)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

- HIGHLIGHTS OF THIS ISSUE

- Part III

- Reference Price for Section 45I Credit for Production of Natural Gas from Marginal Wells During Taxable Years Beginning in Calendar Year 2026

- Superfund Tax on Chemical Substances; Notice of Determinations to Add Substances to List of Taxable Substances

- Transfer Tax Safe Harbor for Certain Contributions to Trump Accounts

- Part IV

- Deletions From Cumulative List of Organizations, Contributions to Which are Deductible Under Section 170 of the Code

- Definition of Terms

- Numerical Finding List1

- Finding List of Current Actions on Previously Published Items1

- How to get the Internal Revenue Bulletin

Internal Revenue Bulletin: 2026-29

July 13, 2026

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

This Announcement advises the public that the Internal Revenue Service is revising the optional standard mileage rates for substantiating the costs of operating an automobile for business, medical or moving purposes. These revised rates are effective beginning July 1, 2026. This Announcement modifies Notice 2026-10.

This is a revenue procedure that provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) satisfy certain specified conditions. If the conditions are satisfied, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax exclusion applies. As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions.

26 CFR 601.601: Rules and regulations. (Also Part I, Sections 530A, 2010, 2503, 2505, 2642, 2662, 6019.)

This notice publishes the 2026 calendar-year inflation adjustment factor for the section 45U zero-emission nuclear power production credit, as well as the inflation adjustment factors and corresponding applicable amounts for the section 45V clean hydrogen production credit and the section 45Z clean fuel production credit, respectively. The inflation adjustment factors (applicable to sections 45U, 45V, and 45Z) and the applicable amounts (in the case of sections 45V and 45Z) are used to determine the amount of the credit allowable under sections 45U, 45V, and 45Z.

This notice publishes the applicable reference price and credit amount under § 45I of the Internal Revenue Code for qualified natural gas production from qualified marginal wells during taxable years beginning in calendar year 2026. The applicable reference price and credit amount are used in determining the marginal well production credit under § 45I for qualified natural gas production.

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

This notice publishes the inflation adjustment factors and applicable amounts, as appropriate, for calendar year 2026 for the zero-emission nuclear power production credit under § 45U of the Internal Revenue Code (Code) (the § 45U credit), the credit for production of clean hydrogen under § 45V of the Code (the § 45V credit), and the clean fuel production credit under § 45Z of the Code (the § 45Z credit). These inflation adjustment factors and applicable amounts, as appropriate, are used to determine the corresponding credit amounts under §§ 45U, 45V, and 45Z.

.01 Section 45U.

Section 45U was added to the Code by section 13105 of Public Law 117-169, 136 Stat. 1818, 1929 (August 16, 2022), commonly known as the Inflation Reduction Act of 2022 (IRA), to provide an income tax credit for producing electricity at a qualified nuclear power facility.

Section 45U(a) provides that, for purposes of § 38, the § 45U credit for any taxable year is an amount equal to the amount by which the product of 0.3 cents (the amount provided in § 45U(a)(1)(A)) and the kilowatt hours of electricity the taxpayer produced at a qualified nuclear power facility and sold to an unrelated person during the taxable year, exceeds the reduction amount for that taxable year.

Section 45U(b)(2) defines the reduction amount as the lesser of: (1) the amount determined under § 45U(a) before application of the reduction amount, or (2) the amount equal to 16 percent of the excess of, subject to other rules regarding the treatment of certain receipts, the gross receipts from any electricity produced by a qualified nuclear power facility (including any electricity services or products provided in conjunction with the electricity produced by such facility) and sold to an unrelated person during the taxable year, over the amount equal to the product of 2.5 cents (the amount provided in § 45U(b)(2)(A)(ii)(II)(aa)), multiplied by the kilowatt hours of electricity determined in § 45U(a).

Section 45U(c)(1) provides that the 0.3 cent amount in § 45U(a)(1)(A) and the 2.5 cent amount in § 45U(b)(2)(A)(ii)(II)(aa) are each adjusted by multiplying such amounts by the inflation adjustment factor (as determined under § 45(e)(2), by substituting “2023” for “1992” in § 45(e)(2)(B)) for the calendar year in which the sale of electricity (as defined in § 45U(b)(3)) occurred. If the 0.3 cent and 2.5 cent amounts, as increased under § 45U(c)(1), are not multiples of 0.05 cent and 0.1 cent, respectively, then such amounts are rounded to the nearest multiples of 0.05 cent and 0.1 cent, respectively.

.02 Section 45V.

Section 45V was added to the Code by IRA section 13204, 136 Stat. at 1935, to provide an income tax credit for producing qualified clean hydrogen.

Section 45V(a) provides that, for purposes of § 38, the § 45V credit for any taxable year is an amount equal to the product of (1) the kilograms of qualified clean hydrogen produced by the taxpayer during such taxable year at a qualified clean hydrogen production facility during the 10-year period beginning on the date such facility was originally placed in service, and (2) the applicable amount as determined under § 45V(b) with respect to such hydrogen.

Section 45V(b)(1) provides that, for purposes of § 45V(a)(2), the applicable amount is an amount equal to the applicable percentage of $0.60. If the amount so determined is not a multiple of 0.1 cent, then such amount is rounded to the nearest multiple of 0.1 cent.

Section 45V(b)(2) provides that, for purposes of § 45V(b)(1), the applicable percentage is determined based on the lifecycle greenhouse gas emissions (lifecycle GHG emissions) rate of the process used to produce any qualified clean hydrogen as follows: (i) if the lifecycle GHG emissions rate is not greater than 4 kilograms of carbon dioxide equivalent (CO2e) per kilogram of hydrogen, and not less than 2.5 kilograms of CO2e per kilogram of hydrogen, then the applicable percentage is 20 percent; (ii) if the lifecycle GHG emissions rate is less than 2.5 kilograms of CO2e per kilogram of hydrogen, and not less than 1.5 kilograms of CO2e per kilogram of hydrogen, then the applicable percentage is 25 percent; (iii) if the lifecycle GHG emissions rate is less than 1.5 kilograms of CO2e per kilogram of hydrogen, and not less than 0.45 kilograms of CO2e per kilogram of hydrogen, then the applicable percentage is 33.4 percent; and (iv) if the lifecycle GHG emissions rate is less than 0.45 kilograms of CO2e per kilogram of hydrogen, then the applicable percentage is 100 percent.

Section 45V(b)(3) provides that the $0.60 amount in § 45V(b)(1) is adjusted by multiplying such amount by the inflation adjustment factor (as determined under § 45(e)(2), by substituting “2022” for “1992” in § 45(e)(2)(B)) for the calendar year in which the qualified clean hydrogen is produced. If any amount as increased under § 45V(b)(3) is not a multiple of 0.1 cent, then such amount is rounded to the nearest multiple of 0.1 cent.

.03 Section 45Z.

