Internal Revenue Code. These indexed amounts are used to calculate the employer shared responsibility payments under section 4980H(a) and (b)(1), respectively.

26 CFR 601.601: Rules and Regulations.

(Also Part I, §§ 4980H; 54.4980H)

Generally, U.S. citizens or resident aliens living and working abroad are taxed on their worldwide income. However, if their tax home is in a foreign country and they meet either the bona fide residence test or the physical presence test, they can choose to exclude from their income a limited amount of their foreign earned income (up to $120,000 for 2022). Both the bona fide residence test and the physical presence test contain minimum time requirements. Revenue Procedure 2023-19 provides a waiver under section 911(d)(4) for the time requirements for individuals electing to exclude their foreign earned income who must leave a foreign country because of war, civil unrest, or similar adverse conditions in that country. Rev. Proc. 2023-19 adds Ethiopia, Iraq, Ukraine, Belarus, China, and Mali to the list of waiver countries for tax year 2022 for which the minimum time requirements are waived.

26 CFR 1.911-2: Qualified Individuals.

(Also: Part I, § 911.)

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

This notice provides guidance to financial institutions on reporting required minimum distributions (RMDs) for 2023 after the amendment to section 401(a)(9) of the Internal Revenue Code made by the Consolidated Appropriations Act, 2023, P. L. 117-328 (the Act).

The Act was enacted on December 29, 2022. Division T of the Act, titled “SECURE 2.0 Act of 2022” (SECURE 2.0 Act), included a number of retirement savings provisions. Section 107 of the SECURE 2.0 Act amended section 401(a)(9)(C) of the Code to delay the required beginning date applicable to section 401(a) plans and other eligible retirement plans described in section 402(c)(8), including individual retirement accounts and annuities (IRAs). For an IRA owner who attains age 72 after December 31, 2022, and age 73 before January 1, 2033, the new required beginning date (that is, the date by which RMDs must begin) is April 1 of the calendar year following the calendar year in which the individual attains age 73, rather than April 1 of the calendar year following the calendar year in which the individual attains age 72.

This amendment to section 401(a)(9)(C) is effective for distributions required to be made after December 31, 2022, with respect to individuals who will attain age 72 after that date. As a result of this amendment, IRA owners who will attain age 72 in 2023 (that is, individuals born in 1951) will have a required beginning date of April 1, 2025, rather than April 1, 2024. This delay in the required beginning date means that these IRA owners (who, prior to enactment of the SECURE 2.0 Act, would have been required to take minimum distributions from their IRAs for 2023) will have no RMD due from their IRAs for 2023.

If an IRA owner has an RMD due for 2023, the financial institution that is the trustee, custodian, or issuer maintaining the IRA must file a 2022 Form 5498 (IRA Contribution Information) by May 31, 2023, and indicate by a check in Box 11 that an RMD is required for 2023. The financial institution may also choose to provide further information in Box 12a (RMD Date) and Box 12b (RMD Amount). Additionally, under Notice 2002-27, 2002-1 CB 814, if an IRA owner has an RMD due for 2023, the financial institution must furnish a statement to the IRA owner by January 31, 2023, that informs the IRA owner of the date by which the RMD must be distributed, and either provides the amount of the RMD or offers to calculate that amount upon request (RMD statement).

For IRA owners who will attain age 72 in 2023, the RMD statement required under Notice 2002–27 should not be sent, and the 2022 Form 5498 should not include a check in Box 11 or any entries in Box 12a or 12b. However, in recognition of the short amount of time that financial institutions have had to change their systems for furnishing the RMD statement since the enactment of the SECURE 2.0 Act, relief is being provided with respect to this reporting. Under this relief, the Internal Revenue Service (IRS) will not consider an RMD statement provided to an IRA owner who will attain age 72 in 2023 to have been provided incorrectly if the IRA owner is notified by the financial institution no later than April 28, 2023, that no RMD is actually required for 2023.

The SECURE 2.0 Act did not change the required beginning date for IRA owners who attained age 72 prior to January 1, 2023. To reduce misunderstanding among IRA owners, the IRS encourages all financial institutions, in communicating these RMD changes, to remind IRA owners who attained age 72 in 2022, and have not yet taken their 2022 RMDs, that they are still required to take those distributions by April 1, 2023.

.01 This notice provides guidance under § 45J of the Internal Revenue Code (Code), relating to the credit for the production of electricity from advanced nuclear power facilities (§ 45J credit). In response to the amendments to certain requirements for the § 45J credit made by § 40501 of the Bipartisan Budget Act of 2018 (2018 Act), Public. Law. 115-123, Div. D, Title I, 132 Stat. 64, 153 (February 9, 2018), this notice provides: (i) guidance for computing the § 45J credit; (ii) the amount of the unutilized national megawatt capacity limitation (NMCL) (as defined in § 45J(b)(5)(B)); (iii) the procedures for taxpayers to apply for allocations of, and that the Internal Revenue Service (IRS) will use to allocate, the unutilized NMCL solely with respect to facilities that the Department of Energy (DOE) previously certified as “advanced nuclear facilities” (as defined in § 45J(d)(2)) under Notice 2013-68, 2013-46 I.R.B. 501; and (iv) the procedures for a “qualified public entity” (as defined in § 45J(e)(2)(A)) to elect, pursuant to § 45J(e), to transfer the § 45J credit to an “eligible project partner” (as defined in § 45J(e)(2)(B)). This notice also requests public comment on topics related to the § 45J credit that may require guidance.

.02 The Department of the Treasury (Treasury Department) and the IRS intend to issue additional guidance regarding the procedures by which any unutilized NMCL will be allocated to a facility that did not receive a certification from the DOE as an “advanced nuclear facility” under Notice 2013-68.

.01 Section 45J was enacted by § 1306 of the Energy Policy Act of 2005, Public Law 109-58, Title XIII, 119 Stat. 594, 997 (August 8, 2005). Subject to limitations under § 45J(b) and (c), a taxpayer may be allowed a § 45J credit of 1.8 cents for each kilowatt hour of electricity (1) that the taxpayer produces at an advanced nuclear power facility during the eight-year period beginning on the date the facility is placed in service and (2) that the taxpayer sells to an unrelated person during the taxable year (qualifying electricity). See § 45J(a).

.02 Under § 45J(d)(1), an “advanced nuclear power facility” is (i) any nuclear facility the reactor design for which is approved by the Nuclear Regulatory Commission (NRC) after December 31, 1993 (and such design or a substantially similar design of comparable capacity was not approved on or before that date), (ii) that is owned by the taxpayer, and (iii) uses nuclear energy to produce electricity. See § 45J(d).

.03 On May 1, 2006, the Treasury Department and the IRS published Notice 2006-40, 2006-18 I.R.B. 855, to provide guidance on the § 45J credit. Specifically, Notice 2006-40 specified the method that the IRS would use to allocate the NMCL and prescribed the application process by which taxpayers could request such an allocation. The notice also provided guidance on the requirement that electricity be sold to an unrelated person and on the effect of grants, tax-exempt bonds, subsidized energy financing, and other credits.

.04 On November 12, 2013, the Treasury Department and the IRS published Notice 2013-68, which modified and superseded Notice 2006-40. Notice 2013-68 generally republished the guidance contained in Notice 2006-40, but also provided a new streamlined application process allowing an applicant to submit a single application only to the IRS. The IRS would then obtain necessary certification from the DOE. In addition, Notice 2013-68 provided guidance on the allocation rules for facilities that are directly or indirectly owned by more than one person and the time for filing an application with the NRC.

.05 As originally enacted in 2005, § 45J(d)(1) required all advanced nuclear power facilities to be placed in service before January 1, 2021, to be eligible for a § 45J credit. Accordingly, section 6 of Notice 2013-68 provided that the amount of the NMCL allocated to a facility under Notice 2013-68 will be withdrawn if the facility is not placed in service before January 1, 2021, or if the DOE informs the IRS that the DOE certification for the facility has been withdrawn. However, effective for taxable years beginning after its February 9, 2018, date of enactment, § 40501 of the 2018 Act added new § 45J(b)(5) to the Code, which, in part, eliminates the requirement for a facility receiving an allocation of unutilized NMCL pursuant to § 45J(b)(5) to be placed in service before January 1, 2021, to qualify as an advanced nuclear power facility.

.06 Under § 45J(b)(1) and (3), a taxpayer may be allowed a § 45J credit for qualifying electricity only if an amount of NMCL has been allocated to the facility, in the manner prescribed by the Secretary of the Treasury or her delegate (Secretary).1 The aggregate amount of NMCL allocated by the Secretary cannot exceed 6,000 megawatts. See § 45J(b)(2).

.07 As added by § 40501 of the 2018 Act, § 45J(b)(5)(A) directs the Secretary to allocate any unutilized NMCL (as defined in § 45J(b)(5)(B)) as rapidly as is practicable after December 31, 2020, as follows: (i) first to facilities placed in service on or before December 31, 2020, to the extent that such facilities did not receive an allocation equal to their full nameplate capacity under the procedures provided in Notice 2013-68, and (ii) then to facilities placed in service after December 31, 2020, in the order in which such facilities are placed in service. Section 45J(b)(5)(B) defines the term “unutilized NMCL” as the excess (if any) of 6,000 megawatts over the aggregate amount of NMCL allocated by the Secretary before January 1, 2021, reduced by any amount of such limitation that was allocated to a facility that was not placed in service before January 1, 2021. Under § 45J(b)(5)(C), any allocation of the unutilized NMCL is treated for purposes of the § 45J credit in the same manner as an allocation of the NMCL.

