)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

Internal Revenue Bulletin: 2024-31

July 29, 2024

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

These proposed regulations would remove the prohibition in the current regulation under section 6311(d)(2) that prevents the IRS from paying a fee under a contract that allows the receipt of credit card or debit card payments from a taxpayer. The proposed regulations would also remove the prohibition on charging the taxpayer a fee for paying taxes by credit or debit card. The proposed regulations reflect amendments to section 6311 made in the Taxpayer First Act. The proposed regulation would not require the IRS to change its current procedure of using third parties to process credit and debit card tax payments.

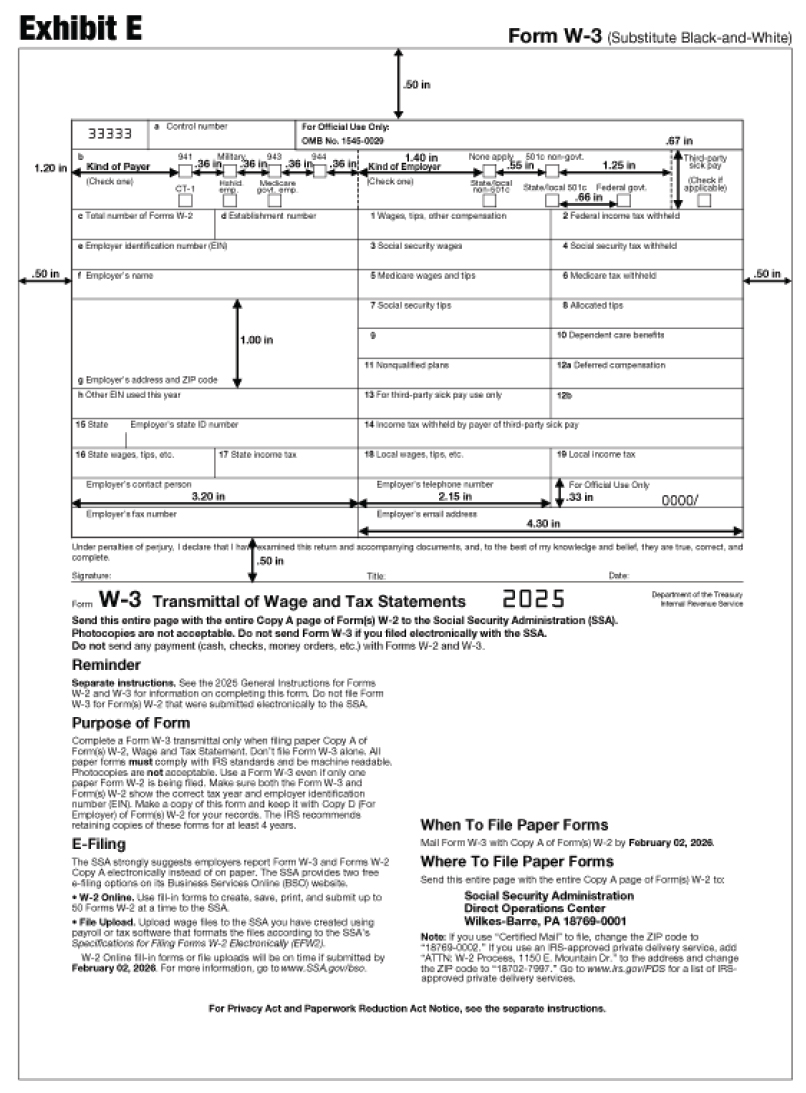

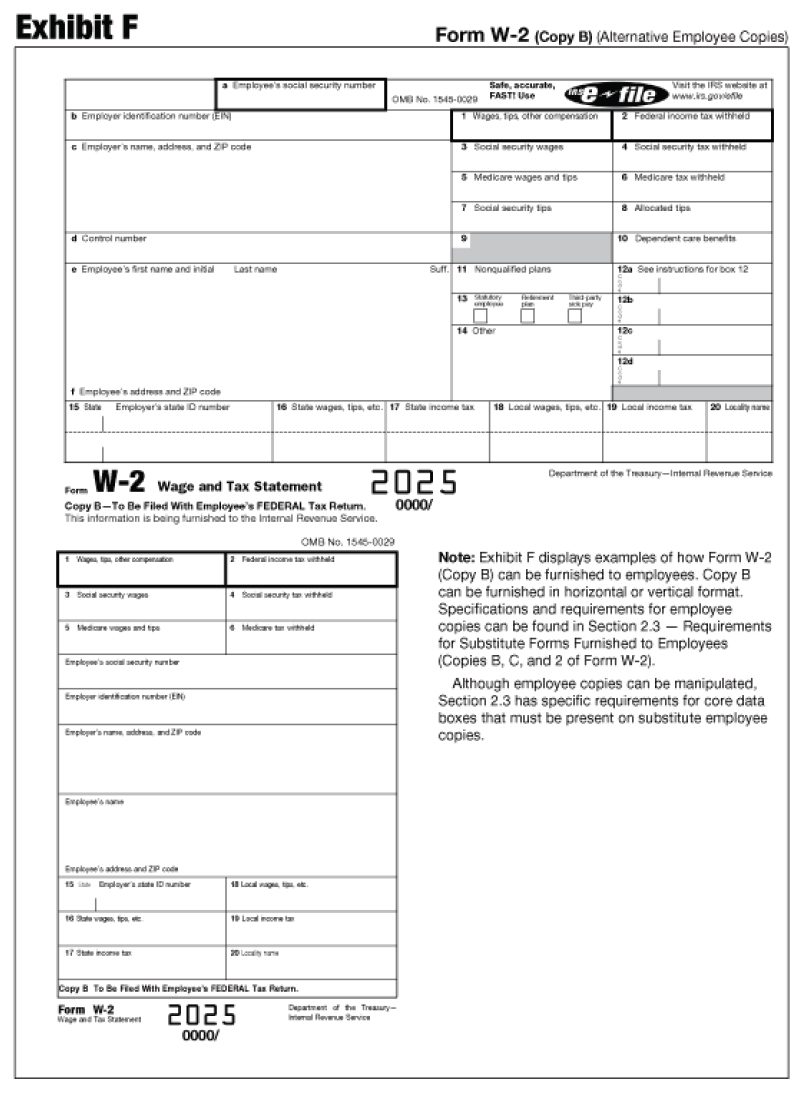

This revenue procedure provides specifications for the private printing of red-ink substitutes for the 2024 Forms W-2 and W-3. This revenue procedure will be produced as the next revision of Publication 1141. Rev. Proc. 2023-25 is superseded.

NOTE. This revenue procedure will be reproduced as the next revision of IRS Publication 1141, General Rules and Specifications for Substitute Forms W-2 and W-3.

26 CFR 601.602: Tax forms and instructions. (Also Part I, Sections 6041, 6051, 6071, 6081, 6091; 1.6041-1, 1.6041-2, 31.6051-1, 31.6051-2, 31.6071(a)-1, 31.6081(a)-1, 31.6091-1.)

The regulations require information reporting by brokers for certain digital asset sales and exchanges. They apply to brokers who take possession of the assets involved in these sales and exchanges, including custodial digital asset exchanges, certain hosted wallet providers, certain processors of digital asset payments, and digital asset kiosks, which are sometimes known as digital asset ATM machines. Brokers covered by these final regulations will be required to file new Form 1099-DA and furnish payee statements reporting the gross proceeds of transactions occurring on or after January 1, 2025. Certain brokers will be required to report basis on Forms 1099-DA for transactions occurring on or after January 1, 2026. Basis reporting is required only if the customer acquired the digital asset being sold or exchanged from the same broker on or after January 1, 2026. Real estate reporting persons, who were already required to file information returns under the existing section 6045 regulations, will now also be required to report dispositions of digital assets as all or part of the purchase price of real property, beginning with transactions occurring on or after January 1, 2026. In addition to the broker reporting rules, these regulations also establish rules for calculating the value and basis of digital assets.