Section 45Z was added to the Code by IRA section 13704, 136 Stat. at 1997, to provide an income tax credit for producing clean transportation fuel.

Section 45Z(a)(1) provides that, for purposes of § 38, the § 45Z credit for any taxable year is an amount equal to the product of (1) the applicable amount per gallon (or gallon equivalent) with respect to any transportation fuel which is produced by the taxpayer at a qualified facility and sold by the taxpayer in a specific manner during the taxable year, and (2) the emissions factor for such fuel as determined under § 45Z(b).

As enacted by the IRA, § 45Z(a)(2) and (3) provided the applicable amounts for transportation fuels. Specifically, for transportation fuel that was not a sustainable aviation fuel (non-SAF transportation fuel), the applicable amount was 20 cents under § 45Z(a)(2)(A), or $1.00 under § 45Z(a)(2)(B). For transportation fuel that was a sustainable aviation fuel (SAF transportation fuel), the applicable amount was 35 cents under § 45Z(a)(3)(A)(i), or $1.75 under § 45Z(a)(3)(A)(ii).

Section 45Z refers to the lower amount for a fuel as the base amount and to the higher amount for a fuel as the alternative amount. A taxpayer uses the alternative amount if it produces transportation fuel at a qualified facility that satisfies certain prevailing wage and apprenticeship requirements.

Section 70521(g)(2) of Public Law 119-21, 139 Stat. 72, 278 (July 4, 2025), commonly known as the One, Big, Beautiful Bill Act, amended § 45Z by eliminating the higher applicable amounts for SAF transportation fuel. This amendment applies to fuel produced after December 31, 2025. Thus, for all transportation fuel produced after December 31, 2025, the applicable amount is either 20 cents or $1.00 as provided in § 45Z(a)(2). However, for transportation fuel produced between January 1, 2025, and December 31, 2025, the applicable amounts are those as enacted under the IRA and differ for SAF and non-SAF transportation fuel.

Section 45Z(c)(1) provides that, for calendar years beginning after 2024, the applicable amount must be adjusted by multiplying such amount by the inflation adjustment factor for the calendar year in which the sale of the transportation fuel occurs. Any amount adjusted under § 45Z(c)(1) must be rounded to the nearest cent. Section 45Z(c)(2) provides that the inflation adjustment factor for the § 45Z credit is the inflation adjustment factor determined and published by the Secretary of the Treasury or his delegate pursuant to § 45Y(c), determined by substituting “calendar year 2022” for “calendar year 1992” in § 45Y(c)(3).

.04 Sections 45(e)(2)(B) and 45Y(c)(3).

Sections 45(e)(2)(B) and 45Y(c)(3) define the term inflation adjustment factor as, with respect to a calendar year, a fraction, the numerator of which is the GDP implicit price deflator for the preceding calendar year and the denominator of which is the GDP implicit price deflator for the calendar year 1992. Under both statutes, the term GDP implicit price deflator means the most recent revision of the implicit price deflator for the gross domestic product as computed and published by the Department of Commerce before March 15 of the calendar year.

.01 2026 Section 45U Inflation Adjustment Factor.

For purposes of § 45U(c)(1), for sales of electricity occurring in calendar year 2026, the inflation adjustment factor is a fraction, the numerator of which is the GDP implicit price deflator for 2025 (128.986) and the denominator of which is the GDP implicit price deflator for 2023 (122.39), which yields an inflation adjustment factor of 1.0539.

For sales of electricity occurring in calendar year 2026, the amount provided in § 45U(a)(1)(A) is 0.3 cents (0.3 cents (or $0.003) x 1.0539, then rounded to the nearest multiple of 0.05 cent). The amount provided in § 45U(b)(2)(A)(ii)(II)(aa) is 2.6 cents (2.5 cents (or $0.025) x 1.0539, then rounded to the nearest multiple of 0.1 cent).

.02 2026 Section 45V Inflation Adjustment Factor and Applicable Amount.

For purposes of § 45V(b)(3), for qualified clean hydrogen produced in calendar year 2026, the inflation adjustment factor is a fraction, the numerator of which is the GDP implicit price deflator for 2025 (128.986) and the denominator of which is the GDP implicit price deflator for 2022 (118.023), which yields an inflation adjustment factor of 1.0929.

For qualified clean hydrogen produced in calendar year 2026, the applicable amount determined under § 45V(b)(1) is the product of $0.656 ($0.60 x 1.0929, then rounded to the nearest multiple of 0.1 cent) and the applicable percentage, which depends on the lifecycle GHG emissions rate of the qualified clean hydrogen production process. Thus, for qualified clean hydrogen produced through a process that results in a lifecycle GHG emissions rate of:

(i) not greater than 4 kilograms of CO2e per kilogram of hydrogen, and not less than 2.5 kilograms of CO2e per kilogram of hydrogen, the applicable amount is $0.131;

(ii) less than 2.5 kilograms of CO2e per kilogram of hydrogen, and not less than 1.5 kilograms of CO2e per kilogram of hydrogen, the applicable amount is $0.164;

(iii) less than 1.5 kilograms of CO2e per kilogram of hydrogen, and not less than 0.45 kilograms of CO2e per kilogram of hydrogen, the applicable amount is $0.219; and

(iv) less than 0.45 kilograms of CO2e per kilogram of hydrogen, the applicable amount is $0.656.

.03 2026 Section 45Z Inflation Adjustment Factor and Applicable Amount.

For purposes of § 45Z(c), for transportation fuel sold in calendar year 2026, the inflation adjustment factor is a fraction, the numerator of which is the GDP implicit price deflator for 2025 (128.986) and the denominator of which is the GDP implicit price deflator for 2022 (118.023), which yields an inflation adjustment factor of 1.0929.

For all transportation fuel produced and sold in calendar year 2026, and for non-SAF transportation fuel produced in calendar year 2025 and sold in calendar year 2026:

(i) The base amount is 22 cents (20 cents x 1.0929, then rounded to the nearest cent) under § 45Z(a)(2)(A).

(ii) The alternative amount is $1.09 ($1.00 x 1.0929, then rounded to the nearest cent) under § 45Z(a)(2)(B).

For SAF transportation fuel produced in calendar year 2025 and sold in calendar year 2026:

(i) The base amount is 38 cents (35 cents x 1.0929, then rounded to the nearest cent) under § 45Z(a)(3)(A)(i) as enacted by IRA § 13704.

(ii) The alternative amount is $1.91 ($1.75 x 1.0929, then rounded to the nearest cent) under § 45Z(a)(3)(A)(ii) as enacted by IRA § 13704.

The principal authors of this notice are Whitney Brady, Glenn Kats, and Andrew Clark of the Office of Associate Chief Counsel (Energy, Credits, and Excise Tax). For further information regarding this notice contact Whitney Brady at (202) 317-6325, Glenn Kats at (202) 317-3995, or Andrew Clark at (202) 317-6855 (not toll-free numbers).

