)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

- HIGHLIGHTS OF THIS ISSUE

- Part III

- Reference Price for Section 45I Credit for Production of Natural Gas from Marginal Wells During Taxable Years Beginning in Calendar Year 2019

- Notice Proposing Revenue Procedure Updating Group Exemption Letter Program

- Definition of Terms

- Numerical Finding List

- Finding List of Current Actions on Previously Published Items1

- How to get the Internal Revenue Bulletin

Internal Revenue Bulletin: 2020-21

May 18, 2020

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

This procedure modifies Rev. Proc. 2020-1 temporarily to allow for the electronic submission of requests for letter rulings, closing agreements, determination letters, and information letters issued by the Associate Chief Counsel (Corporate), Associate Chief Counsel (Financial Institutions and Products), Associate Chief Counsel (Income Tax and Accounting), Associate Chief Counsel (International), Associate Chief Counsel (Passthroughs and Special Industries), Associate Chief Counsel (Procedure and Administration), and Associate Chief Counsel (Employee Benefits, Exempt Organizations, and Employment Taxes). This procedure also contains revised procedures for determination letters issued by the IRS Large Business and International Division.

26 CFR 601.201: Rulings and determination letters

This notice contains a proposed revenue procedure that sets forth updated procedures under which recognition of exemption from federal income tax for organizations described in § 501(c) of the Internal Revenue Code may be obtained on a group basis for subordinate organizations affiliated with and under the general supervision or control of a central organization.

This notice provides guidance regarding the nondeductibility of costs that are the subject of loan forgiveness under section 1106 of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Public Law 116-136, 134 Stat. 281 (March 27, 2020).

This notice provides the applicable reference price for qualified natural gas production from qualified marginal wells during taxable years beginning in calendar year 2019 for the purpose of determining the marginal well production credit under §45I. The applicable reference price for taxable years beginning in calendar year 2019 is $2.55 per 1,000 cubic feet. The notice also provides the credit amount used for the purpose of determining the marginal well production credit. The credit amount for taxable years beginning in calendar year 2019 is $0.08 per 1,000 cubic feet.

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

This notice provides guidance regarding the deductibility for Federal income tax purposes of certain otherwise deductible expenses incurred in a taxpayer’s trade or business when the taxpayer receives a loan (covered loan) pursuant to the Paycheck Protection Program under section 7(a)(36) of the Small Business Act (15 U.S.C. 636(a)(36)). Specifically, this notice clarifies that no deduction is allowed under the Internal Revenue Code (Code) for an expense that is otherwise deductible if the payment of the expense results in forgiveness of a covered loan pursuant to section 1106(b) of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Public Law 116-136, 134 Stat. 281, 286-93 (March 27, 2020) and the income associated with the forgiveness is excluded from gross income for purposes of the Code pursuant to section 1106(i) of the CARES Act.

The Paycheck Protection Program was established by section 1102 of the CARES Act. Under the Paycheck Protection Program, a recipient of a covered loan may use the proceeds to pay (1) payroll costs, (2) certain employee benefits relating to healthcare, (3) interest on mortgage obligations, (4) rent, (5) utilities, and (6) interest on any other existing debt obligations. See section 7(a)(36)(F) of the Small Business Act (describing allowable uses of a covered loan). See also Q&A 2.r. in Part III of the interim final rule, Business Loan Program Temporary Changes; Paycheck Protection Program, Docket No. SBA-2020-0015, 85 Fed. Reg. 20811, 20814 (April 15, 2020).

Under section 1106(b) of the Cares Act, a recipient of a covered loan can receive forgiveness of indebtedness on the loan (covered loan forgiveness) in an amount equal to the sum of payments made for the following expenses during the 8-week “covered period” beginning on the covered loan’s origination date (each, an eligible section 1106 expense): (1) payroll costs, (2) any payment of interest on any covered mortgage obligation, (3) any payment on any covered rent obligation, and (4) any covered utility payment. See section 1106(a) (defining the terms “covered period”, “covered mortgage obligation,” “covered rent obligation,” “covered utility payment,” and “payroll costs”), (b) (regarding eligibility for covered loan forgiveness), and (g) (regarding covered loan forgiveness decisions). However, section 1106(d) of the CARES Act provides that the amount of the covered loan forgiveness is reduced if, during the covered period, (1) the average number of full-time equivalent employees of the recipient is reduced as compared to the number of full-time employees in a specified base period, or (2) the salary or wages of certain employees is reduced by more than 25 percent as compared to the last full quarter before the covered period. In addition, pursuant to an interim final rule issued by the Small Business Administration, no more than 25 percent of the amount forgiven can be attributable to non-payroll costs. See Q&A 2.o. in Part III of the interim final rule, Business Loan Program Temporary Changes; Paycheck Protection Program, Docket No. SBA-2020-0015, 85 Fed. Reg. 20811, 20813-20814 (April 15, 2020).

Section 1106(i) of the CARES Act addresses certain Federal income tax consequences resulting from covered loan forgiveness. Specifically, that subsection provides that, for purposes of the Code, any amount that (but for that subsection) would be includible in gross income of the recipient by reason of forgiveness described in section 1106(b) “shall be excluded from gross income.” Thus, section 1106(i) of the CARES Act operates to exclude from the gross income of a recipient any category of income that may arise from covered loan forgiveness, regardless of whether such income would be (1) properly characterized as income from the discharge of indebtedness under section 61(a)(11) of the Code, or (2) otherwise includible in gross income under section 61 of the Code.

Neither section 1106(i) of the CARES Act nor any other provision of the CARES Act addresses whether deductions otherwise allowable under the Code for payments of eligible section 1106 expenses by a recipient of a covered loan are allowed if the covered loan is subsequently forgiven under section 1106(b) of the CARES Act as a result of the payment of those expenses. This Notice addresses the effect of covered loan forgiveness on the deductibility of payments of eligible section 1106 expenses.

Section 161 of the Code provides that, in computing taxable income under section 63 of the Code, there shall be allowed as deductions the items specified in part VI, subchapter B, chapter 1 of the Code (for example, sections 162 and 163). However, section 161 of the Code provides that the allowance of these deductions is subject to the exceptions provided in part IX, subchapter B, chapter 1 of the Code. These exceptions include section 265 of the Code. See also section 261.

In general, section 162 of the Code provides for a deduction for all ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business. Covered rent obligations, covered utility payments, and payroll costs consisting of wages and benefits paid to employees comprise typical trade or business expenses for which a deduction under section 162 of the Code generally is appropriate. Section 163(a) of the Code provides a deduction for certain interest paid or accrued during the taxable year on indebtedness, including interest paid or incurred on a mortgage obligation of a trade or business.