26 CFR 1.6045-1 Returns of information of brokers and barter exchanges

These proposed regulations under sections 3111, 3131, 3132, 3134 and 3221 of the Internal Revenue Code authorize the assessment and collection of any overpayment interest paid to a taxpayer on an erroneous refund of the employment tax credits provided under the Families First Coronavirus Response Act, the Coronavirus Aid, Relief, and Economic Security Act, and the American Rescue Plan Act of 2021. This allows the IRS to efficiently recover any overpayment interest on erroneous refunds while preserving administrative protections for taxpayers.

Subject to certain requirements, this Revenue Procedure generally permits taxpayers to rely on any reasonable allocation of units unattached basis to a digital asset wallet or account that holds the same number of remaining digital asset units based on the taxpayer’s records of such unattached basis and remaining units. The allocation must be a reasonable allocation as defined in section 5.02 of this Revenue Procedure and must be made as of January 1, 2025. However, the taxpayer may identify the method of allocation and may comply with the requirements set forth in section 4.02 of this Revenue Procedure at a later date to the extent permitted by section 5.02(4) or 5.02(5) of this Revenue Procedure.

26 CFR 1.1012: GUIDANCE FOR TAXPAYERS TO ALLOCATE BASIS IN DIGITAL ASSETS TO WALLETS OR ACCOUNTS AS OF JANUARY 1, 2025

(Also: Part I, §§ 1012, 6045, 1.1012-1, 1.6045-1)

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 1, 31, and 301

Gross Proceeds and Basis Reporting by Brokers and Determination of Amount Realized and Basis for Digital Asset Transactions

AGENCY: Internal Revenue Service (IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document contains final regulations regarding information reporting and the determination of amount realized and basis for certain digital asset sales and exchanges. The final regulations require brokers to file information returns and furnish payee statements reporting gross proceeds and adjusted basis on dispositions of digital assets effected for customers in certain sale or exchange transactions. These final regulations also require real estate reporting persons to file information returns and furnish payee statements with respect to real estate purchasers who use digital assets to acquire real estate.

DATES: Effective date: These regulations are effective on September 9, 2024.

Applicability dates: For dates of applicability, see §§1.1001-7(c); 1.1012-1(h)(5); 1.1012-1(j)(6); 1.6045-1(q); 1.6045-4(s); 1.6045B-1(j); 1.6050W-1(j); 31.3406(b)(3)-2(c); 31.3406(g)-1(f); 31.3406(g)-2(h); 301.6721-1(j); 301.6722-1(g).

FOR FURTHER INFORMATION CONTACT: Concerning the final regulations under sections 1001 and 1012, Alexa Dubert or Kyle Walker of the Office of the Associate Chief Counsel (Income Tax and Accounting) at (202) 317-4718; concerning the international sections of the final regulations under sections 3406 and 6045, John Sweeney or Alan Williams of the Office of the Associate Chief Counsel (International) at (202) 317-6933; and concerning the remainder of the final regulations under sections 3406, 6045, 6045A, 6045B, 6050W, 6721, and 6722, Roseann Cutrone of the Office of the Associate Chief Counsel (Procedure and Administration) at (202) 317-5436 (not toll-free numbers).

SUPPLEMENTARY INFORMATION:

This document contains amendments to the Regulations on Income Taxes (26 CFR part 1), the Regulations on Employment Tax and Collection of Income Tax at the Source (26 CFR part 31), and the Regulations on Procedure and Administration (26 CFR part 301) pursuant to amendments made to the Internal Revenue Code (Code) by section 80603 of the Infrastructure Investment and Jobs Act, Public Law 117-58, 135 Stat. 429, 1339 (2021) (Infrastructure Act) relating to information reporting by brokers under section 6045 of the Code. Specifically, the Infrastructure Act clarified the rules regarding how certain digital asset transactions should be reported by brokers, expanded the categories of assets for which basis reporting is required to include all digital assets, and provided a definition for the term digital assets. Additionally, the Infrastructure Act clarified that transfer statement reporting under section 6045A(a) of the Code applies to covered securities that are digital assets and added a new information reporting provision under section 6045A(d) to require brokers to report on transfers of digital assets that are covered securities, provided the transfer is not a sale and is not to an account maintained by a person, as defined in section 7701(a)(1) of the Code, that the broker knows or has reason to know is also a broker. Finally, the Infrastructure Act provided that these amendments apply to returns required to be filed, and statements required to be furnished, after December 31, 2023, and provided a rule of construction stating that these statutory amendments shall not be construed to create any inference for any period prior to the effective date of the amendments with respect to whether any person is a broker under section 6045(c)(1) or whether any digital asset is property which is a specified security under section 6045(g)(3)(B).

On August 29, 2023, the Treasury Department and the IRS published in the Federal Register (88 FR 59576) proposed regulations (REG-122793-19) (proposed regulations) relating to information reporting under section 6045 by brokers, including real estate reporting persons and certain third party settlement organizations under section 6050W of the Code. Additionally, the proposed regulations included specific rules under section 1001 of the Code for determining the amount realized in a sale, exchange, or other disposition of digital assets and under section 1012 of the Code for calculating the basis of digital assets. The proposed regulations stated that written or electronic comments provided in response to the proposed regulations must be received by October 30, 2023.

The Treasury Department and the IRS received over 44,000 written comments in response to the proposed regulations. Although https://www.regulations.gov indicated that over 125,000 comments were received, this larger number reflects the number of “submissions” that each submitted comment indicated were included in the posted comment, whether or not the comment actually included such separate submissions. All posted comments were considered and are available at https://www.regulations.gov or upon request. A public hearing was held on November 13, 2023.

Several comments requested an extension of the time to file comments in response to the proposed regulations. These requests for extension ranged from a few weeks to several years, but most comments requested a 60-day extension. In response to these comments, the due date for the comments was extended until November 13, 2023. The comment period was not extended further for several reasons. First, information reporting rules are necessary to make digital asset investors aware of their taxable transactions and to make those transactions more transparent to the IRS to reduce the tax gap. It is, therefore, a priority that the publication of these regulations is not delayed more than is necessary. Second, although the Infrastructure Act amended section 6045 in November 2021 to broadly apply the information reporting rules for digital asset transactions to a wide variety of brokers, the broker reporting regulations for digital assets were added to the Treasury Priority Guidance Plan in late 2019. Brokers, therefore, have long been on notice that there would be proposed regulations on which to comment. Third, as discussed in Part VI. of this Summary of Comments and Explanation of Revisions, the Treasury Department and the IRS understand that brokers need time after these final regulations are published to develop systems to comply with the final reporting requirements. Without further delaying the applicability date of these much-needed regulations, therefore, extending the comment period would necessarily reduce the time brokers would have to develop these systems. Fourth, a 60-day comment period is not inherently short or inadequate. Executive Order (E.O.) 12866 provides that generally a comment period should be no less than 60 days, and courts have uniformly upheld comment periods of even shorter comment periods. See, e.g., Connecticut Light & Power Co. v. NRC, 673 F.2d 525, 534 (D.C.Cir. 1982), cert. denied, 459 U.S. 835, 103 S.Ct. 79, 74 L.Ed.2d 76 (1982) (denying petitioner’s claim that a 30 day comment period was unreasonable, notwithstanding petitioner’s complaint that the rule was a novel proposition); North American Van Lines v. ICC, 666 F.2d 1087, 1092 (7th Cir. 1981) (claim that 45 day comment period was insufficient rejected as “without merit”). Indeed, over 44,000 comments were received before the conclusion of the comment period ending on November 13, 2023, which demonstrates that this comment period was sufficient for interested parties to submit comments. Fifth, it has been a longstanding policy of the Treasury Department and the IRS to consider comments submitted after the published due date, provided consideration of those comments does not delay the processing of the final regulation. IRS Policy Statement 1-31, Internal Revenue Manual 1.2.1.15.4(6) (September 3, 1987). In fact, all comments received through the requested 60-day extension period were considered in promulgating these final regulations. Moreover, the Treasury Department and the IRS accepted late comments through noon eastern time on April 5, 2024.