This notice provides the applicable reference price for qualified natural gas production from qualified marginal wells during taxable years beginning in calendar year 2026 for the purpose of determining the marginal well production credit (MWC) under § 45I of the Internal Revenue Code. The applicable reference price for taxable years beginning in calendar year 2026 is $2.20 per 1,000 cubic feet (Mcf).

This notice also provides the credit amount used for the purpose of determining the MWC for taxable years beginning in calendar year 2026. The credit amount is determined using the 2026 inflation adjustment factor of 1.6295 and the applicable reference price of $2.20 per Mcf. The credit amount for taxable years beginning in calendar year 2026 is $0.81 per Mcf.

Section 45I(a), as it relates to qualified natural gas production, provides that, for purposes of § 38, the MWC for any taxable year is an amount equal to the product of (1) the credit amount and (2) the qualified natural gas production that is attributable to the taxpayer.

Section 45I(c)(1) provides that “qualified natural gas production” means domestic natural gas produced from a qualified marginal well. Section 45I(c)(3)(A) provides that a qualified marginal well is a domestic well (i) the production from which during the taxable year is treated as marginal production under § 613A(c)(6), or (ii) which, during the taxable year (I) has average production of not more than 25 barrel-of-oil equivalents per day, and (II) produces water at a rate not less than 95 percent of total well effluent.

Section 613A(c)(6)(D) and (E) provide that “marginal production” means domestic natural gas produced during any taxable year from a property which is a stripper well property for the calendar year in which the taxable year begins. A “stripper well property” is, with respect to any calendar year, any property producing not more than 15 barrel equivalents per day, determined by dividing the average daily production of domestic crude oil and domestic natural gas from producing wells on the property for such calendar year by the number of such wells.

Section 45I(c)(2)(A) provides that generally only the first 1,095 barrels or barrel-of-oil equivalents (as defined in § 45K(d)(5)) produced during the taxable year qualify for the MWC. This limitation is proportionately reduced in the case of a short taxable year or in the case of a well that is not capable of production each day of a taxable year. See § 45I(c)(2)(B). The number of wells on which a taxpayer may claim the MWC is not limited.

Section 45I(d)(2) provides that to claim the credit a taxpayer must hold an operating interest in the qualified marginal well producing the natural gas to which the credit relates. Under § 45I(d)(1) if a well is owned by more than one owner and the natural gas production exceeds the limitation under § 45I(c)(2), the qualifying natural gas production attributable to the taxpayer is determined on the basis of the ratio which the taxpayer’s revenue interest in the production bears to the aggregate of the revenue interests of all operating interest owners in the production. Finally, § 45I(d)(3) provides that the MWC is not allowable if the taxpayer is also eligible to claim the § 45K nonconventional sources credit for the taxable year, unless the taxpayer elects not to claim the credit under § 45K for the well.

For purposes of § 45I(a)(1), the credit amount is 50 cents (adjusted for inflation) per Mcf of qualified natural gas production (tentative credit amount). See § 45I(b)(1)(B) and (b)(2)(B).

Section 45I(b)(2)(A) and (B) provide that the tentative credit amount (adjusted for inflation) is reduced (but not below zero) to the extent that the applicable reference price exceeds $1.67 (adjusted for inflation). More specifically, § 45I(b)(2)(A) provides that the tentative credit amount (adjusted for inflation) is reduced by an amount which bears the same ratio to the tentative credit amount (adjusted for inflation) as the excess (if any) of the applicable reference price over $1.67 (adjusted for inflation), bears to $0.33 (adjusted for inflation). As a result, the MWC is not available if the applicable reference price for qualified natural gas production is $2.00 (adjusted for inflation) or more.

Section 45I(b)(2)(A) also provides that the applicable reference price for a taxable year is the reference price for the calendar year preceding the calendar year in which the taxable year begins. Section 45I(b)(2)(C)(ii) provides that the term “reference price” means, with respect to any calendar year, in the case of qualified natural gas production, the Secretary’s estimate of the annual average wellhead price per Mcf for all domestic natural gas.

Section 45I(b)(2)(B) provides that in the case of any taxable year beginning in a calendar year after 2005, each of the dollar amounts contained in § 45I(b)(2)(A) will be increased to an amount equal to such dollar amount multiplied by the inflation adjustment factor for such calendar year (determined under § 43(b)(3)(B) by substituting “2004” for “1990”).

.1 Inflation Adjustment. The inflation adjustment factor under § 45I(b)(2)(B) for calendar year 2026 is 1.6295.

.2 Reference Price. The Secretary’s estimate of the calendar year 2025 annual average wellhead price per Mcf for all domestic natural gas under § 45I(b)(2)(C)(ii) was calculated by applying the Producer Price Index commodity index for “Natural Gas from the Wellhead” (WPU053101051)1 published by the Bureau of Labor Statistics (BLS) as part of its Producer Price Index program, to the 2024 annual average wellhead price ($1.64) published in Notice 2025-34, 2025-27 I.R.B. 6. The annual Producer Price Index commodity index for natural gas published by the BLS was 50.869 in 2024 and 68.301 in 2025, which implies a ratio of 2025 to 2024 average wellhead prices of 1.343 (68.301/50.869). Therefore, the Secretary’s estimate of the calendar year 2025 annual average wellhead price per Mcf for all domestic natural gas is $2.20 per Mcf (1.343 × $1.64 per Mcf).

For years after 2025, the Secretary intends to continue calculating the reference price by application of the Producer Price Index commodity index for “Natural Gas from the Wellhead” (WPU053101051) published by the BLS to the previous year’s reference price.

Under § 45I(b)(1)(B) and (2)(B), the tentative credit amount used to calculate the MWC for taxable years beginning in calendar year 2026 is $0.81 per Mcf ($0.50 × 1.6295 inflation adjustment factor).

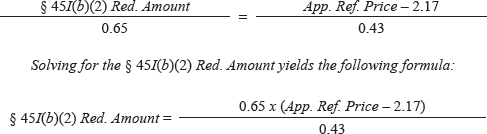

Pursuant to § 45I(b)(2)(A), the tentative credit amount ($0.81) is reduced (but not below zero) by an amount (the Reduction Amount) which bears the same ratio to such amount as (i) the excess (if any) of the applicable reference price ($2.20) over $2.72 ($1.67 × 1.6295 inflation adjustment factor), bears to (ii) $0.54 ($0.33 × 1.6295 inflation adjustment factor). The Reduction Amount (as adjusted for inflation) is computed as follows:

The Reduction Amount is -$0.78 (($2.20 - $2.72) ÷ $0.54 × $0.81), which is less than zero, therefore, the tentative credit amount ($0.81) is not reduced.

This notice is effective for qualified natural gas production during taxable years beginning in calendar year 2026.

The principal author of this notice is Alan W. Tilley of the Office of Associate Chief Counsel (Energy, Credits, and Excise Tax). For further information regarding this notice, contact Mr. Tilley on (202) 317-6512 (not a toll-free number).