.08 The 2018 Act also added new § 45J(e) to the Code effective for taxable years beginning after February 9, 2018. Section 45J(e) permits a “qualified public entity” to make an election for any taxable year with respect to all or any portion of its § 45J credits to transfer such credits to one or more eligible project partners specified in the election. With respect to any § 45J credits transferred by a qualified public entity to an eligible project partner, the credit must be taken into account in the first taxable year of the eligible project partner ending with, or after, the qualified public entity’s taxable year with respect to which the credit was determined.

.09 Section 45J(e)(2)(A) defines the term “qualified public entity” to mean (i) a Federal, State, or local government entity, or any political subdivision, agency, or instrumentality thereof; (ii) a mutual or cooperative electric company described in § 501(c)(12) or § 1381(a)(2) of the Code; or (iii) a not-for-profit electric utility which had or has received a loan or loan guarantee under the Rural Electrification Act of 1936.

.10 Section 45J(e)(2)(B) defines the term “eligible project partner” to mean any person who (i) is responsible for, or participates in, the design or construction of the advanced nuclear power facility to which the § 45J credit relates; (ii) participates in the provision of the nuclear steam supply system to such facility; (iii) participates in the provision of nuclear fuel to such facility; (iv) is a financial institution providing financing for the construction or operation of such facility; or (v) has an ownership interest in such facility.

.11 In the case of a § 45J credit determined at the partnership level, a qualified public entity is treated as the taxpayer with respect to its distributive share of the § 45J credit, and the term “eligible project partner” includes any partner of the partnership. See § 45J(e)(3)(A).

.12 Section 38(b)(21) includes the § 45J credit as a current year business credit. Section 39(a)(1) provides, in part, that if the amount of the current year business credit for the taxable year exceeds the amount of the limitation imposed by § 38(c) for the taxable year (unused credit year), the excess results in a 1-year business credit carryback to the taxable year preceding the unused credit year, and a business credit carryforward to each of the twenty (20) taxable years following the unused credit year. Section 39(a)(2)(A) provides that the entire amount of the unused credit for an unused credit year is carried to the earliest of the twenty-one (21) taxable years to which the credit may be carried. Section 39(a)(2)(B) provides that the amount of the unused credit for the unused credit year is carried to each of the other twenty (20) taxable years to the extent that such unused credit may not be taken into account under § 38(a) for a prior taxable year because of the limitations of § 39(b) and (c).

.01 In general. Under § 45J(a), (b)(1), and (c), the § 45J credit allowed to a taxpayer for a taxable year with respect to qualifying electricity is the lesser of:

(1) the tentative credit for the facility for the taxable year (determined under section 3.02(1) of this notice) multiplied by the taxpayer’s credit percentage (determined under section 3.02(2) of this notice), or

(2) $125,000,000 per 1,000 megawatts of the facility limitation determined under section 5.03(1) and (2) of this notice that is allocated to the taxpayer under section 5.03(3), (4), and (5) of this notice.

.02 Tentative credit; credit percentage

(1) A facility’s tentative credit for the taxable year is equal to 1.8 cents multiplied by the kilowatt hours of qualifying electricity.

(2) The credit percentage for each taxpayer that has been allocated all or part of the amount of the facility limitation is determined by dividing the facility limitation that is allocated to the taxpayer under section 5.03(3), (4), and (5) of this notice by the nameplate capacity of the facility.

.03 Credit determination for partnerships and S corporations. If a facility is owned by a partnership or S corporation, then the partnership or S corporation, and not the partners or shareholders, will be treated as the taxpayer that owns the facility for the purposes of this notice. In such cases, the § 45J credit must be allocated to the partners or shareholders in accordance with § 1.704-1(b)(4)(ii) of the Income Tax Regulations, in the case of partnerships, or § 1.1366-1(a)(2)(v) of the Income Tax Regulations, in the case of S corporations. If the facility is owned through an organization that has made a valid election under § 761(a) of the Code (§ 761(a) election), each member’s undivided ownership share in the facility will be treated for purposes of this notice as a separate facility owned by such member.

.04 Sale of Electricity to Unrelated Person. The § 45J credit is allowed only for qualifying electricity that the taxpayer produces and sells to an unrelated person, as defined in § 45(e)(4). Solely for purposes of § 45J, electricity will be treated as sold to an unrelated person if the ultimate purchaser of the electricity is not related to the person that produces the electricity. Thus, the requirement of a sale to an unrelated person will be treated as satisfied if the producer sells the electricity to a related person for resale by the related person to a person that is not related to the producer.

.05 Effect of Grants, Tax-Exempt Bond Proceeds, Subsidized Energy Financing, and Other Credits. The amount of the § 45J credit with respect to any facility for any taxable year is not reduced by the amount of any grants, tax-exempt bond proceeds, subsidized energy financing, or other credits (as described in § 45(b)(3)) used for, or in connection with, the facility.

After consultation with the DOE, the Treasury Department and the IRS have determined that no advanced nuclear power facility that received an allocation of the NMCL under Notice 2013-68 was placed in service before January 1, 2021. Therefore, in accordance with section 6 of Notice 2013-68 and § 45J(b)(5)(B), all previous allocations of the NMCL are withdrawn and the total unutilized NMCL is 6,000 megawatts. The unutilized NMCL is available for allocation as provided in section 5 of this notice.

.01 Application Limited to Facilities Certified by DOE. The IRS will allocate the unutilized NMCL only to advanced nuclear power facilities (within the meaning of § 45J(d)(1)(A)) for which the DOE provides certification to the IRS that the facility qualifies as an “advanced nuclear facility.” For purposes of this notice, each nuclear power reactor located on a multi-reactor site is a separate facility. At this time, only an owner of an advanced nuclear power facility that (i) either (I) previously received a certification from the DOE under Notice 2013-68 that such facility qualified as an “advanced nuclear facility” or (II) acquired the facility after the IRS had provided a previous owner of the facility a letter stating that the DOE had certified that facility as an “advanced nuclear facility” under Notice 2013-68, and (ii) maintains an active NRC construction permit or license or combined license, may apply for an allocation of the unutilized NMCL pursuant to this notice. In addition, the rule in section 4.04(3) and (5) of Notice 2013-68 that undivided ownership shares in a facility would be treated as separate facilities for purposes of that notice is disregarded for purposes of determining whether a facility previously received a DOE certification under Notice 2013-68.

.02 Application Required. The IRS will not allocate the unutilized NMCL to any owner of an advanced nuclear power facility unless such owner submits a completed application in accordance with section 6 of this notice.

.03 Allocation Method. The unutilized NMCL will be allocated as follows:

(1) Each facility that meets the requirements of sections 5 and 6 of this notice (qualified facility) will be allocated an amount of the unutilized NMCL equal to its nameplate capacity in the order in which such facilities are placed in service (provided the application deadline specified in section 6.02 of this notice is met). The amount of the unutilized NMCL allocated to a qualified facility is referred to as the facility limitation.

(2) The IRS will continue to allocate the unutilized NMCL equal to the nameplate capacity of a qualified facility until all the unutilized NMCL is allocated. The final recipient(s) of the remaining unutilized NMCL may receive only a portion of the unutilized NMCL for which it applied even if it otherwise meets the requirements under this notice to receive a full allocation.

(3) If only one taxpayer owns a direct interest in a qualified facility, the entire facility limitation is allocated to such taxpayer. If more than one taxpayer owns a direct interest in a qualified facility, each taxpayer’s undivided ownership share in the qualified facility will be treated for purposes of this notice as a separate qualified facility owned by such taxpayer. In such cases, a taxpayer’s application must identify the portion of the total nameplate capacity of the qualified facility that is equal to its undivided ownership share in the qualified facility.

(4) Except as provided in sections 3.03 and 5.03(5) of this notice, if a qualified facility is owned by a partnership or S corporation, then the partnership or S corporation, and not the partners or shareholders, will be treated as the taxpayer that owns the qualified facility for the purposes of this notice. In such cases, the § 45J credit must be allocated to the partners or shareholders in accordance with § 1.704-1(b)(4)(ii), in the case of partnerships, or § 1.1366-1(a)(2)(v), in the case of S corporations.

(5) If the qualified facility is owned through an organization that has made a valid § 761(a) election, each member’s undivided ownership share in the qualified facility will be treated for purposes of this notice as a separate qualified facility owned by such member. In such cases, a member’s application for an allocation must identify the portion of the total nameplate capacity of the qualified facility that is equal to its undivided ownership share in the qualified facility.

.01 In general. (1) A taxpayer must submit, for each facility for which an allocation of the unutilized NMCL is requested, an application to the IRS for an allocation of the unutilized NMCL under § 45J(b)(5) (Application for § 45J Allocation).

(2) An Application for § 45J Allocation should be marked or titled “APPLICATION FOR SECTION 45J ALLOCATION” and delivered in the manner provided in section 6.04 of this notice.

(3) Multiple taxpayers owning (or treated as owning) a direct interest in a facility (as described in section 5.03(3) or (5) of this notice) must each file a separate Application for § 45J Allocation with respect to a single facility. See section 6.03(6) of this notice.