The Summary of Comments and Explanation of Revisions of the final regulations summarizes the provisions of the proposed regulations, which are explained in greater detail in the preamble to the proposed regulations. After considering the comments to the proposed regulations, the proposed regulations are adopted as amended by this Treasury decision in response to such comments as described in the Summary of Comments and Explanation of Revisions.

These final regulations concern Federal tax laws under the Internal Revenue Code only. No inference is intended with respect to any other legal regime, including the Federal securities laws and the Commodity Exchange Act, which are outside the scope of these regulations.

A. Definition of digital assets subject to reporting

The proposed regulations required reporting under section 6045 for certain dispositions of digital assets that are made in exchange for cash, different digital assets, stored-value cards, broker services, or property subject to reporting under existing section 6045 regulations or any other property in a payment transaction processed by a digital asset payment processor (referred to in these final regulations as a processor of digital asset payments or PDAP). The proposed regulations defined a digital asset as a digital representation of value that is recorded on a cryptographically secured distributed ledger (or any similar technology), without regard to whether each individual transaction involving that digital asset is actually recorded on the cryptographically secured distributed ledger. Additionally, the proposed regulations provided that a digital asset does not include cash in digital form.

While some comments expressed support for the definition of digital asset in the proposed regulations, other comments raised concerns that the definition of digital asset goes beyond the statutory definition found in amended section 6045. For example, one comment recommended applying the definition only to assets held for investment and excluding any assets that are used for other functions, which include, in their view, nonfungible tokens (NFTs), stablecoins, tokenized real estate, and tokenized commodities. Another comment recommended narrowing the definition of digital asset to apply only to blockchain “native” digital assets and exempting all NFTs and other tokenized versions of traditional asset classes, such as tokenized securities, and other digital assets that don’t function as a medium of exchange, unit of account, or store of value. Another comment recommended that the definition of digital asset distinguish between digital representations of what the comment referred to as “hard assets,” such as gold, where the digital asset is merely a proxy for the underlying asset versus digital assets that are not backed by hard assets. Another comment recommended that the definition of digital asset not include tokenized assets, including financial instruments that have been tokenized. The final regulations do not adopt these comments. As discussed more fully in Parts I.A.1. and A.2. of this Summary of Comments and Explanation of Revisions, neither the statutory language nor the legislative history to the Infrastructure Act suggest Congress intended such a narrow interpretation of the term.

The Infrastructure Act made changes to the third party information reporting rules under section 6045. Third party information reporting generally contributes to lowering the income tax gap, which is the difference between taxes legally owed and taxes actually paid. GAO, Tax Gap: Multiple Strategies Are Needed to Reduce Noncompliance, GAO-19-558T at 6 (Washington, D.C.: May 9, 2019). It is anticipated that broker information reporting on digital asset transactions will lead to higher levels of taxpayer compliance because brokers will provide the information necessary for taxpayers to prepare their Federal income tax returns and reduce the number of inadvertent errors or intentional omissions or misstatements shown on those returns. Because digital assets can easily be held and transferred, including to offshore destinations, directly by a taxpayer rather than by an intermediary, digital asset transactions raise tax compliance concerns that are specific to digital assets in addition to the more general tax compliance concerns relevant to securities, commodities, and other assets that are reportable under section 6045 and to cash payments reportable under other reporting provisions. The Treasury Department and the IRS have consequently concluded that the definition of digital assets in section 6045(g)(3)(D) provides the appropriate scope for digital assets subject to broker reporting. To the extent sales of digital assets including NFTs, tokenized securities, and other digital assets that may not function as a medium of exchange, unit of account, or store of value, give rise to taxable gains and losses, these assets should be included in the definition of digital assets. See, however, Part I.D.3. of this Summary of Comments and Explanation of Revisions for a description of an optional reporting rule for many NFTs that would eliminate reporting on those NFTs when certain conditions are met, and Part I.A.4.a. of this Summary of Comments and Explanation of Revisions for a description of a special rule providing that assets that are both securities and digital assets are reportable as securities rather than as digital assets when specified conditions are met.

Some comments asserted that the statutory definition of digital assets is or should be limited to assets that are financial instruments. These comments are discussed in Part I.A.2. of this Summary of Comments and Explanation of Revisions.

Other comments raised a concern that the definition of digital assets is ambiguous and recommended adding examples that clarify the types of property that are and are not digital assets. For reasons discussed more fully in Parts I.A.1., A.2., and A.3. of this Summary of Comments and Explanation of Revisions, the final regulations include several additional examples that illustrate and further clarify certain types of digital assets that are included in the definition, such as qualifying stablecoins, specified nonfungible tokens (specified NFTs), and other fungible digital assets.

One comment suggested that the term cryptographically secured distributed ledger be defined in the final regulations as a type of data storage and transmission file which uses cryptography to allow for a decentralized system of verifying transactions. This comment also stated that the definition should state that the stored information is an immutable database and includes an embedded system of operation, and that a blockchain is a type of distributed ledger. The final regulations do not adopt this recommendation because clarification of the term is not necessary and because the recommended changes are potentially unduly restrictive to the extent they operate to restrict future broker reporting obligations should advancements be made in how distributed ledgers are cryptographically secured.

One comment suggested that the proposed definition of a digital asset is overly broad because it includes transactions recorded in the broker’s books and records (commonly referred to as “off-chain” transactions) and not directly on a distributed ledger. Another comment specifically supported the decision to not limit the definition to only those digital representations for which each transaction is actually recorded or secured on a cryptographically secured distributed ledger. The Treasury Department and the IRS have determined that the definition of digital asset is not overly broad in this regard because eliminating digital assets that are traded in off-chain transactions from the definition would fail to provide information reporting on the significant amount of trading that occurs off-chain on the internal ledgers of custodial digital asset trading platforms. Moreover, since the mechanics of how an asset sale is recorded does not impact whether there has been a taxable disposition of that asset, those mechanics should not impact whether the underlying asset is or is not a digital asset.

A comment suggested that the definition of a digital asset should eliminate the phrase “or any similar technology” because the scope of that phrase is unclear and could negatively impact future technology improvements, such as privacy-preserving technology, cryptography, distributed database systems, distributed network systems, or other evolving technology. Another comment requested that the definition of any similar technology be limited to instances in which the IRS identifies such future similar technologies in published guidance. The final regulations do not adopt this comment. Using the phrase “any similar technology” is consistent with the Infrastructure Act’s use of the same term in its definition of digital assets in section 6045(g)(3)(D). Further, including any similar technology along with cryptographically secured ledgers is necessary to ensure that brokers continue to report on transactions involving these assets without regard to advancements in or changes to the techniques, methods, and technology, on which these assets are based. The Treasury Department and the IRS are not currently aware of any existing technology that would fit within this “or any similar technology” standard, but if brokers or other interested parties identify new technological developments and are uncertain whether they fit within the definition, they can make the Treasury Department and the IRS aware of the new technology and request guidance at that time.

1. Stablecoins

As explained in the preamble to the proposed regulations, the definition of digital assets was intended to apply to all types of digital assets, including so-called stablecoins that are designed to have a stable value relative to another asset or assets. The preamble to the proposed regulations noted that such stablecoins can take multiple forms, may be backed by several different types of assets that are not limited to currencies, may not be fully collateralized or supported fully by reserves by the underlying asset, do not necessarily have a constant value, are frequently used in connection with transactions involving other types of digital assets, and are held and transferred in the same manner as other digital assets. In addition to fiat currency, other assets to which so-called stablecoins can be pegged include commodities or other financial instruments (including other digital assets). No comments were received that specifically advocated for the exclusion of a so-called stablecoin that has a fixed exchange rate with (that is, is pegged to) a commodity, another financial instrument, or any other asset other than a specific convertible currency issued by a government or a central bank (including the U.S. dollar) (sometimes referred to in this preamble as fiat currency). The Treasury Department and the IRS have determined that it would be inappropriate to exclude stablecoins that are pegged to such assets from the definition of digital assets. Accordingly, this preamble uses the term stablecoin to refer only to the subset of so-called stablecoins referred to in the proposed regulations that are pegged to a fiat currency.