1 https://data.bls.gov/cgi-bin/srgate. The BLS publishes indexes and not actual or average prices.

SUMMARY: This notice of determinations modifies the list of taxable substances to include the following two substances: chloro-isobutene-isoprene rubber ((C4H8)n-(C5H7.31Cl0.69)m; n=97.75, m=2.25) and ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n -(C10H12)o; m=73.18, n=26.53, o=0.29).

EFFECTIVE DATES: The effective date for purposes of the tax under section 4671 of the Internal Revenue Code (Code) for the taxable substances added to the list is October 1, 2026. The effective date for purposes of refund claims under section 4662(e) of the Code for the taxable substances added to the list is April 1, 2023.

FOR FURTHER INFORMATION CONTACT: Julia Barlow at (202) 317-6855 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

Section 4671(a) of the Code imposes an excise tax on the sale or use of a taxable substance by the importer thereof (section 4671 tax). Section 4672(a)(1) of the Code defines the term taxable substance as any substance which, at the time of sale or use by the importer, is listed as a taxable substance by the Secretary of the Treasury or the Secretary’s delegate (Secretary) on the list of taxable substances under section 4672(a) (List).

Under section 4672(a)(2), an importer or exporter of any substance may request that the Secretary determine whether such substance should be added to the List as a taxable substance or should be removed from the List. Under section 4672(a)(2)(B) and (a)(4) and (b)(2), the Secretary is required to add a substance to the List if the Secretary determines that any taxable chemicals that are listed in section 4661(b) of the Code constitute more than 20 percent of the weight, or more than 20 percent of the value, of the materials used to produce such substance, which determination is required under section 4672(a)(2)(B) and (a)(4) to be made based on the predominant method of production (weight or value test). Section 4672(a)(4) authorizes the Secretary to remove a substance from the List only if such substance meets neither the weight nor the value test of section 4672(a)(2)(B).

Section 4672(a)(3) includes an initial list of taxable substances. Section 4 of Notice 2021-66 (2021-52 I.R.B. 901) provides the list of 101 substances that the Secretary added to the List before November 15, 2021. On May 31, 2024, the Secretary published a Notice of Determination in the Federal Register (89 FR 47238) adding polyoxymethylene to the List; this Notice of Determination was also published in the Internal Revenue Bulletin as Notice 2024-50 (2024-26 I.R.B. 1789). On August 4, 2025, the Secretary published a Notice of Determinations in the Federal Register (90 FR 36520) adding 21 substances to the List; this Notice of Determinations was also published in the Internal Revenue Bulletin as Notice 2025-41 (2025-34 I.R.B. 325). On September 17, 2025, the Secretary published a Notice of Determinations in the Federal Register (90 FR 44881) adding 39 substances to the List; this Notice of Determinations was also published in the Internal Revenue Bulletin as Notice 2025-51 (2025-41 I.R.B. 448). Rev. Proc. 2022-26 (2022-29 I.R.B. 90), as modified by Rev. Proc. 2023-20 (2023-15 I.R.B. 636), provides the exclusive procedures by which an importer, exporter, or interested person may request a determination that a particular substance be added to or removed from the List.

Section 4671(b)(3) authorizes the Secretary to prescribe a tax rate for taxable substances in lieu of the tax rate specified in section 4671(b)(2). The tax rate prescribed by the Secretary for a substance added to the List is calculated by multiplying the conversion factor for each taxable chemical used in the production of the substance by the corresponding tax rate for that taxable chemical under section 4661(b), and adding those results together. Conversion factors are determined based on the predominant method of production of the substance. See sections 8 and 10.04(8) of Rev. Proc. 2022-26. Importers are not required to use the prescribed tax rate for a taxable substance and may calculate their own rate under section 4671(b)(1).

Pursuant to Section 4672(a)(4), this notice of determinations modifies the List to include the two additional taxable substances listed in the Summary of Determinations section of this notice, as explained in the Requests to Add Substances to the List and General Explanation of Determinations sections of this notice. The determination for each specific substance added to the List is explained in parts 1 and 2 of the Modifications to the List of Taxable Substances section of this notice.

The updated List and prescribed tax rates for taxable substances will be included in the instructions to Form 6627, Environmental Taxes.

On June 26, 2026, the Secretary determined to add the following substances to the List:

1. Chloro-isobutene-isoprene rubber ((C4H8)n-(C5H7.31Cl0.69)m; n=97.75, m=2.25)

2. Ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n-(C10H12)o; m=73.18, n=26.53, o=0.29)

For each of the substances listed in the Summary of Determinations section of this notice, an importer or an exporter submitted a petition to the IRS in accordance with Rev. Proc. 2022-26 requesting a determination under section 4672(a)(2) to add the substance to the List. For each substance, the petition represented that taxable chemicals constitute more than 20 percent of the weight of materials used to produce the substance, based on the predominant method of production.

After reviewing the petitions for each of the substances listed in the Summary of Determinations section of this notice, the Secretary determined that taxable chemicals constitute more than 20 percent by weight of the materials used to produce the substance, based on the predominant method of production. Therefore, both of the substances are added to the List as required under section 4672(a)(2) and (4). The Secretary made the determinations to add these substances to the List in accordance with the requirements of section 4672(a)(2) and (4), and pursuant to the procedures set forth in Rev. Proc. 2022-26, as modified by Rev. Proc. 2023-20.

The relevant information for each taxable substance is provided in the specific determinations included in parts 1 and 2 of the Modifications to the List of Taxable Substances section of this notice. The tax rate for each taxable substance, as prescribed by the Secretary, is provided in paragraph (a)(6) of each specific determination. All scientific information provided in the specific determinations reflects the information provided by petitioners as published in each taxable substance’s respective Notice of Filing.

Classification numbers proposed by each petitioner are included in paragraph (b) of each part, after each specific determination. The classification numbers provided with respect to a taxable substance are not part of the determination of whether it is added to the List and do not impact whether such substance is a taxable substance. Taxpayers may not rely on classification numbers for any purpose under sections 4661, 4662, 4671, and 4672, including (but not limited to) identification of a substance as a taxable substance on the List. Classification numbers may change over time. The Department of the Treasury (Treasury Department) and the IRS do not anticipate updating this document to reflect any such changes.

For purposes of the section 4671 tax, all the modifications in parts 1 and 2 of the Modifications to the List of Taxable Substances section of this notice are effective on and after October 1, 2026. For purposes of refund claims under section 4662(e), the modifications are effective April 1, 2023.

1. Determination to Add Chloro-isobutene-isoprene Rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25) to the List

Arlanxeo USA LLC and Arlanxeo Canada Inc., importers and exporters of chloro-isobutene-isoprene rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25), submitted a petition in accordance with Rev. Proc. 2022-26 requesting to add chloro-isobutene-isoprene rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25) to the List. According to the petition, the taxable chemicals butylene, chlorine, and sodium hydroxide constitute 97.36 percent by weight of the materials used to produce this substance, based on the predominant method of production.