However, section 265(a)(1) of the Code and §1.265-1 of the Income Tax Regulations provide that no deduction is allowed to a taxpayer for any amount otherwise allowable as a deduction to such taxpayer that is allocable to one or more classes of income other than interest (whether or not any amount of income of that class or classes is received or accrued) wholly exempt from the taxes imposed by subtitle A of the Code. See generally section 265(a)(1); §1.265-1. The term “class of exempt income” means any class of income (whether or not any amount of income of such class is received or accrued) that is either wholly excluded from gross income under any provision of subtitle A of the Code or wholly exempt from the taxes imposed by subtitle A of the Code under the provisions of any other law. See §1.265-1(b)(1). The purpose of section 265 of the Code is to prevent a double tax benefit.

Section 265(a)(1) of the Code applies to otherwise deductible expenses incurred for the purpose of earning or otherwise producing tax-exempt income. It also applies where tax exempt income is earmarked for a specific purpose and deductions are incurred in carrying out that purpose. In such event, it is proper to conclude that some or all of the deductions are allocable to the tax-exempt income. See Christian v. United States, 201 F. Supp. 155 (E.D. La. 1962) (school teacher was denied deductions for expenses incurred for a literary research trip to England because the expenses were allocable to a tax-exempt gift and fellowship grant); Banks v. Commissioner, 17 T.C. 1386 (1952) (certain educational expenses paid by the Veterans’ Administration that were exempt from income tax, were not deductible); Heffelfinger v. Commissioner, 5 T.C. 985 (1945), (Canadian income taxes on income exempt from U.S. tax are not deductible in computing U.S. taxable income); and Rev. Rul. 74-140, 1974-1 C.B. 50, (the portion of a state income tax paid by a taxpayer that is allocable to the cost-of-living allowance, a class of income wholly exempt under section 912, is nondeductible under section 265).

In Manocchio v. Commissioner, 78 T.C. 989 (1982), a taxpayer attended a flight-training course that maintained and improved skills required in the taxpayer’s trade or business. As a veteran, the taxpayer was entitled to an educational assistance allowance from the Veterans’ Administration pursuant to 38 U.S.C. section 1677 (1976) equal to 90 percent of the costs incurred. Because the payments received were exempt from taxation under 38 U.S.C. section 310(a) (1976), the taxpayer did not report them as income. The taxpayer did, however, deduct the entire cost of the flight training course, including the portion that had been reimbursed by the Veterans’ Administration. In a reviewed opinion, the court held that the reimbursed flight-training expenses were nondeductible under section 265(a)(1) of the Code.

NON-DEDUCTIBILITY OF PAYMENTS TO THE EXTENT INCOME RESULTING FROM LOAN FORGIVENESS IS EXCLUDED UNDER SECTION 1106(i) OF THE CARES ACT

To the extent that section 1106(i) of the CARES Act operates to exclude from gross income the amount of a covered loan forgiven under section 1106(b) of the CARES Act, the application of section 1106(i) results in a “class of exempt income” under §1.265-1(b)(1) of the Regulations. Accordingly, section 265(a)(1) of the Code disallows any otherwise allowable deduction under any provision of the Code, including sections 162 and 163, for the amount of any payment of an eligible section 1106 expense to the extent of the resulting covered loan forgiveness (up to the aggregate amount forgiven) because such payment is allocable to tax-exempt income. Consistent with the purpose of section 265, this treatment prevents a double tax benefit.

This conclusion is consistent with prior guidance of the IRS that addresses the application of section 265(a) to otherwise deductible payments. In particular, Rev. Rul. 83-3, 1983-1 C.B. 72, provides that, where tax exempt income is earmarked for a specific purpose, and deductions are incurred in carrying out that purpose, section 265(a) applies because such deductions are allocable to the tax-exempt income. In accordance with the analysis set forth in Rev. Rul. 83-3, the direct link between (1) the amount of tax exempt covered loan forgiveness that a recipient receives pursuant to section 1106 of the CARES Act, and (2) an equivalent amount of the otherwise deductible payments made by a recipient for eligible section 1106 expenses, constitutes a sufficient connection for section 265(a) to apply to disallow deductions for such payments under any provision of the Code, including sections 162 and 163, to the extent of the income excluded under section 1106(i) of the CARES Act.

The deductibility of payments of eligible section 1106 expenses that result in loan forgiveness under section 1106(b) of the CARES Act is also subject to disallowance under case law and published rulings that deny deductions for otherwise deductible payments for which the taxpayer receives reimbursement. See, e.g., Burnett v. Commissioner, 356 F.2d 755, 759-60 (5th Cir. 1966); Wolfers v. Commissioner, 69 T.C. 975 (1978); Charles Baloian Co. v. Commissioner, 68 T.C. 620 (1977); Rev. Rul. 80-348, 1980-2 C.B. 31; Rev. Rul. 80-173, 1980-2 C.B. 60.

The principal authors of this notice are Sarah Daya and Patrick Clinton of the Office of Associate Chief Counsel (Income Tax & Accounting). For further information regarding the application of sections 161, 162, 163, and 261 please contact Ms. Daya at (202) 317-4891 (not a toll-free call); for further information regarding the application of section 265, please contact Mr. Clinton at (202) 317-7005 (not a toll-free number).

This notice provides the applicable reference price for qualified natural gas production from qualified marginal wells during taxable years beginning in calendar year 2019 for the purpose of determining the marginal well production credit (MWC) under §45I of the Internal Revenue Code. The applicable reference price for taxable years beginning in calendar year 2019 is $2.55 per 1,000 cubic feet (Mcf).

This notice also provides the credit amount used for the purpose of determining the MWC for taxable years beginning in calendar year 2019. The credit amount is determined using the 2019 inflation adjustment factor of 1.3015 and the applicable reference price of $2.55 per Mcf. The credit amount for taxable years beginning in calendar year 2019 is $0.08 per Mcf.

Section 45I(a), as it relates to qualified natural gas production, provides that, for purposes of § 38, the MWC for any taxable year is an amount equal to the product of (1) the credit amount and (2) the qualified natural gas production that is attributable to the taxpayer.

Section 45I(c)(1) provides that “qualified natural gas production” means domestic natural gas produced from a qualified marginal well. Section 45I(c)(3)(A) provides that a qualified marginal well is a domestic well (i) the production from which during the taxable year is treated as marginal production under § 613A(c)(6), or (ii) which, during the taxable year (I) has average production of not more than 25 barrel-of-oil equivalents per day, and (II) produces water at a rate not less than 95 percent of total well effluent.