Numerous comments received specifically advocated for the exclusion from the definition of digital assets stablecoins that are pegged to a fiat currency. Numerous comments stated that failure to exclude stablecoins from the definition of digital assets would hinder the adoption of these stablecoins in the marketplace, deter their integration into commercial payment systems, and undermine Congressional efforts to establish a regulatory framework for stablecoins that can be used to make payments. Additional comments raised concerns about privacy, drew an analogy to the exemption in the existing regulations for reporting on shares of money market funds, or recommended that reporting on stablecoins be deferred until after the substantive tax treatment of stablecoins is clarified with guidance issued by the Treasury Department and the IRS or until a legislative framework is established by Congress. Several other comments recommended that reporting on stablecoins be required, noting that stablecoins can be volatile in value and regularly vary from a one-to-one parity with the fiat currency they are pegged to, and therefore may give rise to gain or loss on disposition.

After consideration of the comments, the final regulations do not exclude stablecoins from the definition of digital assets. Stablecoins unambiguously fall within the statutory definition of digital assets as they are digital representations of the value of fiat currency that are recorded on cryptographically secured distributed ledgers. Moreover, because stablecoins are integral to the digital asset ecosystem, excluding stablecoins from the definition of digital assets would eliminate a source of information about digital asset transactions that the IRS can use in order to ensure compliance with taxpayers’ reporting obligations.

The Treasury Department and the IRS are aware that legislation has been proposed that would regulate the issuance and terms of stablecoins. If legislation is enacted regulating stablecoins, the Treasury Department and the IRS intend to take that legislation into account in considering whether to revise the rules for reporting on stablecoins provided in these final regulations.

Notwithstanding that the final regulations include stablecoins in the definition of digital assets, the Secretary has broad authority under section 6045 to determine the extent of reporting required by brokers on transactions involving digital assets. In response to the request for comments in the preamble to the proposed regulations on whether stablecoins, or other coins whose value is pegged to a specified asset, should be excluded from reporting under the final regulations, numerous comments largely focused on stablecoins, rather than coins that track a commodity price or the price of another digital asset. Many of these comments requested that sales of stablecoins be exempted from broker reporting in whole or in part because reporting on all transactions involving stablecoins would result in a very large number of reports on transactions involving little to no gain or loss, on the grounds that these reports would be burdensome for brokers to provide, potentially confusing to taxpayers and of minimal utility to the IRS. These comments asserted that most transactions involved little or no gain or loss because, in their view, stablecoins closely track the value of the fiat currency to which they are pegged. Some comments recommended that certain types of stablecoin transactions be reportable, including requiring reporting of dispositions of stablecoins for cash or where there is active trading in the stablecoin that is intended to give rise to gain (or loss).

The Treasury Department and the IRS agree that transaction-by-transaction reporting for stablecoins would result in a high volume of reports. Indeed, according to a report by Chainalysis on the “Geography of Cryptocurrency” analyzing public blockchain transactions (commonly referred to as “on-chain” transactions), stablecoins are the most widely used type of digital asset, making up more than half of all on-chain transactions to or from centralized services between July 2022 and March 2023. Chainalysis, The 2023 Geography of Cryptocurrency Report, p. 14 (October 2023). Given the popularity of stablecoins and the number of stablecoin sales that are unlikely to reflect significant gains or losses, the Treasury Department and the IRS have determined that it is appropriate to provide an alternative reporting method for certain stablecoin transactions to alleviate unnecessary and burdensome reporting. Accordingly, the final regulations have added a new optional alternative reporting method for sales of certain stablecoins to allow for aggregate reporting instead of transactional reporting, with a de minimis annual threshold below which no reporting is required. See Part I.D.2. of this Summary of Comments and Explanation of Revisions. Consistent with the proposed regulations, brokers that do not use this alternative reporting method must report sales of stablecoins under the same rules as for other digital assets. See Part I.D.2. of this Summary of Comments and Explanation of Revisions for the discussion of alternative reporting rules for certain stablecoins.

2. Nonfungible Tokens

As with stablecoins, the definition of digital assets in the proposed regulations includes NFTs without regard to the nature of the underlying asset, if any, referenced by the NFT. Although some comments expressed agreement that the definition of digital asset in the statute is broad enough to include all NFTs, other comments raised concerns that the Secretary did not have the authority to include NFTs in broker reporting. That is, the comments argued that while NFTs have value, they do not constitute “representations of value” as required by the statutory definition in section 6045(g)(3)(D). Classifying an NFT as a “representation of value” merely because it has value, these comments asserted, would fail to give effect to the word “representation” in the statute. As support for this view, one comment cited to Senator Portman’s floor colloquy reference to the intended application of the reporting rule to “cryptocurrency.” 167 Cong. Rec. S6095-6 (daily ed. August 9, 2021). Ultimately, these comments recommended excluding sales of NFTs from the definition of digital assets. The final regulations do not adopt these comments. Although NFTs may reference assets with value, this does not prevent them from also “representing value.” Moreover, that interpretation would lead to a result that would contravene the statutory changes to the broker reporting rules by the Infrastructure Act. Excluding all NFTs from the definition of digital assets merely because NFTs may reference assets with value rather than “represent value” would result in the exclusion of NFTs that reference traditional financial assets. These assets have been subject to reporting under section 6045 for nearly 40 years, and there is no reason to exclude them from reporting now based only on the circumstance of their trades through NFTs, rather than through other traditional means.

Numerous comments asserted that the statutory reference to any “representation of value” should limit the definition of digital assets to only those digital assets that reference financial instruments or otherwise could be used to deliver value (such as a method of payment). Numerous comments expressed that many NFTs, such as, digital art and collectibles, are unique digital assets that are bought and sold for personal enjoyment rather than financial gain and therefore should not be subject to reporting. Similarly, other comments raised the series-qualifier canon of statutory construction, which provides that when a statute contains a list of closely related, parallel, or overlapping terms followed by a modifier, that modifier should be applied to all the terms in the list. Therefore, according to the comments, because “any digital asset” is included in the section 6045(g)(3)(B) list of assets defining specified security and because that list concludes with “any other financial instrument,” these comments argue that the definition of “digital asset” must be limited to assets that are, or are akin to, “financial instruments.” As additional support for this suggestion, one comment cited the rule of last antecedent, which is another canon of statutory construction and provides that a limiting clause or phrase should ordinarily be read as modifying only the noun or phrase that it immediately follows. That is, because the “other financial instrument” clause directly follows “any digital asset” in the list, the definition of any digital asset must be limited to only those digital assets that constitute financial instruments.

The final regulations do not adopt these comments. The plain language of the digital asset definition in section 6045(g)(3)(D) reflects only two specific limitations on the definition: “[e]xcept as otherwise provided by the Secretary” and “recorded on a cryptographically secured distributed ledger or similar technology as specified by the Secretary.” The legislative history to the Infrastructure Act does not support the conclusion that Congress intended the “representation of value” phrase to limit the definition of digital assets to only those digital assets that are financial instruments. To the contrary, a report by the Joint Committee on Taxation published in the Congressional Record prior to the enactment of the Infrastructure Act cited to and relied on the Notice 2014-21, 2014-16 I.R.B. 938 (April 14, 2014) definition of virtual currency, which first used the phrase “representation of value.” 167 Cong. Rec. S5702, 5703 (daily ed. August 3, 2021) (Joint Committee on Taxation, Technical Explanation of Section 80603 of the Infrastructure Act). That virtual currency definition specifically limited the “representation of value” phrase to those assets that function “as a medium of exchange, unit of account, and/or store of value.” This limitation would not have been necessary had the “representation of value” phrase been limited to assets that function as financial instruments. Moreover, Congress’ use of the term “digital asset” instead of “digital currency” also supports the broader interpretation of the term.