(a) Determination. Chloro-isobutene-isoprene rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25) is added to the list of taxable substances under section 4672(a). Other pertinent information is as follows:

(1) Predominant method of production: The predominant method of producing chloro-isobutene-isoprene rubber involves reacting a hexane solution of butyl rubber with elemental chlorine. Butyl rubber is produced via the cationic copolymerization of butylene with isoprene in the presence of a Friedel-Crafts catalyst at low temperature, around -100°C.

(2) Stoichiometric material consumption equation:

n C4H8 (butylene) + m C5H8 (isoprene) + (0.69m) Cl2 (chlorine) + (0.69m) NaOH (sodium hydroxide) → (C4H8)n (C5H7.31Cl0.69)m (chloro-isobutene-isoprene rubber) + (0.69m) NaCl + (0.69m) H2O

(3) Reasons for the determination: The chloro-isobutene-isoprene rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25) petition was filed on July 13, 2025. The notice of filing summarizing the petition and requesting comments was published in the Federal Register (90 FR 39468) on August 15, 2025. The Treasury Department and the IRS received no substantive written comments in response to the notice of filing. A public hearing was neither requested nor held.

The Secretary followed the process in section 4672(a)(2)(B) in making this determination. A review of the stoichiometric material consumption equation and other information in the petition shows that the taxable chemicals butylene, chlorine, and sodium hydroxide constitute more than 20 percent by weight of the materials used in the production of chloro-isobutene-isoprene rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25), based on the predominant method of production. Therefore, the test in section 4672(a)(2)(B) is satisfied.

(4) Date of determination: June 26, 2026.

(5) Effective dates for addition of chloro-isobutene-isoprene rubber ((C4H8)n -(C5H7.31Cl0.69)m; n=97.75, m=2.25) to the List:

(i) Effective date for purposes of the section 4671 tax (see section 11.01 of Rev. Proc. 2022-26): October 1, 2026.

(ii) Effective date for purposes of refund claims under section 4662(e) (see sections 11.02 and 11.03 of Rev. Proc. 2022-26, as modified by section 3 of Rev. Proc. 2023-20): April 1, 2023.

(6) Tax rate prescribed by the Secretary: $9.46 per ton. The conversion factors for the taxable chemicals used in the production of chloro-isobutene-isoprene rubber ((C4H8)n-(C5H7.31Cl0.69)m; n=97.75, m=2.25) are 0.96 for butylene, 0.02 for chlorine, and 0.01 for sodium hydroxide. The tax rate is calculated by adding the products of the conversion factor for each taxable chemical by the tax rate for that taxable chemical: ((0.96 x $9.74) + (0.02 x $5.40) + (0.01 x $0.56) = $9.46).

(b) Classification numbers.

(1) The Secretary has no basis to object to the following proposed classification numbers:

(i) HTSUS number: 4002.39.0000.

(ii) Schedule B number: 4002.39.0000.

(iii) CAS number: 68081-82-3.

(2) The Secretary is unable to confirm the following proposed classification numbers: Not applicable.

2. Determination to Add Ethylene-propylene-dicyclopentadiene Rubber ((C2H4)m-(C3H6)n-(C10H12)o; m=73.18, n=26.53, o=0.29) to the List

Arlanxeo USA LLC and Arlanxeo Canada Inc., importers and exporters of ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n-(C10H12)o; m=73.18, n=26.53, o=0.29), submitted a petition in accordance with Rev. Proc. 2022-26 requesting to add ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n -(C10H12)o; m=73.18, n=26.53, o=0.29) to the List. According to the petition, the taxable chemicals ethylene and propylene constitute 98.80 percent by weight of the materials used to produce this substance, based on the predominant method of production.

(a) Determination. Ethylene-propylene-dicyclopentadiene rubber ((C2H4)m -(C3H6)n-(C10H12)o; m=73.18, n=26.53, o=0.29) is added to the list of taxable substances under section 4672(a). Other pertinent information is as follows:

(1) Predominant method of production: The predominant method of producing ethylene-propylene-dicyclopentadiene rubber is through the catalytic polymerization of ethylene, propylene, and non-conjugated diene monomers in a solution using various catalysts. Non-conjugated diene monomers include ethylidene norbornene and dicyclopentadiene. The non-conjugated diene monomers are produced from cyclopentadiene and butadiene, and cyclopentadiene, respectively.

(2) Stoichiometric material consumption equation:

m C2H4 (ethylene) + n C3H6 (propylene) + o [2 C5H6 (cyclopentadiene)] → (C2H4)m (C3H6)n(C10H12)o (ethylene-propylene-dicyclopentadiene rubber)

(3) Reasons for the determination: The ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n-(C10H12)o; m=73.18, n=26.53, o=0.29) petition was filed on July 13, 2025. The notice of filing summarizing the petition and requesting comments was published in the Federal Register (90 FR 39469) on August 15, 2025. The Treasury Department and the IRS received no written comments in response to the notice of filing. A public hearing was neither requested nor held.

The Secretary followed the process in section 4672(a)(2)(B) in making this determination. A review of the stoichiometric material consumption equation and other information in the petition shows that the taxable chemicals ethylene and propylene constitute more than 20 percent by weight of the materials used in the production of ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n -(C10H12)o; m=73.18, n=26.53, o=0.29), based on the predominant method of production. Therefore, the test in section 4672(a)(2)(B) is satisfied.

(4) Date of determination: June 26, 2026.

(5) Effective dates for addition of ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n-(C10H12)o; m=73.18, n=26.53, o=0.29) to the List:

(i) Effective date for purposes of the section 4671 tax (see section 11.01 of Rev. Proc. 2022-26): October 1, 2026.

(ii) Effective date for purposes of refund claims under section 4662(e) (see sections 11.02 and 11.03 of Rev. Proc. 2022-26, as modified by section 3 of Rev. Proc. 2023-20): April 1, 2023.

(6) Tax rate prescribed by the Secretary: $9.64 per ton. The conversion factors for the taxable chemicals used in the production of ethylene-propylene-dicyclopentadiene rubber ((C2H4)m-(C3H6)n -(C10H12)o; m=73.18, n=26.53, o=0.29) are 0.64 for ethylene and 0.35 for propylene. The tax rate is calculated by adding the products of the conversion factor for each taxable chemical by the tax rate for that taxable chemical: ((0.64 x $9.74) + (0.35 x $9.74) = $9.64).

(b) Classification numbers.

(1) The Secretary has no basis to object to the following proposed classification numbers:

(i) HTSUS number: 4002.70.0000.

(ii) Schedule B number: 4002.70.0000.

(iii) CAS number: 25038-36-2.

(2) The Secretary is unable to confirm the following proposed classification numbers: Not applicable.

Krishna P. Vallabhaneni, Tax Legislative Counsel.