(4) No user fee is required for the submission of an Application for § 45J Allocation.

.02 Application Deadline. An Application for § 45J Allocation must be filed no later than thirty (30) days after the date that the facility is placed in service. A taxpayer may file its Application for § 45J Allocation before the facility is placed in service, but the taxpayer must supplement its application with the statement required under section 6.03(4) of this notice no later than thirty (30) days after the date that the facility is placed in service.

.03 Required Information. An Application for § 45J Allocation must include the following:

(1) The name, taxpayer identification number (if available), and address of the taxpayer who placed or who will place the facility in service;

(2) The name and location of the facility;

(3) The nameplate capacity of the facility;

(4) A statement signed under penalties of perjury (as provided in section 6.03(8) of this notice) providing the date on which the facility was placed in service, the date the facility received an NRC construction permit or license or combined license, and a statement that such permit or license remains active. If the date on which the facility was placed in service is unknown at the time of the Application for § 45J Allocation, such application may be supplemented at any time prior to the application deadline specified in section 6.02 of this notice;

(5) The total amount of unutilized NMCL requested (not to exceed the nameplate capacity of the facility);

(6) If a taxpayer’s Application for § 45J Allocation relates to a facility in which more than one person owns (or is treated as owning) a direct interest (as described in section 5.03(3) or (5) of this notice), the taxpayer must submit documentation of its undivided ownership share in the facility;

(7) If the facility is owned by an organization that has made a § 761(a) election, a copy of the § 761 election;

(8) A declaration, applicable to the Application for § 45J Allocation and any required supplemental submissions, signed by a person currently authorized to bind the taxpayer in these matters, in the following form:

“Under penalties of perjury I declare that I have examined the information contained in this Application for § 45J Allocation and the documents that substantiate this Application for § 45J Allocation, and to the best of my knowledge and belief, it is true, correct, and complete.”

(9) The following additional statement:

“I further declare that I have authority to sign this Application for § 45J Allocation (and any supplemental submissions) on behalf of the taxpayer.”

.04 Where to Submit an Application for § 45J Allocation.

(1) An Application for § 45J Allocation should be sent to the following address:

Internal Revenue Service

Attn: CC:PSI:6, Room 5114

P.O. Box 7604

Ben Franklin Station

Washington, DC 20044

(2) If a private delivery service is used, the address is:

Internal Revenue Service

Attn: CC:PSI:6, Room 5114

1111 Constitution Ave., N.W.

Washington, DC 20224

(3) An Application for § 45J Allocation may also be faxed or e-faxed to (855) 591-7868.

.05 IRS Action. (1) Upon receipt of a taxpayer’s Application for § 45J Allocation, the IRS will determine whether the Application for § 45J Allocation satisfies the requirements of this notice. If the Application for § 45J Allocation does not satisfy the requirements of this notice, the IRS may advise the taxpayer how to perfect its Application for § 45J Allocation. The IRS will not consider an Application for § 45J Allocation to be complete until the IRS receives all the information requested in this notice. The IRS will confirm that the DOE previously certified the taxpayer’s facility as an advanced nuclear facility pursuant to the procedures of Notice 2013-68.

(2) Upon receipt of a completed Application for § 45J Allocation, the IRS will review the taxpayer’s Application for § 45J Allocation and will notify the taxpayer, by letter, of its decision. If the IRS accepts the taxpayer’s Application for § 45J Allocation, the acceptance letter will state the amount of the facility limitation and the portion of that facility limitation being allocated to the taxpayer.

(3) The IRS will allocate the unutilized NMCL under this notice based on the information provided in a taxpayer’s Application for § 45J Allocation. If the IRS determines upon an examination that a facility was not placed in service on the date the taxpayer specified under section 6.03(4) of this notice, the IRS may subsequently withdraw a facility’s allocation of the unutilized NMCL.

.01 In general. Section 45J(e) permits a qualified public entity (as defined in § 45J(e)(2)(A)) to elect to transfer all or a portion of its § 45J credit to an eligible project partner (as defined in § 45J(e)(2)(B)) (§ 45J(e) Election). If a facility is owned by a partnership, a qualified public entity may elect to transfer its distributive share under § 1.704-1(b)(4)(ii) of the credit to an eligible project partner. In addition, if a facility is owned by a partnership, an eligible project partner includes any partner of the partnership. A § 45J(e) Election may be made by a qualified public entity for a taxable year only if a § 45J credit is determined for the qualified public entity for such taxable year. If a qualified public entity is not required to file an income tax return for the taxable year that the § 45J credit is determined, the qualified public entity is still considered a taxpayer for purposes of making the § 45J(e) Election and its taxable year is treated as the calendar year for purposes of determining the § 45J credit and making such election.

.02 Election Procedures. (1) A qualified public entity may make a § 45J(e) Election by furnishing an eligible project partner with a statement titled “SECTION 45J(e) ELECTION STATEMENT” (§ 45J(e) Election Statement) transferring all or a portion of the qualified public entity’s § 45J credit. The statement must be signed under penalties of perjury by an individual with authority to legally bind the qualified public entity. The election statement must also include the written consent of an individual with authority to legally bind the eligible project partner. A qualified public entity must furnish a separate statement to each eligible project partner to whom it transfers any portion of its § 45J credit.

(2) The § 45J(e) Election Statement must include the following information:

(a) The name, address, and taxpayer identification number (if available) of the qualified public entity;

(b) The name and location of the facility;

(c) The nameplate capacity of the facility;

(d) The date on which the facility was placed in service;

(e) The full amount of the unutilized NMCL allocated to the qualified public entity with respect to the facility and a copy of the letter issued by the IRS stating the amount of the unutilized NMCL allocated to the qualified public entity;

(f) The taxable year of the qualified public entity for which the § 45J credit is determined and the election is made;

(g) The name, address and taxpayer identification number of all known eligible project partners receiving any portion of the qualified public entity’s transferred § 45J credit;

(h) The total kilowatt-hours of electricity produced by the facility and sold to an unrelated taxpayer during the taxable year of the qualified public entity for which the election is made;

(i) The total amount of the § 45J credit determined with respect to the qualified public entity for the taxable year for which the election is made and the amount of that § 45J credit that the qualified public entity is electing to transfer to the eligible project partner;

(j) A statement providing how the § 45J credit claimant qualifies as an eligible project partner; and

(k) A declaration, applicable to the § 45J(e) Election Statement signed by a person currently authorized to bind the qualified public entity in these matters, in the following form:

“Under penalties of perjury I declare that I have examined the information contained in this § 45J(e) Election Statement and the documents that substantiate this § 45J(e) Election Statement, and to the best of my knowledge and belief, it is true, correct, and complete.”

(l) The following additional statement:

“I further declare that I have authority to sign this § 45J(e) Election Statement on behalf of the qualified public entity.”

(3) A § 45J(e) Election is an annual election that must be made for each taxable year for which a qualified public entity will transfer the credit to an eligible project partner. A separate election must be made for each eligible project partner for which a qualified public entity will transfer a portion of the § 45J credit.

.03 Due Date for Making Election. The § 45J(e) Election Statement must be furnished to the eligible project partner on or before the due date (including extensions of time) of the eligible project partner’s Federal income tax return on which it claims the transferred § 45J credit for the taxable year ending with, or after, the qualified public entity’s taxable year with respect to which the credit was determined.

.04 Election Irrevocable. An election by a qualified public entity to transfer any portion of the § 45J credit is irrevocable once the § 45J(e) Election Statement referred to in section 7.02 of this notice is furnished to the eligible project partner.

.05 Requirement for an Eligible Project Partner to Claim the Credit. An eligible project partner claims the § 45J credit by filing the applicable IRS form for claiming the credit (and including all requested information) and attaching the § 45J(e) Election Statement furnished by the qualified public entity as provided in section 7.02 of this notice.

.06 Carryforwards and Carrybacks of Credits. In the case of any credit or portion thereof with respect to which a § 45J(e) Election is made, the credit must be taken into account under § 38 by the eligible project partner in the first taxable year of the eligible project partner ending with or after the qualified public entity’s taxable year with respect to which the credit was determined. The carryback and carryforward rule provided in § 39 regarding unused business credits applies to the eligible project partner.

.01 Comments Requested. The Treasury Department and IRS request written comments on issues relating to § 45J(b)(5) and (e) and the guidance provided in this notice. In particular, the Treasury Department and the IRS request comments to address the following:

(1) Section 45J(b)(5) provides that the unutilized NMCL is allocated to facilities in the order in which a facility is placed in service in an allocation amount up to the facility’s nameplate capacity. The Treasury Department and the IRS intend to issue guidance to provide the procedures for a facility that has not previously received a certification from the DOE as an “advanced nuclear facility” under Notice 2013-68 to be allocated unutilized NMCL. Accordingly, the Treasury Department and the IRS invite comments regarding the procedures for allocating the remaining unutilized NMCL.

(2) Section 45J(c)(2) provides that the § 45J credit phases out based on a ratio of the credit determined in § 45J(a) to the reference price defined in § 45(e)(2)(C). The Treasury Department and the IRS invite comments regarding the method for calculating the reference price for the generation of electricity at an advanced nuclear power facility.