Section 613A(c)(6)(D) and (E) provide that “marginal production” means domestic natural gas produced during any taxable year from a property which is a stripper well property for the calendar year in which the taxable year begins. A “stripper well property” is, with respect to any calendar year, any property producing not more than 15 barrel equivalents per day, determined by dividing the average daily production of domestic crude oil and domestic natural gas from producing wells on the property for such calendar year by the number of such wells.

Section 45I(c)(2)(A) provides that generally only the first 1,095 barrels or barrel-of-oil equivalents (as defined in § 45K(d)(5)) produced during the taxable year qualify for the MWC. This limitation is proportionately reduced in the case of a short taxable year or in the case of a well that is not capable of production each day of a taxable year. See § 45I(c)(2)(B). The number of wells on which a taxpayer may claim the MWC is not limited.

Section 45I(d)(2) provides that to claim the credit a taxpayer must hold an operating interest in the qualified marginal well producing the natural gas to which the credit relates. Under § 45I(d)(1) if a well is owned by more than one owner and the natural gas production exceeds the limitation under § 45I(c)(2), the qualifying natural gas production attributable to the taxpayer is determined on the basis of the ratio which taxpayer’s revenue interest in the production bears to the aggregate of the revenue interests of all operating interest owners in the production. Finally, § 45I(d)(3) provides that the MWC is not allowable if the taxpayer is also eligible to claim the § 45K nonconventional sources credit for the taxable year, unless the taxpayer elects not to claim the credit under § 45K for the well.

For purposes of § 45I(a)(1), the credit amount is 50 cents (adjusted for inflation) per Mcf of qualified natural gas production (tentative credit amount). See § 45I(b)(1)(B) and (b)(2)(B).

Section 45I(b)(2)(A) and (B) provide that the tentative credit amount (adjusted for inflation) is reduced (but not below zero) to the extent that the applicable reference price exceeds $1.67 (adjusted for inflation). More specifically, § 45I(b)(2)(A) provides that the tentative credit amount (adjusted for inflation) is reduced by an amount which bears the same ratio to the tentative credit amount (adjusted for inflation) as the excess (if any) of the applicable reference price over $1.67 (adjusted for inflation), bears to $0.33 (adjusted for inflation). As a result, the MWC is not available if the applicable reference price for qualified natural gas production is $2.00 (adjusted for inflation) or more.

Section 45I(b)(2)(A) also provides that the applicable reference price for a taxable year is the reference price for the calendar year preceding the calendar year in which the taxable year begins. Section 45I(b)(2)(C)(ii) provides that the term “reference price” means, with respect to any calendar year, in the case of qualified natural gas production, the Secretary’s estimate of the annual average wellhead price per Mcf for all domestic natural gas.

Section 45I(b)(2)(B) provides that in the case of any taxable year beginning in a calendar year after 2005, each of the dollar amounts contained in § 45I(b)(2)(A) will be increased to an amount equal to such dollar amount multiplied by the inflation adjustment factor for such calendar year (determined under § 43(b)(3)(B) by substituting “2004” for “1990”).

.1 Inflation Adjustment. The inflation adjustment factor under § 45I(b)(2)(B) for calendar year 2019 is 1.3015.

.2 Reference Price. The Secretary’s estimate of the calendar year 2018 annual average wellhead price per Mcf for all domestic natural gas under § 45I(b)(2)(C)(ii) was calculated by applying the Producer Price Index commodity index for “Natural Gas from the Wellhead” (WPU053101051)1 published by the Bureau of Labor Statistics (BLS) as part of its Producer Price Index program, to the 2017 annual average wellhead price ($2.68) published in Notice 2019-37, 2019-37 I.R.B. 629. The annual Producer Price Index commodity index for natural gas published by the BLS was 83.4 in 2017 and 79.3 in 2018, which implies a ratio of 2018 to 2017 average wellhead prices of 0.951 (79.3 / 83.4). Therefore, the Secretary’s estimate of the calendar year 2018 annual average wellhead price per Mcf for all domestic natural gas is $2.55 per Mcf (0.951 x $2.68 per Mcf).

For years after 2018, the Secretary intends to continue calculating the reference price by application of the Producer Price Index commodity index for “Natural Gas from the Wellhead” (WPU053101051) published by the BLS to the previous year’s reference price.

Under § 45I(b)(1)(B) and (2)(B), the tentative credit amount used to calculate the MWC for taxable years beginning in calendar year 2019 is 65 cents per Mcf ($0.50 x 1.3015 inflation adjustment factor). To determine the credit amount for purposes of § 45I(a)(1), the tentative credit amount must be reduced as provided by § 45I(b)(2)(A).

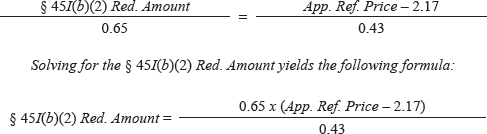

Pursuant to § 45I(b)(2)(A), the tentative credit amount for taxable years beginning in calendar year 2019 is reduced (but not below zero) by an amount (§ 45I(b)(2) Reduction Amount) which bears the same ratio to the tentative credit amount as (i) the excess (if any) of the applicable reference price over $2.17 ($1.67 x 1.3015 inflation adjustment factor), bears to (ii) $0.43 ($0.33 x 1.3015 inflation adjustment factor). Accordingly, the § 45I(b)(2) Reduction Amount (as adjusted for inflation) is computed as follows:

Using the applicable reference price of $2.55, the § 45I(b)(2) Reduction Amount is $0.57. Therefore, the credit amount used to calculate the MWC for taxable years beginning in calendar year 2019 is $0.08 per mcf ($0.65 - $0.57).

This notice is effective for qualified natural gas production during taxable years beginning in calendar year 2019.

This notice contains a proposed revenue procedure that sets forth updated procedures under which recognition of exemption from federal income tax for organizations described in § 501(c) of the Internal Revenue Code (Code) may be obtained on a group basis for subordinate organizations affiliated with and under the general supervision or control of a central organization. The proposed revenue procedure also sets forth updated procedures a central organization must follow to maintain a group exemption letter. The proposed revenue procedure would modify and supersede Rev. Proc. 80-27, 1980-1 C.B. 677 (as modified by Rev. Proc. 96-40, 1996-2 C.B. 301). The Internal Revenue Service (IRS) is issuing this guidance in proposed form to provide an opportunity for public comment because the IRS recognizes that, if finalized, the proposed revenue procedure would make substantial changes to the procedures set forth in Rev. Proc. 80-27 and that the application of these new procedures may impose an additional administrative burden on central organizations with group exemption letters in existence on the date the final revenue procedure is published in the Internal Revenue Bulletin (preexisting group exemption letters).