The final regulations also do not adopt the interpretation of the referenced canons of statutory construction presented by the comments because those canons should not be used to limit the definition of digital assets in a statute that includes an explicit and unambiguous definition of that term. Moreover, the referenced canons do not lead to the result asserted by the comments. The series-qualifier canon is not applicable here because not all the items in the list at section 6045(g)(3)(B) are consistent with the “financial instrument” language following the list. For example, section 6045(g)(3)(B)(iii) references any commodity, which under §1.6045-1(a)(5) of the final regulations effective before the effective date of these final regulations1 and these final regulations, specifically includes physical assets, such as lead, palm oil, rapeseed, tea, and tin, which are not financial instruments. The term commodity also includes any type of personal property that is traded through regulated futures contracts approved by the U.S. Commodity Futures Trading Commission (CFTC), which include live cattle, natural gas, and wheat. See §1.6045-1(a)(5) of the pre-2024 final regulations. (These final regulations also add to the definition of commodity personal property that is traded through regulated futures contracts certified to the CFTC.) These assets also are not financial instruments. Consequently, the term “any other financial instrument” in section 6045(g)(3)(B)(v) should not be read to limit the meaning of the items in the list that came before it. For similar reasons, the rule of last antecedent also does not limit the meaning of digital assets. Prior to the changes made to section 6045 by the Infrastructure Act, the financial instruments language followed the commodities clause. As such, when enacted the financial instruments phrase could not have been intended to limit the item in the list (commodity) that immediately preceded it. Accordingly, the Treasury Department and the IRS understand the inclusion of other financial instruments as potential specified securities as a grant of authority to expand the list of specified securities, not as a provision limiting the meaning of the other asset types listed as specified securities.

One comment suggested that the final regulations should limit the definition of a digital asset to exclude NFTs not used as payment or investment instruments to align the section 6045 reporting rules with other rules and regulatory frameworks. One comment recommended limiting the definition to only digital assets that can be converted to U.S. dollars, another fiat currency, or an asset with market value. Several comments suggested that including all NFTs in the definition of digital assets would be inconsistent with the intended guidance announced in Notice 2023-27, Treatment of Certain Nonfungible Tokens as Collectibles, 2023-15 I.R.B. 634 (April 10, 2023), which indicated that the IRS intends to determine whether an NFT constitutes a collectible under section 408(m) of the Code by using a look-through analysis that looks to the NFT’s associated right or asset. Other comments recommended that the final regulations limit the definition of digital assets to exclude NFTs not used as payment or investment instruments to align the section 6045 reporting rules with the reporting rules for digital assets by foreign governments, such as the Council directive (EU) 2023/2266 of 17 October amending Directive 2011/16/EU on administrative cooperation in the field of taxation, which is popularly known as DAC8. Yet other comments recommended that the final regulations conform to guidelines from the Financial Action Task Force (FATF), an inter-governmental body that sets international standards that aim to prevent money laundering and terrorism financing. FATF guidelines distinguish between those NFTs that are used “as collectibles” from those used “as payment or investment instruments.” Finally, one comment urged the Treasury Department and the IRS to follow the Financial Accounting Standards Board (FASB) standards, which completely exclude NFTs from their definition of digital assets due to their nonfungible nature. FASB, Accounting Standards Update, Intangibles – Goodwill and Other – Crypto Assets (Subtopic 350-60), No. 2023-08, December 2023.

These final regulations do not adopt these comments because they would make the definition of digital assets unduly restrictive. The goal behind information reporting by brokers is to close or significantly reduce the income tax gap from unreported income and to provide information that assists taxpayers. Information reporting generally can achieve that objective when brokers report to the IRS and to their customers the information necessary for customers to report their income. The considerations relevant to a U.S. third party information reporting regime are not the same as the considerations that are relevant to the definition of collectibles under section 408(m), which applies in order to determine assets that have adverse tax consequences if acquired by certain retirement accounts and that are subject to special tax rates. While non-tax policies relating to combating money laundering and terrorism financing or guidelines for generally accepted accounting standards may have some relevance, they are not determinative for Federal tax purposes under the Code. Finally, the Treasury Department and the IRS understand that DAC8 is intended to apply in the same manner as a closely related OECD standard, discussed in the next paragraph. Moreover, NFTs that are actively traded on trading platforms appear to be used for investment purposes in addition to any other purposes. Publicly available information reports that trading in some NFT collections has been in the billions of dollars over time and that 24-hour trading volume in NFTs in 2024 has ranged from $60-410 million. This trading activity suggests that at least some NFT collections have sufficient volume and liquidity to facilitate their use as investments rather than as traditional collectibles.

Another comment suggested that the final regulations should limit the definition of digital assets to exclude NFTs to align the section 6045 definition of digital assets with the definition of “Relevant Crypto-Asset” under the Crypto-Asset Reporting Framework (CARF), a framework for the automatic exchange of information between countries on crypto-assets developed by the Organisation for Economic Co-operation and Development (OECD) and to which the United States is a party. As discussed in Part I.G.2. of this Summary of Comments and Explanation of Revisions, once the United States implements the CARF, U.S. digital asset brokers will need to file information returns under both these final regulations with respect to their U.S. customers, and, under separate final regulations implementing the CARF reporting requirements, with respect to their non-U.S. customers that are resident in jurisdictions implementing the CARF. These final regulations generally attempt to align definitions with those used in the CARF to the extent possible. In this case, however, the final regulations do not adopt this comment because the CARF’s definition of Relevant Crypto-Assets is already consistent with a definition of digital assets that includes NFTs. As noted in paragraph 12 of the CARF’s Commentary on Section IV: Defined terms, although NFTs are often marketed as collectibles, this function does not prevent an NFT from being able to be used for payment or investment purposes. “NFTs that are traded on a marketplace can be used for payment or investment purposes and are therefore to be considered Relevant Crypto-Assets.” See Part I.G.1. of this Summary of Comments and Explanation of Revisions, for a discussion of the United States’ implementation of the CARF.

Notwithstanding that the final regulations include NFTs in the definition of digital assets under section 6045(g)(3)(D), the Treasury Department and the IRS have determined that, pursuant to discretion under section 6045(a), it is appropriate to provide an alternative reporting method for certain types of NFTs to alleviate burdensome reporting. As discussed in Part I.D.3. of this Summary of Comments and Explanation of Revisions, the final regulations have added a new optional alternative reporting method for sales of certain NFTs to allow for aggregate reporting instead of transactional reporting, with a de minimis annual threshold below which no reporting is required. The Treasury Department and the IRS anticipate that the de minimis annual threshold will eliminate reporting on many low-value NFT transactions that are less likely to be used for payment or investment purposes.

3. Closed Loop Assets

The preamble to the proposed regulations stated that the definition of a digital asset was not intended to apply to the types of virtual assets that exist only in a closed system and cannot be sold or exchanged outside that system for fiat currency. The preamble also stated that the definition of digital assets was not intended to cover uses of distributed ledger technology for ordinary commercial purposes, such as tracking inventory or processing orders for purchase and sale transactions, that do not create transferable assets and are therefore not likely to give rise to sales as defined for purposes of the regulations. Several comments requested that the final regulations be revised to provide an exception for closed loop uses in the regulatory text and to add examples illustrating that these types of virtual assets are not included in the definition of a digital asset. Another comment recommended that the final regulations expressly limit the definition of digital assets to only those digital assets that function as currency as described in Notice 2014-21 or that have the capability of being purchased, sold, or exchanged. The Treasury Department and the IRS agree that the text of the final regulations should make clear that transactions involving digital assets in the above-described closed loop environments should not be subject to reporting. The final regulations do not limit the definition of a digital asset as requested to accommodate these comments, however, because it is not clear how the definition could narrowly carve out only these closed loop digital assets without also carving out other assets for which reporting is appropriate. Instead, to address these comments, the final regulations add transactions involving these closed loop digital assets to the list of excepted sales that are not subject to reporting under §1.6045-1(c)(3)(ii). See Part I.C. of this Summary of Comments and Explanation of Revisions, for a discussion of the closed loop transactions added to the list of excepted sales at §1.6045-1(c)(3)(ii).