This revenue procedure provides a transfer tax safe harbor for certain individual donors who make one or more contributions to Trump accounts established under section 530A of the Internal Revenue Code (Code).1 In the interest of sound tax administration, for taxpayers within the scope of section 4 of this revenue procedure, contributions to Trump accounts will be treated as completed gifts that are not gifts of future interests in property and to which the annual per-donee gift tax exclusion applies. As a result, taxpayers within the scope of section 4 of this revenue procedure will not be required to file gift tax returns reporting such contributions.

01. Trump accounts.

Section 70204 of Public Law 119-21, 139 Stat. 72 (July 4, 2025), commonly known as the One, Big, Beautiful Bill Act, added section 530A and related provisions concerning Trump accounts to the Code. A Trump account is a type of traditional individual retirement account (IRA) that is established under section 530A for the exclusive benefit of an eligible individual or the eligible individual’s beneficiaries and is designated as a Trump account at its establishment. An eligible individual is any individual (i) who has not attained age 18 before the close of the calendar year in which an election to open an initial Trump account (initial Trump account election) is made, (ii) for whom a social security number has been issued before the date of the initial Trump account election, and (iii) for whom the initial Trump account election is made. The eligible individual is the owner of the Trump account and is referred to as the account beneficiary.

A Trump account is subject to certain special rules that do not apply to other individual retirement arrangements under section 408, most of which apply only during the period ending before January 1 of the calendar year in which the account beneficiary attains age 18. This period is referred to as the growth period. The special rules that apply only during the growth period include a restriction on distributions to the account beneficiary. Specifically, during the growth period, no distributions may be made from a Trump account, except for qualified rollover contributions, a qualified ABLE rollover contribution (made only during the calendar year in which an account beneficiary attains age 17), distributions of excess contributions, and distributions upon the death of the account beneficiary. Consequently, the account beneficiary of a Trump account generally does not have access to amounts in the Trump account during the growth period.

Trump accounts may receive contributions from nonprofits, governments, employers, and individuals. During the growth period, a Trump account is subject to an annual contribution limit of $5,000, adjusted for inflation after 2027. This annual limit does not apply to the $1,000 Trump account pilot program contribution, qualified general contributions (which are funded by nonprofits and certain governmental entities), or qualified rollover contributions, but does apply to any other contribution (including contributions from employers).

As of June 4, 2026, nearly six million elections to open a Trump account have been received.

.02 Relevant transfer tax rules.

Individuals and their estates generally are subject to gift, estate, or generation-skipping transfer (GST) tax liability once the value of cumulative transfers during life and at death exceed the lifetime basic exclusion amount, which is currently $15 million (adjusted annually for inflation). Sections 2010(c), 2505(a), 2631(c).2

The gift tax applies to a transfer of property by way of gift, whether the transfer is in trust or otherwise, whether the gift is direct or indirect, and whether the property is real or personal, tangible or intangible. Section 2511(a). The term “taxable gifts” is defined as the total amount of gifts made during the calendar year, less any available deductions (e.g., gift tax marital or charitable deductions). Section 2503(a). However, there is an annual per-donee gift tax exclusion from the total amount of the donor’s gifts during a calendar year. Specifically, each donor may exclude from the amount of the donor’s gifts those made to a particular recipient to the extent the total value of the donor’s gifts to that recipient does not exceed this annual exclusion amount, provided that those gifts are not gifts of a future interest in property. Section 2503(b)(1). For calendar year 2026, the annual exclusion amount (as indexed for inflation) is $19,000 per individual recipient, and is available in addition to the donor’s lifetime basic exclusion amount (the cumulative amount excluded from gift and estate taxes).

A taxable gift or transfer at death also may be subject to GST tax. Section 2601. Every individual is allowed a lifetime GST exemption amount, which is equal to the basic exclusion amount for gift and estate tax purposes (thus, $15,000,000 for calendar year 2026). Section 2631(c).

Gifts are also subject to certain reporting requirements. An individual making one or more gifts generally is required by section 6019 (and by section 2662 if the gift also is a direct skip for GST tax purposes) to file a gift tax return to report gifts made during the calendar year. The gift tax return must be filed on or before the date specified in section 6075(b), generally April 15 of the following calendar year. If the donor’s total gifts to each recipient (other than gifts of future interests in property) during the calendar year are valued at or below the annual per-donee gift tax exclusion amount, those gifts do not require the filing of a gift tax return. However, gifts of future interests in property are required to be reported on a gift tax return because they are not eligible for the annual per-donee gift tax exclusion. In FY 2025, the Internal Revenue Service (IRS) received approximately 300,000 gift tax returns (Form 709).3

The Department of the Treasury (Treasury Department) and the IRS have received stakeholder comments and are aware of public commentary raising questions about the transfer tax consequences for individual donors who make contributions to Trump accounts, including whether such contributions constitute taxable gifts that must be reported on a gift tax return. Such reporting would be required if contributions to Trump accounts are treated as gifts of future interests.

The Treasury Department and the IRS understand the concerns raised in public comments and recognize that the vast majority of individual donors to Trump accounts are unlikely to ever owe federal gift, estate or GST tax due to the lifetime basic exclusion amount of $15,000,000 and the corresponding $15,000,000 GST exemption amount. For many of these donors, the cost and other burdens of complying with gift tax reporting requirements could outweigh the anticipated financial savings benefit of making one or more contributions to a Trump account. In addition, gift tax reporting compliance by these donors could dramatically increase the burden on the IRS to process gift tax returns for individual donors who are unlikely to ever be subject to gift, estate, or GST tax. Given the fact that nearly 6,000,000 elections to open Trump accounts have already been received, the number of gift tax returns filed annually could be expected to increase from roughly 300,000 to several million. Accordingly, the Treasury Department and the IRS are providing a safe harbor, described in section 5 of this revenue procedure, for taxpayers within the scope of section 4 of this revenue procedure.

.01 In general. The safe harbor described in section 5 of this revenue procedure applies for a particular calendar year only if all of the requirements of section 4.02 of this revenue procedure are met.

.02 Requirements.

(1) Taxpayer is an individual;

(2) The only taxable gifts made by the taxpayer during the calendar year are cash contributions (in the form of cash, check, money order, or electronic funds transfer) to one or more Trump accounts, each made before the calendar year in which the account beneficiary attains age 18;

(3) The taxpayer’s total gifts during the calendar year to each individual who is an account beneficiary, including contributions to that account beneficiary’s Trump account, do not exceed the annual exclusion amount under section 2503(b) ($19,000 for 2026);

(4) Such contributions to Trump accounts made during the calendar year do not generate for that calendar year either a gift or GST tax liability, after application of the taxpayer’s remaining applicable credit amount4 against the gift tax, or remaining GST exemption; and

(5) Disregarding the Trump account contributions described in section 4.02(2) of this revenue procedure, no gift tax return is required to be filed, and no gift tax return is otherwise filed, for that calendar year by or on behalf of the taxpayer, whether for GST tax, portability, or other purposes.5

If each of the requirements specified in section 4.02 of this revenue procedure is met for a calendar year in which a taxpayer makes contributions to one or more Trump accounts, each Trump account contribution made by the taxpayer during that calendar year will be treated as a completed gift to the account beneficiary that is not a future interest in property and to which the annual exclusion applies for purposes of gift tax, GST tax and gift tax reporting. As a result, taxpayers within the scope of section 4 of this revenue procedure will not be required to file a gift tax return reporting such contributions.