The IRS oversees more than 4,000 group exemption letters that include more than 440,000 subordinate organizations. The IRS has considered how to reduce the administrative burden and increase the efficiency of the group exemption letter program, to improve the integrity of data collected for purposes of program oversight, to increase the transparency of the program, and to increase compliance by central organizations and subordinate organizations with program requirements. For example, Rev. Proc. 80-27 requires a central organization to submit certain information regarding its subordinate organizations to the IRS annually in advance of the close of its accounting period. To facilitate the provision of information under this requirement, the IRS historically mailed each central organization a list of its subordinate organizations for verification and return. As of January 1, 2019, the IRS stopped providing these lists to central organizations because the provision of such lists was not required and imposed a significant administrative burden on the IRS.

Many of the IRS’s goals for the program are attainable only by updating the procedures currently described in Rev. Proc. 80-27. Accordingly, this notice contains a proposed revenue procedure that would make such changes if it is finalized. This notice discusses the changes the proposed revenue procedure would make to Rev. Proc. 80-27 and explains the reasons for the proposed changes and how the proposed changes would affect preexisting group exemption letters.

The proposed revenue procedure is intended to be a comprehensive resource regarding group exemption letters. Accordingly, information located in other guidance, such as in the Treasury Regulations or other revenue procedures, has been incorporated into the proposed revenue procedure, including, but not limited to, information with respect to the filing of group returns (as described in section 7 of the proposed revenue procedure) and donor or contributor reliance on group exemption letters (as described in section 12 of the proposed revenue procedure).

The proposed revenue procedure uses formatting similar to Rev. Proc. 2020-5, 2020-1 I.R.B. 241 (updated annually) and includes much of the same information but specifically tailored to apply to group exemption letters. For example, the proposed revenue procedure states when the IRS will issue a group exemption letter (see section 4 of the proposed revenue procedure) and under what circumstances the IRS may terminate a group exemption letter (see section 8 of the proposed revenue procedure). The proposed revenue procedure describes how a subordinate organization may obtain recognition of exemption or declare its exempt status (without obtaining recognition from the IRS), as applicable, if the IRS does not accept a request for a group exemption letter or declines to issue a group exemption letter or if the IRS or the central organization terminates the group exemption letter (in its entirety or only with respect to a particular subordinate organization) (see section 9.04 of the proposed revenue procedure). The proposed revenue procedure explains how the effective date of exemption is determined in each of these circumstances (see section 10 of the proposed revenue procedure). In particular, the proposed revenue procedure explains that, if a group exemption letter is terminated with respect to all subordinate organizations, a subordinate organization required to file an application for recognition of exemption has 27 months from the date of termination to obtain recognition of its exemption to avoid interruption of its exempt status (see section 10.03(1) of the proposed revenue procedure).

The proposed revenue procedure updates the procedures currently described in Rev. Proc. 80-27 by incorporating changes to the Code enacted since its publication in January of 1980.

(1) Automatic revocation.

The proposed revenue procedure clarifies the application of § 6033(j) to subordinate organizations. Section 6033(j) automatically revokes an organization’s exemption if the organization fails to file a required annual return or notice (as defined in section 2.05 of the proposed revenue procedure with reference to § 6033) for three consecutive years. See Pension Protection Act of 2006, Public Law 109-280 (120 Stat. 780 (2006)). The proposed revenue procedure explains that a subordinate organization that has had its exemption automatically revoked (within the meaning of section 2.06 of the proposed revenue procedure) and has not yet had its exemption reinstated after filing an application for reinstatement (within the meaning of section 2.07 of the proposed revenue procedure) is not eligible for initial inclusion in or subsequent addition to a group exemption letter (see section 3.04(5) of the proposed revenue procedure). A subordinate organization will be removed from a group exemption letter if its exemption is automatically revoked (see section 8.02(1)(c) of the proposed revenue procedure). When submitting the information required annually to maintain a group exemption letter (supplemental group ruling information, or SGRI, discussed in section 6 of the proposed revenue procedure), the central organization must notify the IRS of any subordinate organizations that are no longer included in the group exemption letter because such subordinate organizations have had their exemption automatically revoked (see section 6.02(2)(a)(ii) of the proposed revenue procedure). Under the proposed revenue procedure, the IRS may terminate a group exemption letter with respect to all subordinate organizations if more than half of the subordinate organizations have had their exemption automatically revoked (see section 8.01(1)(g) of the proposed revenue procedure).

(2) Notification of intent to operate as an organization described in § 501(c)(4).

Section 5.03(3)(c) of the proposed revenue procedure explains the application of § 506 to subordinate organizations. Section 506 requires an organization described in § 501(c)(4) to notify the Secretary that it is operating as an organization described in § 501(c)(4) no later than 60 days after the organization is established. See Protecting Americans from Tax Hikes Act of 2015, Public Law 114-113, Div. Q (129 Stat. 2242 (2015)) (PATH Act). Section 5.03(3)(c) of the proposed revenue procedure explains that a subordinate organization described in § 501(c)(4) that is included in (or subsequently added to) a group exemption letter must follow the procedures described in Rev. Proc. 2016-41, 2016-30 I.R.B. 165, and submit a completed electronic Form 8976, “Notice of Intent to Operate Under Section 501(c)(4).” This section explains that a subordinate organization may authorize an individual representing the central organization to submit Form 8976 on the subordinate organization’s behalf and to receive any communications relating to the subordinate organization’s submission.

The proposed revenue procedure would make additional modifications to the procedures currently described in Rev. Proc. 80-27. In general, the changes are intended: to increase efficiency, transparency, and compliance with the group exemption letter program; to improve the central organization’s ability to exercise general supervision or control over its subordinate organizations; and to reduce the administrative burden on the IRS. A transition rule and a grandfather rule (both discussed in the “Applicability” section of this notice and in section 14 of the proposed revenue procedure) address how these changes would apply to preexisting group exemption letters.

(1) Central organization requirements to obtain and maintain a group exemption letter.

The proposed revenue procedure includes two requirements a central organization must satisfy to obtain and maintain a group exemption letter in addition to the requirement set forth in Rev. Proc. 80-27 that a central organization must be described in § 501(c) or must be an instrumentality or an agency of a political subdivision. First, Rev. Proc. 80-27 does not require a central organization to have a specific number of subordinate organizations to obtain or to maintain a group exemption letter. Both Rev. Proc. 80-27 and section 2.02 of the proposed revenue procedure define the term “central organization” as an organization that has one or more subordinate organizations under its general supervision or control. However, the administrative burden of processing one group exemption letter request is comparable to the administrative burden of processing four applications (as defined in section 2.04 of the proposed revenue procedure). Furthermore, more than 300 group exemption letters in existence when the project was conducted included no subordinate organizations but considerable resources are required to administer the program for these group exemption letters. Accordingly, section 3.01(2) of the proposed revenue procedure requires a central organization to have at least five subordinate organizations to obtain a group exemption letter and at least one subordinate organization to maintain the group exemption letter thereafter.