.02 How to Submit Comments. All commenters are strongly encouraged to submit comments electronically. Comments should be submitted in writing by May 8, 2023, and should include reference to Notice 2023-24. Comments may be submitted electronically via the Federal eRulemaking Portal at www.regulations.gov (type IRS-2023-0008 in the search field on the regulations.gov homepage to find this notice and submit comments). Alternatively, comments may be mailed to: Internal Revenue Service, Attn: CC:PA:LPD:PR (Notice 2023-24), Room 5203, P.O. Box 7604, Ben Franklin Station, Washington D.C. 20044. The Treasury Department and the IRS will publish for public availability any comment submitted electronically or on paper to its public docket on www.regulations.gov.

The collection of information contained in this notice has been submitted to the Office of Management and Budget in accordance with the Paperwork Reduction Act (PRA) (44 U.S.C. 3507) under control number 1545-2000. An agency may not conduct or sponsor, and a person is not required to respond to, a collection of information unless the collection of information displays a valid OMB control number.

The collections of information in this notice are in sections 6 and 7. The section 6 requirements are not defined as a collection of information under 5 CFR 1320.3(c). The information collection requirements contained in section 7 will be submitted to OMB for review and approval in accordance with 5 CFR 1320.10.

Section 7 provides procedures for a qualified public entity to make an election to transfer the § 45J credits to an eligible project partner (a third-party disclosure under the PRA). The information will be used to determine the portion of the § 45J credits to which an eligible project partner is entitled. An eligible project partner will use the election statement to claim the § 45J credit. This information is required to be collected and retained for taxpayers to claim the § 45J credit.

The collection of information is required to obtain a benefit. The likely respondents are corporations and partnerships.

The estimated total annual reporting burden is 406 hours.

The estimated annual burden per respondent is 5.07 hours. The estimated number of respondents is 80.

The estimated frequency of responses is on occasion.

Books or records relating to a collection of information must be retained as long as their contents may become material in the administration of any internal revenue law. Generally, tax returns and tax return information are confidential, as required by § 6103 of the Code.

The principal author of this notice is John M. Deininger of the Office of Associate Chief Counsel (Passthroughs & Special Industries). For further information regarding this notice contact Mr. Deininger at (202) 317-6853 (not a toll-free number).

1 The amount of the § 45J credit allowed a taxpayer under § 45J(a) for a taxable year may be (i) limited (after the application of § 45J(b)) by an annual limitation under § 45J(c)(1) applicable to each facility and (ii) reduced under § 45J(c)(2) based on an inflation adjusted reference price for electricity described in § 45(e)(2)(C) of the Code.

This notice provides adjustments to the limitation on housing expenses for purposes of section 911 of the Internal Revenue Code for specific locations for 2023. These adjustments are based on geographic differences in housing costs relative to housing costs in the United States.

Section 911 allows a qualified individual to elect to exclude from gross income the foreign earned income and to exclude or deduct the housing cost amount of such individual.

The term “housing cost amount” is generally the total of the housing expenses for the taxable year minus a base housing amount. See § 911(c)(1). For this purpose, the base housing amount for the taxable year is limited to an amount that is tied to the maximum foreign earned income exclusion amount of the qualified individual, which is $120,000 for 2023. See § 911(c)(1)(B). Specifically, the base housing amount is 16 percent of the maximum foreign earned income exclusion amount (computed on a daily basis), multiplied by the number of days in the applicable period that fall within the taxable year. Assuming that the entire taxable year of a qualified individual is within the applicable period, the base housing amount for 2023 is $19,200 ($120,000 x .16).

Similarly, the housing expense amount is also limited, based on a percentage of the maximum foreign earned income exclusion amount. Specifically, the limit on such housing expenses generally equals 30 percent of the maximum foreign earned income exclusion amount (computed on a daily basis), multiplied by the number of days in the applicable period for which the taxpayer is a qualified individual. See § 911(c)(2)(A) and (d)(1). Thus, under this general limitation, a qualified individual whose entire taxable year is within the applicable period is limited to maximum housing expenses of $36,000 ($120,000 x .30) for 2023. However, section 911(c)(2)(B) authorizes the Secretary to issue regulations or other guidance to adjust the percentage under section 911(c)(2)(A)(i) (which determines the limit on housing expenses) based on geographic differences in housing costs relative to housing costs in the United States. Pursuant to this authority, the Department of the Treasury (Treasury Department) and the Internal Revenue Service (IRS) have published annual notices concerning the limitation on the section 911 housing cost amounts since the 2006 taxable year.

For more background on the foreign housing exclusion, see https://www.irs.gov/individuals/international-taxpayers/foreign-housing-exclusion-or-deduction.

The following table provides adjusted limitations on housing expenses (in lieu of the otherwise applicable limitation of $36,000) for 2023. All amounts are in U.S. dollars.

| Country | Location | Limitation on Housing Expenses (full year) | Limitation on Housing Expenses (daily/365 days) |

|---|---|---|---|

| Angola | Luanda | 84,000 | 230.14 |

| Argentina | Buenos Aires | 56,500 | 154.79 |

| Australia | Sydney | 66,500 | 182.19 |

| Bahamas, The | Nassau | 49,700 | 136.16 |

| Bahrain | Bahrain | 48,300 | 132.33 |

| Barbados | Barbados and Bridgetown | 37,700 | 103.29 |

| Belgium | Brussels | 38,700 | 106.03 |

| Bermuda | Bermuda | 90,000 | 246.58 |

| Brazil | Sao Paulo | 56,600 | 155.07 |

| Canada | Calgary | 38,600 | 105.75 |

| Canada | Montreal | 52,600 | 144.11 |

| Canada | Ottawa | 46,100 | 126.30 |

| Canada | Toronto | 59,900 | 164.11 |

| Canada | Vancouver | 56,800 | 155.62 |

| Canada | Victoria | 41,300 | 113.15 |

| Cayman Islands | Grand Cayman | 48,000 | 131.51 |

| China | Beijing | 69,600 | 190.68 |

| China | Hong Kong | 114,300 | 313.15 |

| China | Shanghai | 57,001 | 156.17 |

| Colombia | Bogota | 58,700 | 160.82 |

| Colombia | All cities other than Bogota | 49,400 | 135.34 |

| Costa Rica | San Jose | 37,800 | 103.56 |

| Democratic Republic of the Congo | Kinshasa | 42,000 | 115.07 |

| Denmark | Copenhagen | 43,704 | 119.74 |

| Dominican Republic | Santo Domingo | 45,500 | 124.66 |

| Ecuador | Quito | 38,200 | 104.66 |

| Estonia | Tallinn | 46,600 | 127.67 |

| France | Garches, Paris, Sevres, Suresnes, and Versailles | 66,400 | 181.92 |

| France | Lyon | 36,700 | 100.55 |

| Germany | Berlin | 39,800 | 109.04 |

| Germany | Boeblingen, Ludwigsburg, Nellingen, and Stuttgart | 39,600 | 108.49 |

| Germany | Bonn | 42,000 | 115.07 |

| Germany | Cologne | 56,200 | 153.97 |

| Germany | Gelnhausen and Hanau | 41,000 | 112.33 |

| Germany | Ingolstadt | 46,500 | 127.40 |

| Germany | Kaiserslautern, Landkreis, Pirmasens, Sembach, and Zweibrueken | 39,900 | 109.32 |

| Germany | Mainz and Wiesbanden | 44,500 | 121.92 |

| Germany | Munich | 46,500 | 127.40 |

| Germany | Wahn | 42,000 | 115.07 |

| Guatemala | Guatemala City | 42,000 | 115.07 |

| Guinea | Conakry | 51,300 | 140.55 |

| Holy See, The | Holy See, The | 44,200 | 121.10 |

| India | Mumbai | 67,920 | 186.08 |

| India | New Delhi | 56,124 | 153.76 |

| Indonesia | Jakarta | 37,776 | 103.50 |

| Ireland | Dublin | 38,400 | 105.21 |

| Israel | Beer Sheva | 58,000 | 158.90 |

| Israel | Jerusalem | 49,000 | 134.25 |

| Israel | Tel Aviv | 50,800 | 139.18 |

| Israel | West Bank | 49,000 | 134.25 |

| Italy | Genoa | 41,800 | 114.52 |

| Italy | La Spezia | 40,400 | 110.68 |

| Italy | Milan | 66,000 | 180.82 |

| Italy | Naples | 45,300 | 124.11 |

| Italy | Rome | 44,200 | 121.10 |

| Italy | Vicenza | 36,900 | 101.10 |

| Jamaica | Kingston | 41,200 | 112.88 |

| Japan | Gifu, Komaki, and Nagoya | 74,300 | 203.56 |

| Japan | Okinawa Prefecture | 47,200 | 129.32 |

| Japan | Osaka-Kobe | 90,664 | 248.39 |

| Japan | Tokyo | 77,000 | 210.96 |

| Japan | Yokohama | 41,000 | 112.33 |

| Japan | Yokosuka | 44,300 | 121.37 |

| Kazakhstan | Almaty | 48,000 | 131.51 |

| Korea | Camp Colbern | 54,200 | 148.49 |

| Korea | Camp Market, K-16, Kimpo Airfield, Seoul, and Suwon | 48,600 | 133.15 |