4. Coordination with Reporting Rules for Securities, Commodities, and Real Estate

The preamble to the proposed regulations noted that the Treasury Department and the IRS are aware that many provisions of the Code incorporate references to the terms security or commodity, and that questions exist as to whether, and if so, when, a digital asset may be treated as a security or a commodity for purposes of those Code sections. Apart from the rules under sections 1001 and 1012 discussed in Part II. of this Summary of Comments and Explanation of Revisions, these final regulations are information reporting regulations, and are therefore not the appropriate vehicle for answering those questions. Accordingly, the treatment of an asset as reportable as a security, commodity, digital asset, or otherwise in these rules applies for purposes of sections 3406, 6045, 6045A, 6045B, 6050W, 6721, and 6722 of the Code, and for certain purposes of sections 1001 and 1012, and should not be construed to apply for any other purpose of the Code, including but not limited to determining whether a digital asset should be classified as a security, commodity, option, securities futures contract, regulated futures contract, or forward contract.

One comment expressed concern that promulgation of final regulations requiring brokers to report on digital asset transactions could be cited by other government agencies to support treating digital assets as securities for purpose of the securities statutes, rules, and regulations. This comment requested that these regulations not take any position on whether digital assets are securities for these other purposes. The Treasury Department and the IRS agree with this comment. The potential characterization of digital assets as securities, commodities, or derivatives for purposes of any other legal regime, such as the Federal securities laws and the Commodity Exchange Act, is outside the scope of these final regulations.

a. Special coordination rules for dual classification assets

Because §1.6045-1(a)(9) of the pre-2024 final regulations (redesignated in the proposed and final regulations as §1.6045-1(a)(9)(i)) require reporting with respect to sales for cash of securities as defined in §1.6045-1(a)(3) and certain commodities as defined in §1.6045-1(a)(5), the proposed regulations included coordination rules to provide certainty to brokers with respect to whether a particular transaction involving securities or certain commodities is reportable as a securities or commodities sale under proposed §1.6045-1(a)(9)(i) (sale of securities or commodities) or as a digital assets sale under proposed §1.6045-1(a)(9)(ii) (sale of digital assets) and to avoid duplicate reporting obligations. Specifically, for transactions involving the sale of a digital asset that also constitutes the sale of a commodity or security (other than options that constitute contracts covered by section 1256(b) of the Code) (dual classification assets), the proposed regulations provided that the broker would report the sale only as a sale of a digital asset and not as a sale of a security or commodity.

Numerous comments raised the concern that requiring brokers that have been historically reporting sales of securities and commodities on Form 1099-B, Proceeds from Broker and Barter Exchange Transactions to report these transactions as sales of digital assets on Form 1099-DA, Digital Asset Proceeds From Broker Transactions would force these brokers to overhaul their existing reporting systems and potentially cause confusion for taxpayers who are not even aware that their securities and commodities have been tokenized. To address this concern, some comments recommended that the digital asset definition be revised to exclude some or all securities and commodities. Other comments recommended revising the coordination rule so that the reporting rules for sales of securities and commodities apply to digital assets that are also securities or commodities. One comment suggested applying the reporting rules for sales of securities and commodities to any digital asset that represents a fund subject to the Investment Company Act of 1940, 15 U.S.C. 80a-1 et seq. (1940 Act Fund), or another highly regulated product outside of 1940 Act Funds.

The final regulations do not adopt the comments recommending that sales of dual classification assets generally be reported as sales of securities or commodities. One of the benefits of treating dual classification assets as digital assets is that it avoids forcing brokers to make determinations about whether the dual classification asset is properly classified as a security or a commodity under current law. For example, a rule that treats all dual classification assets as securities and commodities would require brokers to determine whether a digital asset that represents a governance token is properly classified as a security under final §1.6045-1(a)(3) to determine how to report sales of that digital asset. Moreover, such a rule would affect reporting on digital assets commonly referred to as cryptocurrencies that fit within the definition of a commodity under final §1.6045-1(a)(5)(i) because the trading of regulated futures contracts in that digital asset has been certified to the CFTC. It would be inappropriate for brokers to report these assets as sales of commodities rather than as sales of digital assets because, as is discussed in Part I.F. of this Summary of Comments and Explanation of Revisions, it is important that brokers report basis for these sales.

Other comments offered recommendations designed to limit reporting of dual classification assets under the rules governing sales of securities and commodities. For example, one comment recommended that the reporting rules for sales of securities and commodities apply to any digital asset representing readily ascertainable securities or commodities and not purely blockchain-based digital assets, such as cryptocurrencies or governance tokens, for which treatment as securities or commodities may be uncertain. Another comment recommended that the reporting rules for sales of securities and commodities apply to any digital asset that represents a non-digital asset security or commodity otherwise reportable on Form 1099-B under the reporting rules for sales of securities and commodities or is otherwise backed by collateral that represents such non-digital asset. One comment suggested applying the reporting rules for sales of securities and commodities to any digital asset, the blockchain ledger entry for which solely serves as a record of legal ownership of an underlying security or commodity that is not itself a digital asset. Another comment recommended applying the reporting rules for sales of securities and commodities to dual classification assets that are digitally native to a blockchain that is used simply to record ownership changes. Recognizing that identifying digital assets that represent securities and commodities that are not themselves digital assets could be burdensome, one comment recommended that when information is not available for brokers to make these determinations about dual classification assets, the broker should report the transaction as a sale of a digital asset. Another comment requested that the final regulations include a safe harbor rule providing that no penalties will be imposed on a broker who consistently and accurately reports the sale of dual classification assets under either the reporting rules for sales of securities and commodities (on Form 1099-B) or for sales of digital assets (on Form 1099-DA) based on the broker’s reasonable determination that the chosen reporting method is correct because it may be administratively difficult for brokers to examine every dual classification asset to make a determination based on the nature of the asset.

Numerous comments also focused on the circumstances that may give rise to securities and commodities being treated as digital assets. For example, one comment indicated that the proposed coordination rule would inadvertently capture transactions involving securities and commodities for which brokers use distributed ledger technology, shared ledgers, or similar technology merely to facilitate the processing, clearing, or settlement of orders between well-regulated brokers and other financial institutions. To address this concern, several comments recommended that the reporting rules for sales of securities and commodities apply only to digital assets that are more appropriately categorized within a traditional asset class (for example, as a security with an effective registration statement filed under the Securities Act of 1933) and that are issued, stored, or transferred through a distributed ledger that is a regulated clearing agency system in compliance with all applicable Federal and State securities laws. Another comment recommended addressing this problem by making the information required to be reported for digital asset sales (on Form 1099-DA) not more burdensome than that for securities and commodities (on Form 1099-B). Another comment requested that, if brokers are required to report these dual classification assets on the Form 1099-DA, the final regulations allow brokers to optionally make appropriate basis adjustments for dual classification assets that are securities. This comment also recommended revising the rules in §1.6045-1(d)(2)(iv)(B) of the pre-2024 final regulations to permit (but not require) brokers to take into account information about a covered security other than what is furnished on a transfer statement or issuer statement and to provide penalty relief under certain circumstances to brokers that take such information into account. Finally, one comment recommended providing written clarity that even though wash sale adjustment rules do not apply to digital assets, they still apply to tokenized securities such as, for example, 1940 Act Funds.