Second, Rev. Proc. 80-27 does not limit the number of group exemption letters a central organization may maintain. However, maintaining more than one group exemption letter may adversely affect the central organization’s ability to exercise general supervision or control over its subordinate organizations. Traditionally, IRS electronic databases have not systemically tracked more than one group exemption letter for each central organization. Accordingly, section 3.01(3) of the proposed revenue procedure provides that a central organization may maintain only one group exemption letter.

(2) The central organization’s relationship with its subordinate organizations.

Consistent with Rev. Proc. 80-27, section 3.02(1) of the proposed revenue procedure requires a central organization to establish that each subordinate organization to be included in the group exemption letter be affiliated with the central organization and subject to its general supervision or control. Rev. Proc. 80-27, however, does not define the terms “affiliation,” “general supervision,” or “control.” This lack of definition has caused confusion and created a lack of consistency for both the IRS and central organizations. Accordingly, these terms are described in greater detail in sections 3.02(2), 3.02(3), and 3.02(4) of the proposed revenue procedure. Further, section 3.02(5) of the proposed revenue procedure provides that the descriptions of “general supervision” and “control” apply only for purposes of the proposed revenue procedure and § 1.6033-2(d) of the Treasury Regulations (relating to group returns).

(3) Organizations eligible for initial inclusion in or subsequent addition to a group exemption letter as subordinate organizations.

The proposed revenue procedure describes four new requirements that a subordinate organization must meet for initial inclusion in or subsequent addition to a group exemption letter.

(a) Matching requirements.

Rev. Proc. 80-27 provides that the central organization must establish that all subordinate organizations included in a group exemption letter request are described in the same paragraph of § 501(c), though not necessarily the paragraph in which the central organization is described. Thus, under Rev. Proc. 80-27, a central organization described in § 501(c)(3) may have a group exemption letter for subordinate organizations described in § 501(c)(4). Section 3.03(2)(a)(i) of the proposed revenue procedure retains the requirement that all subordinate organizations be described in the same paragraph of § 501(c). However, permitting a central organization to have subordinate organizations described in a paragraph of § 501(c) that is different from the paragraph describing the central organization limits the central organization’s ability to exercise general supervision or control over its subordinate organizations. Accordingly, section 3.03(2)(a)(ii) of the proposed revenue procedure requires all subordinate organizations initially included in or subsequently added to a group exemption letter to be described in the same paragraph of § 501(c) as the central organization. For example, if a central organization is described in § 501(c)(3), all the subordinate organizations initially included in or subsequently added to the group exemption letter must be described in § 501(c)(3). Nonetheless, section 3.03(2)(a)(iii) of the proposed revenue procedure explains that, if the central organization is either an instrumentality or an agency of a political subdivision and is not described in § 501(c), the matching requirement in section 3.03(2)(a)(ii) of the proposed revenue procedure does not apply. Accordingly, such a central organization may obtain and maintain a group exemption letter for subordinate organizations described in any paragraph of § 501(c) (provided that the eligibility requirements of section 3.03 of the proposed revenue procedure are met), as long as all the subordinate organizations are described in the same paragraph of § 501(c) (see section 3.03(2)(a)(i) of the proposed revenue procedure). For example, a state college or university may obtain and maintain a group exemption letter for organizations described in § 501(c)(3), provided that the state college or university can establish that it is a qualified governmental agency.

(b) Foundation classification requirement.

The second new requirement for initial inclusion in or subsequent addition to a group exemption letter introduced by the proposed revenue procedure involves the foundation classification of subordinate organizations described in § 501(c)(3). Rev. Proc. 80-27 does not require subordinate organizations described in § 501(c)(3) to have any particular foundation classification under § 509(a) (other than the prohibition of subordinate organizations that are private foundations). Traditionally, IRS electronic databases have not systemically tracked multiple foundation classifications in connection with a particular group exemption letter. This limitation reduces transparency, complicates compliance, and increases the administrative burden because different foundation classifications have different requirements. Accordingly, section 3.03(2)(b)(i) of the proposed revenue procedure provides that, if the subordinate organizations initially included in or subsequently added to a group exemption letter are described in § 501(c)(3), all such subordinate organizations must be classified as public charities under the same paragraph of § 509(a).

Subordinate organizations described in § 501(c)(3) and classified under § 509(a)(1) are not required to be classified under the same paragraph of § 170(b)(1)(A). For example, subordinate organizations described in § 501(c)(3) that are classified under § 509(a)(1) as churches described in § 170(b)(1)(A)(i), educational organizations described in § 170(b)(1)(A)(ii), or hospitals described in § 170(b)(1)(A)(iii) may all be initially included in or subsequently added to the same group exemption letter, provided that the other requirements of the proposed revenue procedure are satisfied. Nonetheless, the IRS is considering how, and the extent to which, this requirement may affect a central organization’s ability to exercise general supervision or control over its subordinate organizations and, after an appropriate transition period, eventually may require all subordinate organizations classified under § 509(a)(1) to be classified under the same paragraph of § 170(b)(1)(A).

Public support is calculated annually and may change from year to year. See §§ 170(b)(1)(A)(vi) & 509(a)(1) & (2). Thus, for purposes of the foundation classification requirement described in the proposed revenue procedure, a subordinate organization classified under § 509(a)(1) and described in § 170(b)(1)(A)(vi) will be considered as having the same foundation classification as a subordinate organization classified under § 509(a)(2), and vice versa.

Additionally, subordinate organizations described in § 501(c)(3) are not required to be classified under the same paragraph of § 509(a) as the central organization. For example, subordinate organizations classified as hospitals under §§ 509(a)(1) and 170(b)(1)(A)(iii) may be included in a group exemption letter maintained by a central organization that is a Type III supporting organization described in § 509(a)(3).

(c) Similar purpose requirement.

The third new requirement for initial inclusion in or subsequent addition to a group exemption letter adheres to the original intent of the group exemption letter program by requiring certain subordinate organizations included in a group exemption letter to have the same or similar purposes. This requirement will facilitate the central organization’s exercise of general supervision or control and reduce the administrative burden of the group exemption letter program. Therefore, section 3.03(2)(c) of the proposed revenue procedure requires all subordinate organizations described in § 501(c) (other than § 501(c)(3)) initially included in or subsequently added to a group exemption letter to be described by the same National Taxonomy of Exempt Entities (NTEE) Code (as defined in section 2.08 of the proposed revenue procedure). In this case, the proposed revenue procedure directs a central organization requesting a group exemption letter to visit the Urban Institute, National Center for Charitable Statistics, website at nccs.urban.org for a complete list of NTEE codes.