| Korea | Camp Mercer | 54,200 | 148.49 |

| Kuwait | Kuwait City | 64,400 | 176.44 |

| Kuwait | All cities other than Kuwait City | 57,700 | 158.08 |

| Luxembourg | Luxembourg | 36,200 | 99.18 |

| Malaysia | Kuala Lumpur | 46,200 | 126.58 |

| Malta | Malta | 55,100 | 150.96 |

| Mexico | Merida | 37,900 | 103.84 |

| Mexico | Mexico City | 47,900 | 131.23 |

| Mexico | All cities other than Ciudad Juarez, Cuernavaca, Guadalajara, Hermosillo, Matamoros, Mazatlan, Merida, Metapa, Mexico City, Monterrey, Nogales, Nuevo Laredo, Tijuana, and Veracruz | 39,400 | 107.95 |

| Mozambique | Maputo | 39,500 | 108.22 |

| Netherlands | Amsterdam and Schiphol | 52,900 | 144.93 |

| Netherlands | Aruba | 39,300 | 107.67 |

| Netherlands | Hague, The | 52,700 | 144.38 |

| Netherlands Antilles | Curacao | 45,800 | 125.48 |

| Oman | Muscat | 41,300 | 113.15 |

| Panama | Panama City | 39,500 | 108.22 |

| Peru | Lima | 39,100 | 107.12 |

| Poland | Warsaw | 50,200 | 137.53 |

| Portugal | Alverca and Lisbon | 40,400 | 110.68 |

| Qatar | Doha | 45,888 | 125.72 |

| Romania | Bucharest | 41,200 | 112.88 |

| Russia | Moscow | 108,000 | 295.89 |

| Russia | Saint Petersburg | 60,000 | 164.38 |

| Saudi Arabia | Riyadh | 40,000 | 109.59 |

| Singapore | Singapore | 82,900 | 227.12 |

| Slovenia | Ljubljana | 46,400 | 127.12 |

| South Africa | Pretoria | 39,300 | 107.67 |

| Spain | Barcelona | 40,600 | 111.23 |

| Spain | Madrid | 53,900 | 147.67 |

| Switzerland | Bern | 69,000 | 189.04 |

| Switzerland | Geneva | 98,300 | 269.32 |

| Switzerland | Zurich | 39,219 | 107.45 |

| Taiwan | Taipei | 46,188 | 126.54 |

| Tanzania | Dar Es Salaam | 44,000 | 120.55 |

| Thailand | Bangkok | 59,000 | 161.64 |

| Trinidad and Tobago | Port of Spain | 54,500 | 149.32 |

| Ukraine | Kiev | 72,000 | 197.26 |

| United Arab Emirates | Abu Dhabi | 49,687 | 136.13 |

| United Arab Emirates | Dubai | 57,174 | 156.64 |

| United Kingdom | Basingstoke | 41,099 | 112.60 |

| United Kingdom | Bath | 41,000 | 112.33 |

| United Kingdom | Bracknell, High Wycombe, and Reading | 62,100 | 170.14 |

| United Kingdom | Caversham | 73,800 | 202.19 |

| United Kingdom | Cheltenham | 45,600 | 124.93 |

| United Kingdom | Farnborough | 54,700 | 149.86 |

| United Kingdom | Gibraltar | 44,616 | 122.24 |

| United Kingdom | Lakenheath and Mildenhall | 42,600 | 116.71 |

| United Kingdom | London | 64,600 | 176.99 |

| United Kingdom | Loudwater | 52,400 | 143.56 |

| United Kingdom | Southampton | 44,200 | 121.10 |

| United Kingdom | Surrey | 48,402 | 132.61 |

| Venezuela | Caracas | 57,000 | 156.16 |

| Vietnam | Hanoi | 46,800 | 128.22 |

| Vietnam | Ho Chi Minh City | 42,000 | 115.07 |

For some locations, the limitation on housing expenses provided in Section 3 of this notice may be higher than the limitation on housing expenses provided in the “Table of Adjusted Limitations for 2022” in Notice 2022-10, 2022-10 I.R.B. 815. A qualified individual incurring housing expenses in such a location during 2022 may apply the adjusted limitation on housing expenses provided in Section 3 of this notice for 2023 in lieu of the amounts provided in the “Table of Adjusted Limitations for 2022” in Notice 2022-10 (and as set forth in the Instructions to Form 2555, Foreign Earned Income, for 2022).

The Treasury Department and the IRS anticipate that future annual notices providing adjustments to housing expense limitations will make a similar option available to qualified individuals that incur housing expenses in the immediately preceding year. For example, when adjusted housing expense limitations for 2024 are issued, it is expected that taxpayers will be permitted to apply those adjusted limitations to the 2023 taxable year.

This notice is effective for taxable years beginning on or after January 1, 2023. However, as provided in Section 4, taxpayers may apply the 2023 adjusted housing limitations contained in Section 3 of this notice to his or her taxable year beginning in 2022.

| PART 1 – | |

|---|---|

| Section 1.1 – Purpose | 582 |

| Section 1.2 – What’s New | 584 |

| Section 1.3 – Reminders | 584 |

| Section 1.4 – General Requirements for Reproducing IRS Official Form 941, Schedule B, Schedule D, Schedule R, and Form 8974 | 584 |

| Section 1.5 – Reproducing Form 941, Schedule B, Schedule D, Schedule R, and Form 8974 for Software-Generated Paper Forms | 586 |

| Section 1.6 – Specific Instructions for Schedule D | 588 |

| Section 1.7 – Specific Instructions for Schedule R | 588 |

| Section 1.8 – Specific Instructions for Form 8974 | 589 |

| Section 1.9 – Office of Management and Budget (OMB) Requirements for Substitute Forms | 590 |