The Treasury Department and the IRS have concluded that it is generally not appropriate to permit optional approaches to reporting dual classification assets because the underlying reporting requirements for securities and commodities are significantly different from those for digital assets due, in large part, to industry differences and the timing of when the reporting rules were first implemented. Although the proposed requirement for brokers to report transaction identification numbers and digital asset addresses has been removed in these final regulations (see Part I.D. of this Summary of Comments and Explanation of Revisions), there are several remaining differences in the basis reporting requirements for securities and commodities as compared to digital assets. For example, unlike brokers effecting sales of digital assets, brokers effecting sales of commodities are not required to report the customer’s adjusted basis for those commodities because commodities are not included in the definition of covered securities. Additionally, brokers effecting sales of stock, other than stock for which the average basis method is available under §1.1012-1(e), must generally report the adjusted basis of these shares to the extent they were acquired for cash in an account on or after January 1, 2011, and generally must report the adjusted basis on shares of stock for which the average basis method is available to the extent those shares were acquired for cash in an account on or after January 1, 2012. These brokers of stock that are covered securities under final §1.6045-1(a)(15)(i)(A) or (B) must also send transfer statements to other brokers under section 6045A when their customers move that stock to another broker.

In contrast, as discussed in Part I.F. of this Summary of Comments and Explanation of Revisions, under the final regulations, brokers effecting sales of digital assets that are covered securities under final §1.6045-1(a)(15)(i)(J) are required to report the adjusted basis of those digital assets only if they were acquired for cash, stored-value cards, different digital assets, or certain other property or services in the customer’s account by such brokers providing custodial services for such digital assets on or after January 1, 2026. Additionally, these brokers are not currently required to send transfer statements to other brokers under section 6045A when their customers transfer digital assets that are specified securities to another broker. Indeed, the details of how section 6045A reporting will apply to brokers of digital assets will not be addressed until a future notice of proposed rulemaking. Accordingly, whether the sale of a dual classification asset is treated as a sale of a security or commodity under final §1.6045-1(a)(9)(i) or as a sale of a digital asset under final §1.6045-1(a)(9)(ii) has consequences beyond the particular form that the broker must use when filing returns with respect to those sales.

Given these different basis reporting requirements and transfer statement obligations under section 6045A, the Treasury Department and the IRS have determined that, except in the case of certain exceptions described in the next several paragraphs, it is not appropriate to treat dual classification assets as subject only to the pre-2024 final regulations (that is, required to report the transactions under final §1.6045-1(d)(2)(i)(A) as sales described in final §1.6045-1(a)(9)(i)) for securities and commodities if those assets can be traded on public blockchains and custodied by customers. Accordingly, final §1.6045-1(c)(8)(i) provides that brokers must generally treat sales of dual classification assets only as a sale of a digital asset under final §1.6045-1(a)(9)(ii) and only as a sale of a specified security that is a digital asset under final §1.6045-1(a)(14)(v) or (vi). As such, the broker must apply the digital asset reporting rules for the information required to be reported for such sale and file the return on Form 1099-DA. Further, as discussed in Part IV. of this Summary of Comments and Explanation of Revisions, brokers are not required to send transfer statements under final §1.6045A-1(a)(1)(vi) with respect to the transfer of these dual classification assets that are reportable as digital assets. Additionally, final §1.6045-1(d)(2)(iv)(B) does not permit brokers to take into account any other information, including information received from a customer or third party, with respect to covered securities that are digital assets, although brokers may take customer-provided acquisition information into account for purposes of identifying which units are sold, disposed of, or transferred under final §1.6045-1(d)(2)(ii)(A).

However, to accommodate the comments relating to the application of the various basis adjustment rules, including the wash sale adjustment rules, and other important information applicable to dual classification assets that represent an interest in a traditional security, final §1.6045-1(c)(8)(i)(D) requires the broker to report certain additional information with respect to any dual classification asset that is a tokenized security. For this purpose, any dual classification asset that provides the holder with an interest in another asset that is a security under final §1.6045-1(a)(3), other than a security that is also a digital asset, is a tokenized security. This description is intended to apply when the digital asset represents an interest in a separate, traditional, financial asset that is reportable as a security. For example, a digital asset that represents an ownership interest in a traditional share of stock in a 1940 Act Fund or another corporation would be a tokenized security. A dual classification asset that is an interest in a trust or partnership that holds assets that are securities under final §1.6045-1(a)(3), other than securities that are also digital assets, also would be a tokenized security.

In addition, an asset the offer and sale of which was registered with the U.S. Securities and Exchange Commission (SEC) (other than an asset treated as a security for securities law purposes solely as an investment contract) is also treated as a tokenized security. This part of the description of tokenized securities is intended to refer to a digital asset that is also a security within the meaning of final §1.6045-1(a)(3) but does not represent an interest in a separate financial asset. A bond that exists solely in tokenized form would be an example of such a tokenized security, if the bond was issued pursuant to a registration statement approved by the SEC. The reference to whether an asset’s offer and sale was registered with the SEC, other than solely as an investment contract, is intended to limit the scope of the term tokenized security to digital forms of traditional financial assets, and not to capture assets native to the digital asset ecosystem. The reference to registration of an asset’s offer and sale with the SEC is not intended to imply that such assets are necessarily securities for Federal income tax purposes or for purposes of final §1.6045-1(a)(3). Additionally, no inference is intended as to how the Federal securities laws apply to sales of digital assets within the meaning of final §1.6045-1(a)(19), as the interpretation or applicability of those laws are outside the scope of these final regulations.

For the avoidance of doubt, final §1.6045-1(c)(8)(i)(D) provides that a qualifying stablecoin is not treated as a tokenized security for purposes of these special rules. For sales of tokenized securities, final §1.6045-1(c)(8)(i)(D) provides that the broker must report additional information required by final §1.6045-1(d)(2)(i)(B)(6), generally relating to gross proceeds. Final §1.6045-1(d)(2)(i)(B)(6) requires that the broker report the Committee on Uniform Security Identification Procedures (CUSIP) number of the security sold, any information related to options required under final §1.6045-1(m), any information related to debt instruments under final §1.6045-1(n), and any other information required by the form or instructions. In addition, final §1.6045-1(c)(8)(i)(D) provides that the broker must report additional information required by final §1.6045-1(d)(2)(i)(D)(4) (relating to reporting for basis and holding period) for sales of tokenized securities, except that the broker is not required to report such information for a tokenized security that is an interest in another asset that is a security under final §1.6045-1(a)(3), other than a security that is also a digital asset, unless the tokenized security is also a specified security under final §1.6045-1(a)(14)(i), (ii), (iii), or (iv). Accordingly, because a trust or partnership interest is not a specified security within the meaning of those paragraphs, a broker is not required to report basis information with respect to a tokenized security that is an interest in a trust or partnership that holds assets that are securities under final §1.6045-1(a)(3), other than securities that are also digital assets.

Final §1.6045-1(d)(2)(i)(D)(4) provides specific rules for reporting basis and related information for tokenized securities. It cross-references the wash sale rules in final §1.6045-1(d)(6)(iii)(A)(2) and (d)(7)(ii)(A)(2), which rules have also been revised to specifically apply to tokenized securities. These wash sale reporting rules apply only to assets treated as stock or securities within the meaning of section 1091 of the Code. They apply regardless of whether the taxpayer buys or sells a tokenized security. For example, if a taxpayer sells a tokenized security (or the underlying traditional stock or security) at a loss and buys the same tokenized security (or the underlying traditional stock or security) within the 30-day period before or after the sale, and the other conditions to the wash sale reporting rules are satisfied, the broker would be required to take the wash sale reporting rules into account in reporting the loss and the basis of the newly acquired asset. Final §1.6045-1(d)(2)(i)(D)(4) also cross-references the average basis rules in final §1.6045-1(d)(6)(v), which have been revised to apply to any stock that is also a tokenized security, and the rules related to options and debt instruments in final §1.6045-1(m) and (n). Accordingly, the information reportable for tokenized securities on Form 1099-DA should be similar to the information reportable for traditional securities on Form 1099-B, except that under final §1.6045A-1(a)(1)(vi), no transfer statement is required with respect to the transfer of tokenized securities, though penalty relief is provided if the broker voluntarily chooses to provide a transfer statement with respect to tokenized securities. Additionally, until the Treasury Department and the IRS determine which third party information is sufficiently reliable, final §1.6045-1(d)(2)(iv)(B) provides that brokers are not permitted to take into account information about covered securities that are digital assets other than what is furnished on a transfer statement or issuer statement, although brokers may take customer-provided acquisition information into account for purposes of identifying which units are sold, disposed of, or transferred under final §1.6045-1(d)(2)(ii)(A). The Treasury Department and the IRS intend to provide additional guidance on how to report tokenized securities in the instructions to Form 1099-DA.