The IRS has chosen to use NTEE codes, rather than a different coding system, such as the North American Industry Classification System, because the NTEE codes were created specifically to describe the activities engaged in by exempt organizations that further one or more exempt purposes. Indeed, the IRS already requires organizations applying for recognition under § 501(c)(3) to enter the NTEE code that best describes the organization’s activities on Form 1023-EZ, “Streamlined Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code.”

Subordinate organizations described in § 501(c)(3) initially included in or subsequently added to a group exemption letter are not required to have the same primary purpose (and therefore are not required to provide an NTEE code), because, although such subordinate organizations must be classified in the same paragraph of § 509(a), such subordinate organizations may have different religious, charitable, educational, or other exempt purposes.

(d) Uniform governing instrument requirement.

The fourth new requirement for initial inclusion in or subsequent addition to a group exemption letter introduced by the proposed revenue procedure is a modification to the requirement in Rev. Proc. 80-27 directing a central organization to include a sample copy the governing instrument adopted by the subordinate organizations with its request for a group exemption letter. If a uniform governing instrument is not used, Rev. Proc. 80-27 requires the central organization to submit copies of representative instruments. However, governing instruments that are not uniform are not consistent with the similar purpose requirement. Accordingly, section 3.03(2)(d) of the proposed revenue procedure eliminates the option of submitting copies of representative instruments in the absence of a uniform governing instrument and requires all subordinate organizations to adopt a uniform governing instrument. Section 5.03(2)(a) of the proposed revenue procedure requires the central organization to submit a copy of the uniform governing instrument with its request for a group exemption letter. Representative instruments are no longer acceptable for this purpose.

Section 3.03(2)(d) of the proposed revenue procedure includes an exception for subordinate organizations described in § 501(c)(3) because, under the foundation classification requirement, such subordinate organizations may have different religious, charitable, educational, or other exempt purposes and because the similar purpose requirement does not apply to subordinate organizations described in § 501(c)(3). Accordingly, the proposed revenue procedure allows the governing instruments of subordinate organizations described in § 501(c)(3) to describe different purposes. The proposed revenue procedure further explains that, if a group exemption letter includes subordinate organizations described in § 501(c)(3) with different purposes, the governing instrument describing each purpose should be a uniform governing instrument. For example, if a group exemption letter includes subordinate organizations that are schools and hospitals, all the subordinate organizations that are schools should adopt a uniform governing instrument describing their educational purpose and all the subordinate organizations that are hospitals should adopt a uniform governing instrument describing their charitable purpose.

(4) Organizations not eligible for inclusion in or subsequent addition to a group exemption letter as subordinate organizations.

Rev. Proc. 80-27 states that a group exemption letter may not include any subordinate organization that is organized and operated in a foreign country or that is described in § 501(c)(3) and classified as a private foundation under § 509(a). The proposed revenue procedure generally retains these requirements, except it permits a subordinate organization to operate in a foreign country, provided that it is organized in the United States. More specifically, section 3.04(1) of the proposed revenue procedure provides that a subordinate organization that is organized in a foreign country may not be initially included in or subsequently added to a group exemption letter. A subordinate organization that is organized in the United States is subject to federal tax law even if it operates in a foreign country, and a central organization therefore should be able to exercise general supervision or control over such a subordinate organization. In addition, section 3.04(2) of the proposed revenue procedure states that an organization described in § 501(c)(3) that is classified as a private foundation under § 509(a) is not eligible for initial inclusion in or subsequent addition to a group exemption letter as a subordinate organization.

The proposed revenue procedure also provides that other types of organizations may not be initially included in or subsequently added to a group exemption letter as subordinate organizations. Sections 3.04(3) and 3.04(4) of the proposed revenue procedure state that neither an organization described in § 501(c)(3) that is classified as a Type III supporting organization under § 509(a)(3) nor a qualified nonprofit health insurance issuer (QNHII) described in § 501(c)(29) is eligible for initial inclusion in or subsequent addition to a group exemption letter as a subordinate organization. Both Type III supporting organizations and QNHIIs are subject to complex requirements. Permitting these types of organizations to be subordinate organizations would not be in the sound interest of tax administration because of the complexity of the rules governing such organizations and, in the case of Type III supporting organizations, the history of abuse associated with such organizations.

Additionally, section 3.04(5) of the proposed revenue procedure states that an organization that has had its exemption automatically revoked and that has not yet had its exemption reinstated after filing an application for reinstatement may not be initially included in or subsequently added to a group exemption letter as a subordinate organization. An organization that has had its exemption automatically revoked is required to apply for reinstatement under § 6033(j)(2). However, unlike the other types of organizations that may not be initially included in or subsequently added to a group exemption letter as subordinate organizations, such as private foundations, an organization that has had its exemption automatically revoked is eligible to become a subordinate organization after it has filed an application for reinstatement and has had its exemption reinstated, provided that it meets the other requirements of the proposed revenue procedure.

(5) Authorization for initial inclusion in or subsequent addition to a group exemption letter.

Rev. Proc. 80-27 requires a subordinate organization to authorize the central organization to include it in the request for a group exemption letter. Section 3.05(1) of the proposed revenue procedure retains this requirement, but section 3.05(2) of the proposed revenue procedure adds the requirement that the authorization permit the central organization to remove the subordinate organization from the group exemption letter if the subordinate organization fails to comply with the requirements of the proposed revenue procedure. Consistent with Rev. Proc. 80-27, section 3.05(3) of the proposed revenue procedure requires the central organization to retain the authorization but clarifies that the central organization must retain the authorization only while the group exemption letter includes the particular subordinate organization, rather than for the entire duration the group exemption letter is in effect.

(6) Information required to maintain a group exemption letter.

Both Rev. Proc. 80-27 and the proposed revenue procedure require a central organization to submit certain information (supplemental group ruling information, or SGRI) annually to maintain a group exemption letter. Under section 6.01 of the proposed revenue procedure, a central organization must submit the SGRI at least 30 days, rather than 90 days as required by Rev. Proc. 80-27, before the close of its annual accounting period. This change is intended to increase the accuracy of the SGRI submitted by the central organization. Nonetheless, the proposed revenue procedure explains that a central organization may provide additional updates at any time. Section 6.05 of the proposed revenue procedure includes the exception to the SGRI filing requirement originally included in Pub. 4573 for central organizations described in § 501(c)(3) that are churches or conventions or associations of churches. More specifically, section 6.05 of the proposed revenue procedure provides that a central organization that is a church or a convention or association of churches may, but is not required to, submit the SGRI.

(7) Declaratory judgment provisions of § 7428.