| Section 1.10 – Order Forms and Instructions | 590 |

| Section 1.11 – Effect on Other Documents | 591 |

| Section 1.12 – Helpful Information | 591 |

| Section 1.13 – Exhibits | 592 |

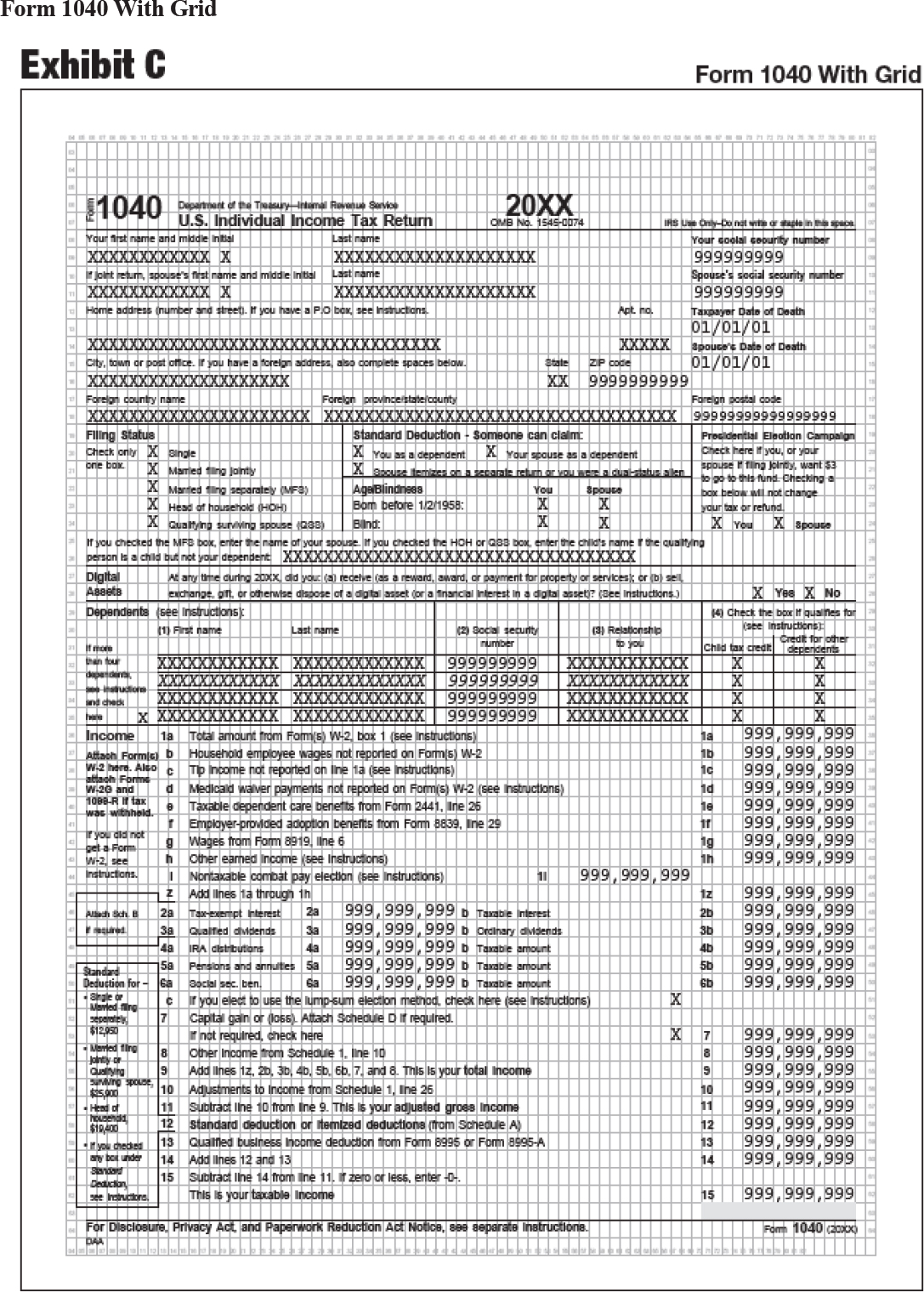

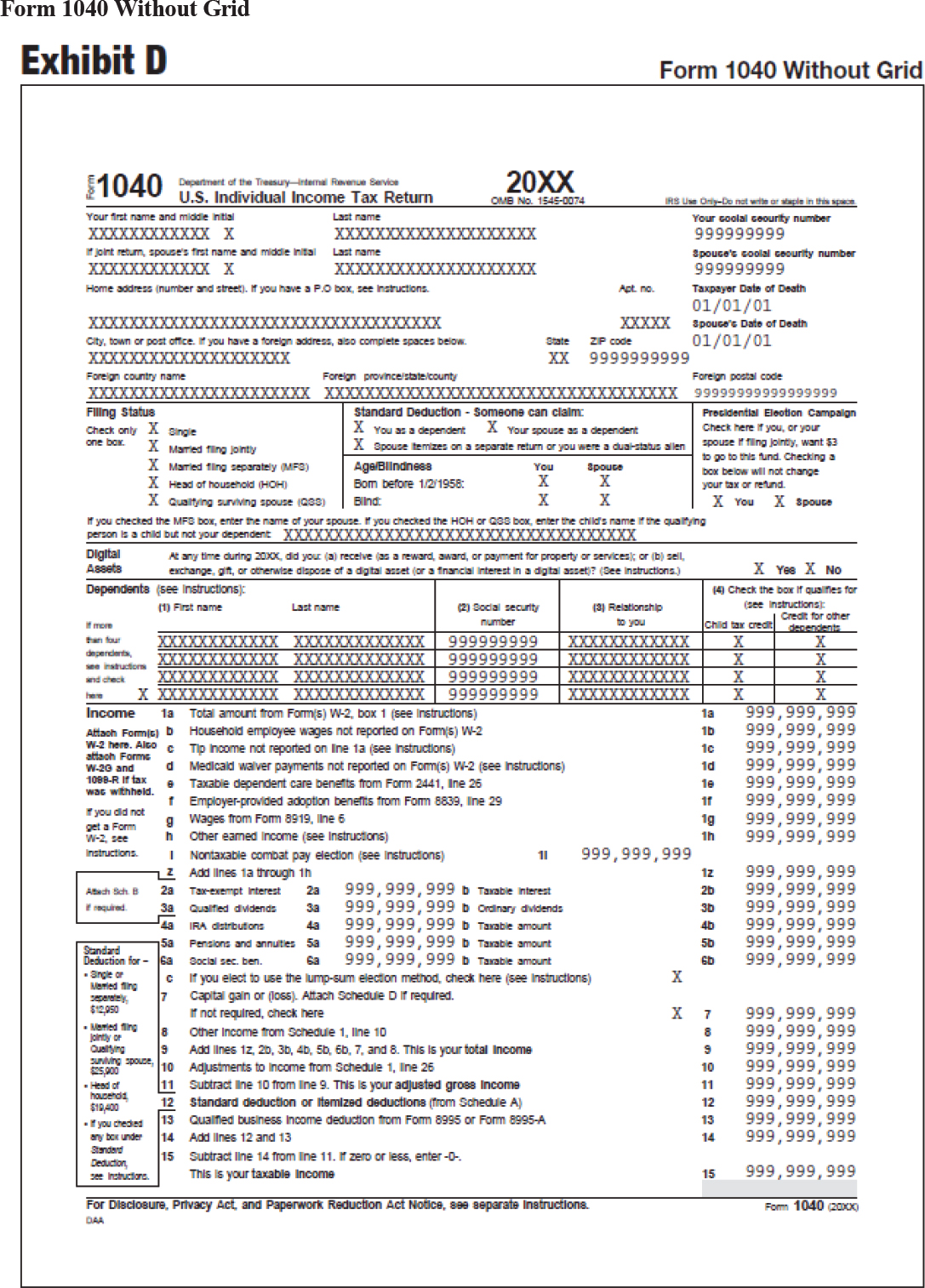

.01 The purpose of this revenue procedure is to provide general rules and specifications from the IRS for paper and computer-generated substitutes for Form 941, Employer’s QUARTERLY Federal Tax Return; Schedule B (Form 941), Report of Tax Liability for Semiweekly Schedule Depositors (referred to in this revenue procedure as “Schedule B”); Schedule D (Form 941), Report of Discrepancies Caused by Acquisitions, Statutory Mergers, or Consolidations (referred to in this revenue procedure as “Schedule D”); Schedule R (Form 941), Allocation Schedule for Aggregate Form 941 Filers (referred to in this revenue procedure as “Schedule R”); and Form 8974, Qualified Small Business Payroll Tax Credit for Increasing Research Activities.

Caution. Before creating a substitute Form 941, see Pub. 1167, General Rules and Specifications for Substitute Forms and Schedules, for additional rules and specifications for payment vouchers (Vouchers), printing in margins (Marginal Printing), and additional instructions (Additional Instructions for All Forms).

Note. Substitute territorial forms (941-PR, Planilla para la Declaración Federal TRIMESTRAL del Patrono; 941-SS, Employer’s QUARTERLY Federal Tax Return (American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, and the U.S. Virgin Islands); and Anexo B (Formulario 941-PR), Registro de la Obligación Contributiva para los Despositantes de Itinerario Bisemanal), should also generally conform to the specifications outlined in this revenue procedure. However, some of the measurements provided in the exhibits, later, may need to be adjusted for substitute territorial forms.

.02 This revenue procedure provides information for substitute Form 941, Schedule B, Schedule D, Schedule R, and Form 8974. If you need more in-depth information on who must complete these forms and how to complete them, see the Instructions for Form 941, the Instructions for Schedule B, the Instructions for Schedule D, the Instructions for Schedule R, the Instructions for Form 8974, and Pub. 15, Employer’s Tax Guide, or go to IRS.gov.

Note. Failure to produce acceptable substitutes of the forms and schedules listed in this revenue procedure may result in delays in processing. This may result in penalties.

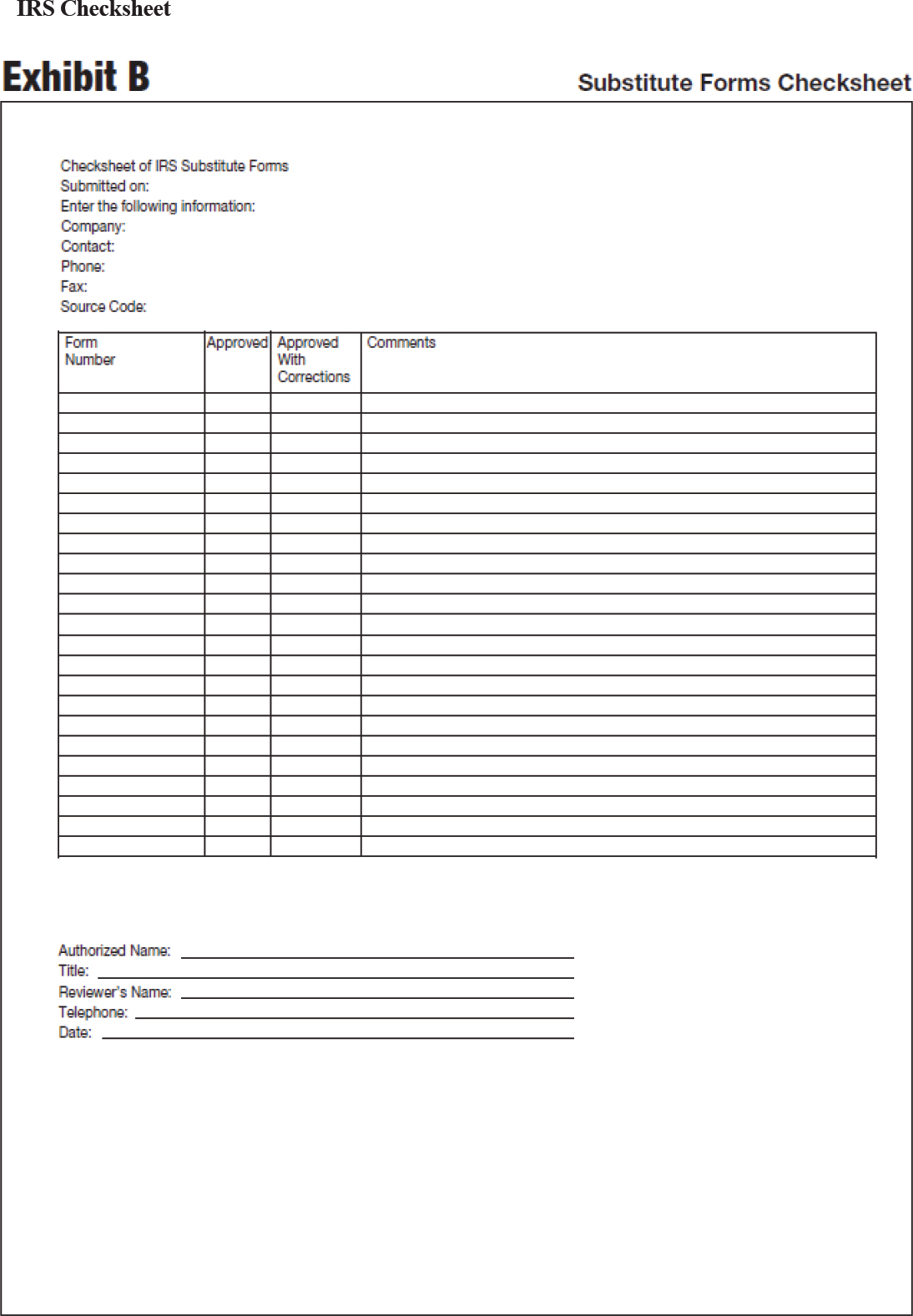

.03 Forms that completely follow the guidelines in this revenue procedure and are exact replicas of the official IRS forms do not need to be submitted to the IRS for specific approval. Substitute forms and schedules need to be scanned using IRS scanning equipment.