Final §1.6045-1(d)(2)(i)(D)(3) requires that, for purposes of determining the basis and holding period information required in final §1.6045-1(d)(2)(i)(D)(1) and (2), the rules related to options in final §1.6045-1(m) apply, both with respect to the option and also with respect to any asset delivered in settlement of an option. Accordingly, an option that is itself a digital asset, on an asset that is also a digital asset, is subject to the same reporting rules as other options.

Additionally, in response to the comments described above, the Treasury Department and the IRS have determined that the final regulations should include three exceptions to the rules requiring that dual classification assets be reported as digital assets, for the reasons described herein. Those exceptions apply to dual classification assets cleared or settled on a limited-access regulated network, to dual classification assets that are section 1256 contracts, and to dual classification assets that are shares in money market funds.

First, the Treasury Department and the IRS agree that it is not appropriate to disrupt reporting on dual classification assets that are treated as digital assets solely because distributed ledger technology is used to facilitate the processing, clearing, or settlement of orders between regulated financial entities. Accordingly, in response to the comments submitted, final §1.6045-1(c)(8)(iii) adds a new exception to the coordination rule for any sale of a dual classification asset that is a digital asset solely because the sale of such asset is cleared or settled on a limited-access regulated network. Under this exception, such a sale will be treated as a sale described in final §1.6045-1(a)(9)(i) (reportable on the Form 1099-B) and not as a digital asset sale described in final §1.6045-1(a)(9)(ii) (reportable on the Form 1099-DA). Additionally, such a sale must be treated as a sale of a specified security under final §1.6045-1(a)(14)(i), (ii), (iii), or (iv) to the extent applicable, and not as a sale of a specified security that is a digital asset under final §1.6045-1(a)(14)(v) or (vi). For all other purposes of this section including transfers, a dual classification asset that is a digital asset solely because it is cleared or settled on a limited-access regulated network is not treated as a digital asset and is not reportable as a digital asset. Accordingly, depending on the type of the asset, the asset may be a covered security under final §1.6045-1(a)(15)(i)(A) through (G) (if purchased in an account on or after January 1, 2011 through 2016, as applicable) rather than a digital asset covered security under final §1.6045-1(a)(15)(i)(H), (J) or (K) (if purchased in an account on or after January 1, 2026). Thus, brokers are required under section 6045A to provide transfer statements with respect to transfers of these dual classification assets, and the rules set forth in final §1.6045-1(d)(2)(iv)(A) and (B), regarding the broker’s obligation to take into account the information reported on those statements and certain other customer provided information also apply.

Final §1.6045-1(c)(8)(iii)(B) sets forth three different types of limited-access regulated network for which this rule applies. The first type of limited-access network is described as a cryptographically secured distributed ledger or network of interoperable distributed ledgers that provide clearance or settlement services and provide access only to a group of persons made up of registered dealers in securities or commodities, banks and similar financial institutions, common trust funds, or futures commission merchants. Final §1.6045-1(c)(8)(iii)(B)(1)(i). As used in this rule, an interoperable distributed ledger means a group of distributed ledgers that permit digital assets to travel from one permissioned distributed ledger (for example, at one securities broker) to another permissioned distributed ledger (at another securities broker). In such cases, while the clearance or settlement of the dual classification asset is on a network of permissioned distributed ledgers, it is anticipated that the asset will remain in a traditional securities or commodities account from the perspective of an investor in the asset and so can readily be reported as a security or commodity under existing rules.

The second type of limited-access network is also described as a cryptographically secured distributed ledger or network of interoperable distributed ledgers that provide clearance or settlement services, but this type of limited-access network is distinguishable from the first type because it is provided by an entity that has registered with the SEC as a clearing agency, or has received an exemption order from the SEC as a clearing agency, under section 17A of the Securities Exchange Act of 1934. Additionally, the entity must provide access to the network exclusively to network participants, who are not required to be registered dealers in securities or commodities, banks and similar financial institutions, common trust funds, or futures commission merchants, although it is anticipated that participants typically will be securities brokers and other regulated financial institutions. Final §1.6045-1(c)(8)(iii)(B)(1)(ii). For example, dual classification assets cleared and settled through a central clearing agency that clears and settles high volumes of equity and debt transactions on a daily basis through automated systems for participants that are financial market participants may be reportable as securities under this exception if the clearance or settlement takes place on a cryptographically secured distributed ledger or network of interoperable distributed ledgers.

Finally, the third type of limited-access regulated network is a cryptographically secured distributed ledger controlled by a single person that is a registered dealer in securities or commodities, a futures commission merchant, a bank or similar financial institution, a real estate investment trust, a common trust fund, or a 1940 Act Fund, that permits the ledger to be used solely by itself and its affiliates (and not by any customers or investors) to clear or settle sales of assets. Final §1.6045-1(c)(8)(iii)(B)(2). As with the other types of limited-access regulated network, it is anticipated that from an investor perspective the assets will remain in a traditional securities or commodities account.

This exception in final §1.6045-1(c)(8)(iii) is limited to dual classification assets that are digital assets solely because the sale of such dual classification asset is cleared or settled on a limited-access regulated network. Accordingly, a digital asset commonly referred to as a cryptocurrency that fits within the definition of commodity under final §1.6045-1(a)(5)(i) because the trading of regulated futures contracts in that digital asset have been approved by or certified to the CFTC will not be eligible for this rule because the cryptocurrency meets the definition of a digital asset for reasons other than because it is cleared or settled on a limited-access regulated network. Given the requirement that the sole reason that the security or commodity is a digital asset is that transactions involving those assets are cleared or settled on a limited-access regulated network, it is anticipated that brokers will have sufficient information to be able to determine how to report the assets in question under these revised rules. Accordingly, the request for a safe harbor that would allow brokers to avoid penalties if they consistently and accurately report sales of dual classification assets under either final §1.6045-1(d)(2)(i)(A) (on Form 1099-B) or final §1.6045-1(d)(2)(i)(B) and (D) as a digital asset (on Form 1099-DA) is not adopted as it is unnecessary.

The second exception to the general dual classification asset coordination rule in final §1.6045-1(c)(8)(i) treating such assets as digital assets was included in the proposed regulations. Proposed §1.6045-1(c)(8)(iii) provided that digital asset options or other contracts that are also section 1256 contracts should be reported under the rules set forth in §1.6045-1(c)(5) of the pre-2024 final regulations for contracts that are section 1256 contracts and not under the proposed rules for digital assets. The final regulations retain this exception and redesignate it as final §1.6045-1(c)(8)(ii). Accordingly, under this rule, for the disposition of a contract that is a section 1256 contract, reporting is required under §1.6045-1(c)(5) of the pre-2024 final regulations regardless of whether the contract disposed of is a non-digital asset contract or a digital asset contract or whether the contract was issued with respect to digital asset or non-digital asset underlying property. One comment raised a concern that the proposed rule did not make it clear that information reporting for a section 1256 contract subject to information reporting under section 6045 should be reported on a Form 1099-B regardless of whether the contract is or is not a digital asset. The final regulations respond to this concern by providing additional clarification to the text of §1.6045-1(c)(5)(i) of the pre-2024 final regulations to make it clear that reporting for all section 1256 contracts should be on Form 1099-B. Accordingly, information reporting for section 1256 contracts in digital asset form will be on Form 1099-B and not on Form 1099-DA.