In 1976, Congress enacted § 7428 to permit organizations described in § 501(c)(3) to file a declaratory judgment action in the case of an actual controversy involving determinations made by the IRS. See Tax Reform Act of 1976, Public Law 94-455 (90 Stat. 1520 (1976)). The PATH Act extended application of § 7428 to all organizations described in § 501(c).

Rev. Proc. 80-27 does not address the application of § 7428 to either central organizations or subordinate organizations. Nevertheless, questions exist regarding how the statute applies in the context of group exemption letters. Accordingly, section 11 of the proposed revenue procedure explains when § 7428 applies in the group exemption letter context. With respect to a central organization, section 11.02 of the proposed revenue procedure clarifies that section 10.02 of Rev. Proc. 2020-5 (or its successor) describes when § 7428 applies. With respect to subordinate organizations, section 11.03 of the proposed revenue procedure describes the limited circumstances in which § 7428 applies.

Section 11.03(1) of the proposed revenue procedure explains that § 7428 applies to a final determination by the IRS that a subordinate organization is no longer described in § 501(c) and therefore is not exempt under § 501(a). Such a determination occurs when the IRS terminates a group exemption letter with respect to a particular subordinate organization under section 8.02(1)(b)(i) of the proposed revenue procedure. Section 11.03(2) of the proposed revenue procedure explains that § 7428 also applies to a final determination by the IRS that a subordinate organization was not eligible for initial inclusion in or subsequent addition to a group exemption letter under section 3.04 of the proposed revenue procedure (other than under section 3.04(5) of the proposed revenue procedure regarding automatic revocation). Such a determination occurs when the IRS terminates a group exemption letter with respect to a particular subordinate organization under section 8.02(1)(b)(ii) of the proposed revenue procedure. Section 11.04 of the proposed revenue procedure explains that § 7428 does not apply to certain other actions the IRS may take, such as not accepting a group exemption letter request for a reason described in section 4.02 of the proposed revenue procedure or declining to issue a group exemption letter for a reason described in section 4.03 of the proposed revenue procedure.

Section 11.05 of the proposed revenue procedure explains that a subordinate organization must file the declaratory judgment action under § 7428 with respect to a determination affecting its own initial or continuing qualification or classification; the central organization may not file the declaratory judgment action under § 7428 on behalf of the subordinate organization. Similarly, a subordinate organization may not file a declaratory judgment action under § 7428 on behalf of its central organization.

The proposed revenue procedure will apply to group exemption letters requested and issued after the date the final revenue procedure is published in the Internal Revenue Bulletin and to preexisting group exemption letters (see sections 14.01 and 14.02 of the proposed revenue procedure). However, section 14.02(2)(a) of the proposed revenue procedure provides that the requirements that a central organization have at least one subordinate organization to maintain a group exemption letter (see section 3.01(2) of the proposed revenue procedure) and that the central organization maintain only one group exemption letter (see section 3.01(3) of the proposed revenue procedure) will apply after a one year transition period. Section 14.02(2)(b) of the proposed revenue procedure directs a central organization with a preexisting group exemption letter, but no preexisting subordinate organizations, to add at least one subordinate organization to the preexisting group exemption letter or to notify the IRS of its intent to terminate the group exemption letter. Section 14.02(2)(c) of the proposed revenue procedure directs a central organization with more than one preexisting group exemption letter to determine, during the transition period, which, if any, preexisting group exemption letter it intends to maintain and to notify the IRS of its intent to terminate any additional preexisting group exemption letters.

The proposed revenue procedure will apply to all new subordinate organizations added to a preexisting group exemption letter (see sections 2.11 and 14.02(3) of the proposed revenue procedure). Section 14.02(3)(b) of the proposed revenue procedure describes the information a central organization must submit the first time it adds one or more subordinate organizations to a preexisting group exemption letter.

The proposed revenue procedure generally will apply to preexisting subordinate organizations (as defined in section 2.10 of the proposed revenue procedure). However, section 14.02(4)(b)(i) through (iii) of the proposed revenue procedure provide a grandfather rule with respect to certain requirements in the proposed revenue procedure. In particular, the following definitions and rules will not apply to preexisting subordinate organizations:

-

the definitions of “general supervision” or “control” in sections 3.02(3) and 3.02(4) of the proposed revenue procedure;

-

the matching, foundation classification, similar purpose, and uniform governing instrument requirements in section 3.03(2) of the proposed revenue procedure; and

-

the limitation applicable to Type III supporting organizations in section 3.04(3) of the proposed revenue procedure.

Instead, definitions and rules similar to those contained in Rev. Proc. 80-27 will apply. Section 14.02(4)(c) of the proposed revenue procedure clarifies that preexisting subordinate organizations must all be described in the same paragraph of § 501(c), though not necessarily the same paragraph as the central organization; preexisting subordinate organizations described in § 501(c)(3) may be classified in any paragraph of § 509(a) (including § 509(a)(3)); and all preexisting subordinate organizations may have different primary purposes and unique, as opposed to “uniform,” governing instruments.

Additionally, section 14.02(4)(b)(iv) of the proposed revenue procedure provides that the requirement that the authorization for initial inclusion in or subsequent addition to a group exemption letter described in section 3.05(1) of the proposed revenue procedure permit the central organization to remove a subordinate organization in certain circumstances does not apply to preexisting subordinate organizations. The IRS recognizes that imposing this requirement on preexisting group exemption letters could require the central organization to obtain new authorizations from all of its preexisting subordinate organizations, which would likely impose a considerable administrative burden on many central organizations.

Although the definitions of “general supervision” or “control” in sections 3.02(3) and 3.02(4) of the proposed revenue procedure do not apply to preexisting group exemption letters, section 14.02(4)(e) of the proposed revenue procedure explains that a central organization that meets the requirements of section 3.02(3) or section 3.02(4) of the proposed revenue procedure with respect to a particular preexisting subordinate organization will be deemed to exercise “general supervision” or “control,” as applicable, over that preexisting subordinate organization.

Finally, section 14.03 of the proposed revenue procedure provides examples of how the grandfather and transition rules function.

The IRS requests comments on all aspects of the proposed revenue procedure, including the grandfather and transition rules. In particular, the IRS requests comments regarding:

-

the administrative burden imposed by the collections of information in sections 3.02(3) (certain information a central organization that exercises general supervision over its subordinate organizations must annually collect from its subordinate organizations and transmit to its subordinate organizations), 3.05 (authorization for initial inclusion in or subsequent addition to a group exemption letter as a subordinate organization), and 6 (SGRI) of the proposed revenue procedure;

-

factors indicating that a subordinate organization is affiliated with a central organization for purposes of section 3.02(2) of the proposed revenue procedure (description of affiliation); and

-

whether central organizations with more than one preexisting group exemption letter would benefit from procedures permitting the consolidation or transfer of one or more preexisting group exemption letters.