If you are uncertain of any specification and want clarification, do the following.

-

Submit a letter citing the specification.

-

State your understanding of the specification.

-

Enclose an example (if appropriate) of how the form would appear if produced using your understanding.

-

Be sure to include your name, complete address, phone number, and, if applicable, your email address with your correspondence. Send your request to SCRIPS@IRS.gov or SubstituteForms@IRS.gov, or use the following address.

Internal Revenue Service Attn: Substitute Forms Program SE:W:CAR:MP:P:TP:TP 5000 Ellin Road, Mail Stop C6-110 Lanham, MD 20706

Note. Allow at least 30 days for the IRS to respond.

.04 However, software developers and form producers should send a blank copy of their substitute Form 941, Schedule B, and Schedule R in Portable Document Format (PDF) to SCRIPS@IRS.gov. The purpose is not specifically for approval but to assist the IRS in preparing to scan these forms. Submitters will only receive comments if a significant problem is discovered through this process. Submitters are not expected to delay marketing their forms in order to receive feedback. Submitters must not include any “live” taxpayer data on any substitute form submitted for review.

.05 Form 941, Schedule B, Schedule R, and Form 8974 have a six-digit form ID code in the upper right-hand corner. The first two digits of the form ID code represent whether the form is an official paper form or a substitute 6x10 grid. The third and fourth digits of the form ID code are a unique identifier that is subject to change each quarter when changes are made to a page of the form. The fifth and six digits of the form ID code generally represent the year in which the IRS made major formatting changes to the layout of a page of the form. The following six-digit form ID codes, some of which have been updated for the first quarter of 2023, are currently used on Form 941, Schedule B, Schedule R, and Form 8974.

-

Official paper forms: 950122 (Form 941, page 1); 951222 (Form 941, page 2); 950922 (Form 941, page 3); 951020 (Form 941, page 4); 960311 (Schedule B); 951422 (Schedule R, page 1); 951522 (Schedule R, page 2); and 950823 (Form 8974).

-

Substitute 6x10 grids: 970122 (Form 941, page 1); 971222 (Form 941, page 2); 970922 (Form 941, page 3); 971020 (Form 941, page 4); 970311 (Schedule B); 971422 (Schedule R, page 1); 971522 (Schedule R, page 2); and 970823 (Form 8974).

You must always use the form ID code provided on the current form for the applicable quarter for which you are creating a substitute form, even if this revenue procedure is not superseded to reflect a change to a form ID code.

Note. Page 4 of Form 941 (page intentionally left blank) is not required to be filed with the IRS as part of a substitute Form 941. However, if page 4 of the substitute Form 941 is filed, it must include the form ID code.

.06 This revenue procedure will be updated only if there are major formatting changes to the layout of the forms (that is, changes to the measurements provided in the exhibits at the end of this revenue procedure) or there are other changes that impact the processing of substitute forms. This revenue procedure won’t be updated solely because a line is changed to “Reserved for future use” or solely because a form ID code changes without major formatting changes.

.01 Some measurements shown in the exhibits for Form 941 have changed due to minor design changes.

.02 Some column headings on Schedule R were revised to make use of columns that were previously “Reserved for future use.”

.03 Form 8974 was revised due to the Inflation Reduction Act of 2022. See the instructions for this form at IRS.gov/Form8974.

.04 Form 941-SS and Form 941-PR will no longer be available after the fourth quarter of 2023. Instead, employers in the U.S. territories will file Form 941, or, if you prefer your form and instructions in Spanish, you can file new Form 941 (sp), Declaración del Impuesto Federal TRIMESTRAL del Empleador.

.01 Submit substitute Form 941, Schedule B, Schedule D, Schedule R, and Form 8974 to the IRS for specifications review. Substitute Form 941, Schedule B, Schedule D, Schedule R, and Form 8974 that completely conform to the specifications contained in this revenue procedure do not require prior approval from the IRS, but should be submitted to SCRIPS@IRS.gov to ensure that they conform to IRS format and scanning specifications.

.02 Print the form on standard 8.5-inch wide by 11-inch paper.

.03 Use white paper that meets generally accepted weight, color, and quality standards (minimum 20 lb. white bond paper).

Note. Reclaimed fiber in any percentage is permitted provided that the requirements of this standard are met.

.04 The IRS prefers printing Form 941 on both sides of a single sheet of paper, but it is acceptable to print on one side of each of two separate sheets of paper.

.05 Make the substitute paper form as identical to the official form as possible.

.06 Print the substitute form using nonreflective black (not blue or other-colored) ink. Printing in an ink color other than black may reduce readability in the scanning process. This may result in figures being too faint to be recognizable.

.07 Use typefaces that are substantially identical in size and shape to the official form and use rules and shading (if used) that are substantially identical to those on the official form. Use font size as large as possible within the fields.

.08 In the same location as shown on the official IRS forms, print the six-digit form ID code (if one exists on the official form) on each form using nonreflective black, carbon-based, 12-point font. The use of non-OCR-A font may reduce readability for scanning. Use the official form to develop your substitute form.

Note. Maintain as much white space as possible around the form ID code. Do not allow character strings to print adjacent to the code.

The following six-digit form ID codes are used on Form 941, Schedule B, Schedule R, and Form 8974 for the first quarter of 2023. Print “950122” on Form 941, page 1; “951222” on Form 941, page 2; “950922” on Form 941, page 3; “951020” on Form 941, page 4; “960311” on Schedule B; “951422” on Schedule R, page 1; “951522” on Schedule R, page 2; and “950823” on Form 8974. You must always use the form ID code provided on the current form for the applicable quarter for which you are creating a substitute form, even if this revenue procedure is not superseded to reflect a change to a form ID code. See Section 1.5 for information on form ID codes for software-generated forms.

Note. Page 4 of Form 941 (page intentionally left blank) is not required to be filed with the IRS as part of a substitute Form 941. However, if page 4 of the substitute Form 941 is filed, it must include the form ID code.

.09 Print the OMB number in the same location as on the official form. Be sure to include the OMB number on Form 941, Schedule B, Schedule D, Schedule R, and Form 8974.

.10 Print all entry boxes and checkboxes exactly as shown (location and size) on the official forms.

Note. Instead of a four-sided checkbox for the entry, just the bottom line of the box can be used as long as the location and size remain the same.

.11 Print “For Privacy Act and Paperwork Reduction Act Notice, see the back of the Payment Voucher.” at the bottom of page 1 of Form 941.

.12 Print “For Paperwork Reduction Act Notice, see separate instructions.” at the bottom of Schedule B and Schedule D.

.13 Print “For Paperwork Reduction Act Notice, see the separate instructions.” at the bottom of Schedule R.

.14 Print “For Paperwork Reduction Act Notice, see the separate instructions.” at the bottom of Form 8974.

.15 Do not print the form catalog number (“Cat. No.”) at the bottom of the forms or instructions. Instead, print your IRS-issued three-letter substitute form source code in place of the catalog number on the left at the bottom of page 1 of Form 941, Schedule B, Schedule D, Schedule R, and Form 8974.

Note. You can obtain a three-letter substitute form source code by requesting it by email at SubstituteForms@IRS.gov. Enter “Substitute Forms” on the subject line.

.16 Do not print the Government Publishing Office (GPO) symbol at the bottom of the forms or instructions.

.01 You may use the PDF files to develop the layout for your forms. Draft forms found at IRS.gov/DraftForms can be used to develop interim formats until the forms are finalized. When forms become finalized, they are posted and can be found at IRS.gov/Forms. You may use 6x10 grid formats to develop software versions of Form 941, Schedule B, Schedule D, Schedule R, and Form 8974.

Please follow the specifications exactly to develop the fields.

.02 If you are developing software using the 6x10 grid, the following six-digit form ID codes are used on Form 941, Schedule B, Schedule R, and Form 8974 for the first quarter of 2023.

-

“970122” for Form 941, page 1; “971222” for Form 941, page 2; “970922” for Form 941, page 3; “971020” for Form 941, page 4; “970311” for Schedule B; “971422” for Schedule R, page 1; “971522” for Schedule R, page 2; and “970823” for Form 8974.

You must always use the form ID code provided on the current form, with the first two digits changed to “97” when using a 6x10 grid, for the applicable quarter for which you are creating a substitute form, even if this revenue procedure is not superseded to reflect a change to a form ID code.