In calendar year 2026 individual donor (Taxpayer) contributes $5,000 cash to each of three Trump accounts established for account beneficiaries A, B, and C, and makes an additional gift to C of $13,000 cash. Taxpayer makes no other gifts during the calendar year and is not required to, and does not, file a gift tax return for the calendar year for any other purpose. The $15,000 in contributions to Trump accounts do not generate a gift or GST tax liability, after taking into consideration the Taxpayer’s remaining lifetime applicable exclusion amount or remaining GST exemption. Under these facts, the requirements of section 4.02 of this revenue procedure are met and Taxpayer’s 2026 Trump account contributions will be treated as completed gifts to A, B, and C that are not future interests in property. If instead Taxpayer’s cash gift to C in 2026 is $14,500, the requirement in section 4.02(3) of this revenue procedure is not met because Taxpayer’s total gifts to C during calendar year 2026 exceed the annual per-donee gift tax exclusion under section 2503(b) of $19,000. Accordingly, Taxpayer must file a gift tax return for calendar year 2026 reporting all 2026 gifts, and must report the Trump account contributions to A, B, and C as gifts of future interests.

The Paperwork Reduction Act of 1995 (44 U.S.C. 3501-3520) (PRA) generally requires that a Federal agency obtain the approval of the Office of Management and Budget (OMB) before collecting information from the public, whether such collection of information is mandatory, voluntary, or required to obtain or retain a benefit. An agency may not conduct or sponsor, and a person is not required to respond to, a collection of information unless it displays a valid control number assigned by the OMB.

Section 4 of this revenue procedure sets forth safe harbor requirements that taxpayers may follow for Trump account contributions to be treated as gifts to which the gift tax annual exclusion under IRC section 2503(b) applies for purposes of gift tax, GST tax, and gift tax reporting. Taxpayers should maintain records sufficient to substantiate compliance with the safe harbor rules. These recordkeeping requirements are considered general tax records under §1.6001-1(e). For PRA purposes, general tax records are already approved by OMB under 1545-0074 for individual filers. The revenue procedure does not impose any additional burden for taxpayers for purposes of PRA.

The principal author of this revenue procedure is Rachel K. Downs of the Office of Associate Chief Counsel (Passthroughs, Trusts, and Estates). For further information regarding this revenue procedure, please contact Rachel K. Downs at (202) 317-6859 (not a toll-free call).

26 C.F.R. 20.2010-1: Unified credit against estate tax; in general.

This revenue procedure provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) meet certain requirements. If the requirements are met, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax annual exclusion applies under § 2503(b). As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions. See Rev. Proc. 2026-25, page 45.

26 C.F.R. 25.2503-2: Exclusions from gifts.

This revenue procedure provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) meet certain requirements. If the requirements are met, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax annual exclusion applies under § 2503(b). As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions. See Rev. Proc. 2026-25, page 45.

26 C.F.R. 25.2505-1: Unified credit against gift tax; in general.

This revenue procedure provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) meet certain requirements. If the requirements are met, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax annual exclusion applies under § 2503(b). As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions. See Rev. Proc. 2026-25, page 45.

26 C.F.R. 26.2642-1(c)(3): Nontaxable gifts.

This revenue procedure provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) meet certain requirements. If the requirements are met, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax annual exclusion applies under § 2503(b). As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions. See Rev. Proc. 2026-25, page 45.

26 C.F.R. 26.2662-1: Generation-skipping transfer tax return requirements.

This revenue procedure provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) meet certain requirements. If the requirements are met, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax annual exclusion applies under § 2503(b). As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions. See Rev. Proc. 2026-25, page 45.

26 C.F.R. 25.6019-1: Persons required to file returns.

This revenue procedure provides a safe harbor for individual taxpayers who (i) make contributions to Trump accounts established under § 530A of the Internal Revenue Code and (ii) meet certain requirements. If the requirements are met, contributions to Trump accounts will be treated as completed gifts that are not future interests in property and to which the annual per-donee gift tax annual exclusion applies under § 2503(b). As a result, taxpayers within the scope of the revenue procedure will not be required to file gift tax returns reporting such contributions. See Rev. Proc. 2026-25, page 45.

1 Unless otherwise specified, all “section” references are to sections of the Code.

2 In general terms, if a portability election under section 2010(c)(5) is made by the estate of a predeceasing spouse, the predeceasing spouse’s unused exclusion amount (deceased spousal unused exclusion or DSUE) is added to the surviving spouse’s basic exclusion amount to increase the value of the surviving spouse’s cumulative transfers exempt from gift and estate tax. The sum of the basic exclusion amount and any available DSUE amount is the applicable exclusion amount. Section 2010(c)(3).

3 2025-I.R.S. Data Book at 4 tbl. 1-2 (2026). See IRS Data Book, Table 1-2, available here: Returns filed, taxes collected and refunds issued | Internal Revenue Service.

4 The applicable credit amount effectively exempts from federal estate and gift tax an individual’s taxable transfers with a cumulative value not exceeding the applicable exclusion amount. See section 2010(c).

5 For example, a gift tax return may be required to make affirmative allocations of GST exemption, such as a late allocation of GST exemption to a prior transfer or an allocation at the close of an estate tax inclusion period (as defined in section 2642(f)(3)), or to make certain GST elections. In addition, a gift tax return may be required as the result of an examination of the estate tax return.

This announcement informs taxpayers that the Internal Revenue Service is modifying Notice 2026-10, 2026-4 I.R.B. 378, by revising the optional standard mileage rates for computing the deductible costs of operating an automobile for business, medical, or moving expense purposes and for determining the reimbursed amount of these expenses that is deemed substantiated. This modification results from recent increases in the price of fuel.

The revised standard mileage rates are:

(1) Business 76 cents per mile

(2) Medical and moving 23.5 cents per mile

The mileage rate that applies to the deduction for charitable contributions is fixed under § 170(i) of the Internal Revenue Code at 14 cents per mile.

The revised standard mileage rates set forth in this announcement apply to deductible transportation expenses paid or incurred for business, medical, or moving expense purposes on or after July 1, 2026, and to mileage allowances that are paid both (1) to an employee on or after July 1, 2026, and (2) for transportation expenses paid or incurred by the employee on or after July 1, 2026.

The standard mileage rates set forth in Notice 2026-10 continue to apply to deductible transportation expenses paid or incurred for business, medical, or moving expense purposes before July 1, 2026, and to mileage allowances paid (1) to an employee before July 1, 2026, or (2) with respect to transportation expenses paid or incurred by the employee before July 1, 2026.