Note. Maintain as much white space as possible around the form ID code. Do not allow character strings to print adjacent to the code.

-

Place all 6x10 grid boxes and entry spaces in the same field locations as indicated on the official forms.

-

Use single lines for “Employer Identification Number (EIN)” and other entry areas in the entity section of Form 941, pages 1, 2, and 3; Schedule B; Schedule R, pages 1 and 2; and Form 8974.

-

Reverse type is not needed as shown on the official form.

-

Do not pre-print decimal points in the data boxes. However, where the amounts are required, the amounts should be printed with decimal points and place holders for cents.

-

Delete the pre-printed formatting in any “date” boxes.

-

Use a single box for “Personal Identification Number (PIN)” on Form 941.

-

You may delete all shading when using the 6x10 grid format.

.03 If producing both the form and the data or the form only, print your three-letter source code at the bottom of Form 941, page 1; Schedule B; Schedule D; Schedule R, page 1; or Form 8974. See Section 1.4.15.

.04 If producing only the data on the form, print your four-digit software industry vendor code on Form 941. The four-digit vendor code preceded by four zeros and a slash (0000/9876) must be pre-printed. If you have a valid vendor code issued to you through the National Association of Computerized Tax Processors (NACTP), you should use that code. If you do not have a valid vendor code, contact the NACTP via email at president@nactp.org for information on these codes.

.05 Print “For Privacy Act and Paperwork Reduction Act Notice, see the back of the Payment Voucher.” at the bottom of Form 941, page 1.

.06 Print “For Paperwork Reduction Act Notice, see separate instructions.” at the bottom of Schedule B and Schedule D.

.07 Print “For Paperwork Reduction Act Notice, see the separate instructions.” at the bottom of Schedule R, page 1.

.08 Print “For Paperwork Reduction Act Notice, see the separate instructions.” at the bottom of Form 8974.

.09 Be sure to print the OMB number in the same location as on the official forms on substitute Form 941, Schedule B, Schedule D, Schedule R, and Form 8974.

.10 Do not print the form catalog number (“Cat. No.”) at the bottom of the forms or instructions.

.11 Do not print the Government Publishing Office (GPO) symbol at the bottom of the forms or instructions.

.12 To ensure accurate scanning and processing, enter data on Form 941, Schedule B, Schedule D, Schedule R, and Form 8974 as follows.

-

Display/print the name and EIN on all pages and attachments in the proper associated fields.

-

Use 12-point (minimum 10-point) Courier font (where possible).

-

Omit dollar signs. Commas are optional.

-

Except for Form 941, lines 1, 2, and 12, leave blank any data field with a value of zero.

-

Enter negative amounts with a minus sign. For example, report “-10.59” instead of “(10.59).”

Note. The IRS prefers that you use a minus sign for negative amounts instead of parentheses or some other means. However, if your software only allows for parentheses in reporting negative amounts, you may use them.

.01 To properly file and to reduce delays and contact from the IRS, Schedule D must be produced as close as possible to the official form.

.02 Use Schedule D to explain why you have certain discrepancies. See the Instructions for Schedule D for more information. In many cases, the information on Schedule D helps the IRS resolve discrepancies without contacting you.

.03 If a substitute Schedule D is not submitted in similar format to the official IRS schedule, the substitutes may be returned, you may be contacted by the IRS, delays in processing may occur, and you may be subject to penalties.

.01 To properly file and to reduce delays and contact from the IRS, Schedule R and Continuation Sheets for Schedule R must be produced as close as possible to the official form.

Note. Do not present the information in spreadsheet or similar format. We may not be able to properly process nonconforming documents with an excessive number of entries. Complete as many Continuation Sheets for Schedule R (Schedule R, page 2) as necessary. If Continuation Sheets are not used or they vary in form from the official form, processing may be delayed and you may be subject to penalties.

.02 Use Schedule R to allocate the aggregate information reported on Form 941 to each client. If you have more than 5 clients, complete as many Continuation Sheets for Schedule R as necessary. Attach Schedule R, including any Continuation Sheets, to your aggregate Form 941 and file it with your return.

Enter your business information carefully.

Make sure all information exactly matches the information shown on the aggregate Form 941. Compare the total of each column on Schedule R, line 9 (including your information on line 8), to the amounts reported on the aggregate Form 941. For each column total of Schedule R, the relevant line from Form 941 is noted in the column heading. If the totals on Schedule R, line 9, do not match the totals on Form 941, there is an error that must be corrected before submitting Form 941 and Schedule R.

.03 Do:

-

Develop and submit only conforming Schedules R;

-

Follow the format and fields exactly as on the official Schedule R, even if this revenue procedure is not superseded to reflect a change in a column heading on Schedule R; and

-

Maintain the same number of entry lines on the substitute Schedule R as on the official form.

.04 Do not:

-

Add or delete entry lines;

-

Submit spreadsheets, database printouts, or similar formatted documents instead of using the Schedule R format to report data; and

-

Reduce or expand font size to add or delete extra data or lines.

.05 If substitute Schedules R and Continuation Sheets for Schedule R are not submitted in similar format to the official schedule, the substitutes may be returned, you may be contacted by the IRS, delays in processing may occur, and you may be subject to penalties.

.01 To properly file and to reduce delays and contact from the IRS, Form 8974 must be produced as close as possible to the official form.

.02 Use Form 8974 only if you are claiming the qualified small business payroll tax credit for increasing research activities.

.03 If a substitute Form 8974 is not submitted in similar format to the official IRS form, the substitutes may be returned, you may be contacted by the IRS, delays in processing may occur, and you may be subject to penalties.

.01 The Paperwork Reduction Act (the Act) of 1995 (P.L. 104-13) requires the following.

-

OMB approves all IRS tax forms that are subject to the Act.

-

Each IRS form contains the OMB approval number, if assigned. The official OMB numbers may be found on the official IRS-printed forms.

-

Each IRS form (or its instructions) states:

1. Why the IRS needs the information,

2. How it will be used, and

3. Whether or not the information is required to be furnished to the IRS.

.02 This information must be provided to any users of official or substitute IRS forms or instructions.

.03 The OMB requirements for substitute IRS forms are the following.

-

Any substitute form or substitute statement to a recipient must show the OMB number as it appears on the official form.

-

For Form 941, Schedule B, Schedule D, Schedule R, and Form 8974, the OMB number (1545-0029) must appear exactly as shown on the official form.

-

For Form 941, Schedule B, Schedule D, Schedule R, and Form 8974, the OMB number must use one of the following formats.

1. OMB No. 1545-0029 (preferred).

2. OMB # 1545-0029 (acceptable).

.04 If no instructions are provided to users of your forms, you must furnish to them the exact text of the Privacy Act and Paperwork Reduction Act Notice.

.01 You can order forms and instructions at IRS.gov/OrderForms.

.01 Revenue Procedure 2022-15, 2022-13 I.R.B. 908, dated March 28, 2022, is superseded.

.01 Please follow the specifications and guidelines to produce substitute Form 941, Schedule B, Schedule D, Schedule R, and Form 8974.

.02 These forms are subject to review and possible changes, as required. Therefore, employers are cautioned against overstocking supplies of privately printed substitutes.

.03 Here is a review of references that were listed throughout this document.

-

Form 941, Employer’s QUARTERLY Federal Tax Return.

-

Schedule B (Form 941), Report of Tax Liability for Semiweekly Schedule Depositors (referred to in this revenue procedure as “Schedule B”).

-

Schedule D (Form 941), Report of Discrepancies Caused by Acquisitions, Statutory Mergers, or Consolidations (referred to in this revenue procedure as “Schedule D”).

-

Schedule R (Form 941), Allocation Schedule for Aggregate Form 941 Filers (referred to in this revenue procedure as “Schedule R”).

-

Form 8974, Qualified Small Business Payroll Tax Credit for Increasing Research Activities.

-

Substitute territorial forms (941-PR, 941-SS, and Anexo B (Formulario 941-PR)).

-

Instructions for Form 941.

-

Instructions for Schedule B (Form 941).

-

Instructions for Schedule D (Form 941).

-

Instructions for Schedule R (Form 941).

-

Instructions for Form 8974.

-

Pub. 15, Employer’s Tax Guide.

-

SCRIPS@IRS.gov for submissions.

-

SubstituteForms@IRS.gov for questions.

-

For questions:

Internal Revenue Service

Attn: Substitute Forms Program

SE:W:CAR:MP:P:TP:TP

5000 Ellin Road, Mail Stop C6-110

Lanham, MD 20706

-

IRS.gov/DraftForms for draft forms.

-

IRS.gov/Forms for final forms.

This revenue procedure provides indexing adjustments for the applicable dollar amounts under § 4980H(c)(1) and (b)(1) of the Internal Revenue Code. These indexed amounts are used to calculate the employer shared responsibility payments (ESRP) under § 4980H(a) and (b)(1), respectively.

Under § 4980H(c)(5), in the case of any calendar year after 2014, the applicable dollar amounts of $2,000 and $3,000 under § 4980H(c)(1) and (b)(1), respectively, are increased by an amount equal to the product of such dollar amount and the premium adjustment percentage (as defined in § 1302(c)(4) of the Patient Protection and Affordable Care Act1) for the calendar year. If the amount of any increase is not a multiple of $10, such increase is rounded to the next lowest multiple of $10.