All other provisions of Notice 2026-10 remain in effect.

Table of Contents

The Internal Revenue Service has revoked its determination that the organizations listed below qualify as organizations described in sections 501(c)(3) and 170(c)(2) of the Internal Revenue Code of 1986.

Generally, the IRS will not disallow deductions for contributions made to a listed organization on or before the date of announcement in the Internal Revenue Bulletin that an organization no longer qualifies. However, the IRS is not precluded from disallowing a deduction for any contributions made after an organization ceases to qualify under section 170(c)(2) if the organization has not timely filed a suit for declaratory judgment under section 7428 and if the contributor (1) had knowledge of the revocation of the ruling or determination letter, (2) was aware that such revocation was imminent, or (3) was in part responsible for or was aware of the activities or omissions of the organization that brought about this revocation.

If on the other hand a suit for declaratory judgment has been timely filed, contributions from individuals and organizations described in section 170(c)(2) that are otherwise allowable will continue to be deductible. Protection under section 7428(c) would begin on June 24, 2026, and would end on the date the court first determines the organization is not described in section 170(c)(2) as more particularly set for in section 7428(c)(1). For individual contributors, the maximum deduction protected is $1,000, with a husband and wife treated as one contributor. This benefit is not extended to any individual, in whole or in part, for the acts or omissions of the organization that were the basis for revocation.

| Name Of Organization | Effective Date of Revocation | Location |

|---|---|---|

| Preserve Silver Lake Fund | 08/01/2022 | Lewisberry, PA |

| Community School of New Hope | 01/01/2022 | New Hope, PA |

| ACTS Community Development Corporation | 01/01/2022 | Brooklyn, NY |

| Treasure County Senior Citizens | 07/01/2022 | Hysham, MT |

Revenue rulings and revenue procedures (hereinafter referred to as “rulings”) that have an effect on previous rulings use the following defined terms to describe the effect:

Amplified describes a situation where no change is being made in a prior published position, but the prior position is being extended to apply to a variation of the fact situation set forth therein. Thus, if an earlier ruling held that a principle applied to A, and the new ruling holds that the same principle also applies to B, the earlier ruling is amplified. (Compare with modified, below).

Clarified is used in those instances where the language in a prior ruling is being made clear because the language has caused, or may cause, some confusion. It is not used where a position in a prior ruling is being changed.

Distinguished describes a situation where a ruling mentions a previously published ruling and points out an essential difference between them.

Modified is used where the substance of a previously published position is being changed. Thus, if a prior ruling held that a principle applied to A but not to B, and the new ruling holds that it applies to both A and B, the prior ruling is modified because it corrects a published position. (Compare with amplified and clarified, above).

Obsoleted describes a previously published ruling that is not considered determinative with respect to future transactions. This term is most commonly used in a ruling that lists previously published rulings that are obsoleted because of changes in laws or regulations. A ruling may also be obsoleted because the substance has been included in regulations subsequently adopted.

Revoked describes situations where the position in the previously published ruling is not correct and the correct position is being stated in a new ruling.

Superseded describes a situation where the new ruling does nothing more than restate the substance and situation of a previously published ruling (or rulings). Thus, the term is used to republish under the 1986 Code and regulations the same position published under the 1939 Code and regulations. The term is also used when it is desired to republish in a single ruling a series of situations, names, etc., that were previously published over a period of time in separate rulings. If the new ruling does more than restate the substance of a prior ruling, a combination of terms is used. For example, modified and superseded describes a situation where the substance of a previously published ruling is being changed in part and is continued without change in part and it is desired to restate the valid portion of the previously published ruling in a new ruling that is self contained. In this case, the previously published ruling is first modified and then, as modified, is superseded.

Supplemented is used in situations in which a list, such as a list of the names of countries, is published in a ruling and that list is expanded by adding further names in subsequent rulings. After the original ruling has been supplemented several times, a new ruling may be published that includes the list in the original ruling and the additions, and supersedes all prior rulings in the series.

Suspended is used in rare situations to show that the previous published rulings will not be applied pending some future action such as the issuance of new or amended regulations, the outcome of cases in litigation, or the outcome of a Service study.

The following abbreviations in current use and formerly used will appear in material published in the Bulletin.

A—Individual.

Acq.—Acquiescence.

B—Individual.

BE—Beneficiary.

BK—Bank.

B.T.A.—Board of Tax Appeals.

C—Individual.

C.B.—Cumulative Bulletin.

CFR—Code of Federal Regulations.

CI—City.

COOP—Cooperative.

Ct.D.—Court Decision.

CY—County.

D—Decedent.

DC—Dummy Corporation.

DE—Donee.

Del. Order—Delegation Order.

DISC—Domestic International Sales Corporation.

DR—Donor.

E—Estate.

EE—Employee.

E.O.—Executive Order.

ER—Employer.

ERISA—Employee Retirement Income Security Act.

EX—Executor.

F—Fiduciary.

FC—Foreign Country.

FICA—Federal Insurance Contributions Act.

FISC—Foreign International Sales Company.

FPH—Foreign Personal Holding Company.

F.R.—Federal Register.

FUTA—Federal Unemployment Tax Act.

FX—Foreign corporation.

G.C.M.—Chief Counsel’s Memorandum.

GE—Grantee.

GP—General Partner.

GR—Grantor.

IC—Insurance Company.

I.R.B.—Internal Revenue Bulletin.

LE—Lessee.

LP—Limited Partner.

LR—Lessor.

M—Minor.

Nonacq.—Nonacquiescence.

O—Organization.

P—Parent Corporation.

PHC—Personal Holding Company.

PO—Possession of the U.S.

PR—Partner.

PRS—Partnership.

PTE—Prohibited Transaction Exemption.

Pub. L.—Public Law.

REIT—Real Estate Investment Trust.

Rev. Proc.—Revenue Procedure.

Rev. Rul.—Revenue Ruling.

S—Subsidiary.

S.P.R.—Statement of Procedural Rules.

Stat.—Statutes at Large.

T—Target Corporation.

T.C.—Tax Court.

T.D.—Treasury Decision.

TFE—Transferee.

TFR—Transferor.

T.I.R.—Technical Information Release.

TP—Taxpayer.

TR—Trust.

TT—Trustee.

U.S.C.—United States Code.

X—Corporation.

Y—Corporation.

Z—Corporation.

The Introduction at the beginning of this issue describes the purpose and content of this publication. The weekly Internal Revenue Bulletins are available at www.irs.gov/irb/.

If you have comments concerning the format or production of the Internal Revenue Bulletin or suggestions for improving it, we would be pleased to hear from you. You can email us your suggestions or comments through the IRS Internet Home Page www.irs.gov) or write to the

Internal Revenue Service, Publishing Division, IRB Publishing Program Desk, 1111 Constitution Ave. NW, IR-6230 Washington, DC 20224.