Comments should be submitted on or before August 16, 2020. Please include Notice 2020-36 on the cover page. Comments should be sent to the following address:

Internal Revenue Service

CC:PA:LPD:PR (Notice 2020-36), Room 5203

P.O. Box 7604

Ben Franklin Station

Washington, DC 20044

Submissions may be hand delivered Monday through Friday between the hours of 8 a.m. and 4 p.m. to:

Internal Revenue Service

Courier’s Desk

1111 Constitution Ave., N.W.

Washington, DC 20224

Attn: CC:PA:LPD:PR (Notice 2020-36)

Submissions may also be sent electronically to the following e-mail address:

Notice.Comments@irscounsel.treas.gov.

Please include “Notice 2020-36” in the subject line.

All comments will be available for public inspection and copying.

CONTINUED APPLICATION OF REV. PROC. 80-27

Pending publication of the final revenue procedure in the Internal Revenue Bulletin, Rev. Proc. 80-27 continues to apply. However, the IRS will not accept any requests for group exemption letters starting on June 17, 2020 (30 days after publication of this notice in the Internal Revenue Bulletin) until publication of the final revenue procedure or other guidance in the Internal Revenue Bulletin.

DRAFTING INFORMATION

The principal authors of this notice are Seth J. Groman and Stephanie N. Robbins of the Office of Associate Chief Counsel (Employee Benefits, Exempt Organizations and Employment Taxes). For further information regarding this notice contact Seth J. Groman at (202) 317-4086 (not a toll-free number).

| SECTION 1. PURPOSE |

| SECTION 2. DEFINITIONS |

| SECTION 3. REQUIREMENTS TO OBTAIN AND MAINTAIN A GROUP EXEMPTION LETTER |

| .01 Central organization |

| (1) Exemption |

| (2) Minimum number of subordinate organizations |

| (3) Only one group exemption letter |

| .02 The central organization’s relationship with its subordinate organizations |

| (1) In general |

| (2) Affiliation |

| (3) General supervision |

| (4) Control |

| (5) Application |

| .03 Organizations eligible for initial inclusion in or subsequent addition to a group exemption letter as subordinate organizations |

| (1) In general |

| (2) Requirements for initial inclusion in or subsequent addition to a group exemption letter |

| .04 Organizations not eligible for initial inclusion in or subsequent addition to a group exemption letter as subordinate organizations |

| .05 Authorization for initial inclusion in or subsequent addition to a group exemption letter as a subordinate organization |

| (1) In general |

| (2) Removal |

| (3) Retention of the authorization by the central organization |

| .06 Employer identification numbers (EINs) |

| .07 Annual information return or notice |

| SECTION 4. ISSUANCE OF GROUP EXEMPTION LETTERS |

| .01 Group exemption letter requests |

| .02 Non-acceptance |

| .03 Circumstances under which group exemption letters are not ordinarily issued |

| SECTION 5. INSTRUCTIONS FOR REQUESTING A GROUP EXEMPTION LETTER |

| .01 Group exemption letter request |

| .02 Information about the central organization |

| .03 Information about the subordinate organizations |

| (1) In general |

| (2) Supporting information |

| (3) Additional requirements |

| .04 Request for a new group exemption letter after the termination of a group exemption letter |

| SECTION 6. INFORMATION REQUIRED TO MAINTAIN A GROUP EXEMPTION LETTER |

| .01 Information required annually |

| .02 Supplemental group ruling information |

| (1) Changes in purposes or activities |

| (2) Lists of certain changes, removals, or additions |

| (3) Organizations to be added to the group exemption letter as subordinate organizations |

| (4) No change |

| (5) Intent to terminate the group exemption letter |

| .03 Address |

| .04 Additional information |

| .05 Exception for central organizations that are churches or conventions or associations of churches |

| SECTION 7. ANNUAL FILING REQUIREMENT |

| .01 In general |

| .02 Group returns |

| SECTION 8. TERMINATION OF THE GROUP EXEMPTION LETTER |

| .01 Termination of the group exemption letter with respect to all subordinate organizations |

| (1) Termination by the IRS |

| (2) Termination by the central organization |

| .02 Termination of the group exemption letter with respect to a particular subordinate organization |

| (1) Removal from the group exemption letter |

| (2) Group exemption letter remains in effect |

| SECTION 9. EFFECT OF NON-ACCEPTANCE, NON-ISSUANCE, TERMINATION, OR REMOVAL |

| .01 Effect of non-acceptance or non-issuance |

| .02 Effect of termination |

| (1) In general |

| (2) Churches or conventions or associations of churches |

| .03 Effect of removal |

| .04 Subsequent recognition of exemption |

| (1) In general |

| (2) Organization required to file an application |

| (3) Organization not required to file an application |

| (4) Automatic revocation |

| SECTION 10. EFFECTIVE DATE OF EXEMPTION |

| .01 Initial inclusion |

| .02 Subsequent addition |

| .03 Termination or removal |

| (1) In general |

| (2) Automatic revocation |

| (3) Declaratory judgment action |

| SECTION 11. DECLARATORY JUDGMENT PROVISIONS OF § 7428 |

| .01 In general |

| .02 Application to central organizations |

| .03 Application to subordinate organizations |

| .04 Actions to which § 7428 does not apply |

| .05 Who must file |

| SECTION 12. RELIANCE |

| .01 By a central or subordinate organization |

| .02 By grantors and contributors |

| SECTION 13. DISCLOSURE OF GROUP EXEMPTION LETTER REQUESTS AND GROUP EXEMPTION LETTERS |

| SECTION 14. APPLICABILITY |

| .01 New group exemption letters |

| .02 Preexisting group exemption letters |

| (1) In general |

| (2) Certain sections applicable to preexisting group exemption letters after a transition period |

| (3) New subordinate organizations |

| (4) Preexisting subordinate organizations |

| .03 Examples |

| (1) One preexisting group exemption letter for subordinate organizations described in a different paragraph of § 501(c) than the central organization |

| (2) One preexisting group exemption letter for subordinate organizations described in the same paragraph of § 501(c) as the central organization |

| (3) Two preexisting group exemption letters for subordinate organizations described in different paragraphs of § 501(c) |

| (4) Central organization that is not described in § 501(c) with two preexisting group exemption letters for subordinate organizations described in different paragraphs of § 501(c) |

| (5) One preexisting group exemption letter with no subordinate organizations |

| (6) One preexisting group exemption letter with subordinate organizations described in different paragraphs of § 501(c) |

| SECTION 15. EFFECT ON OTHER REVENUE PROCEDURES |

| SECTION 16. EFFECTIVE DATE |

The purpose of this revenue procedure is to modify and supersede Rev. Proc. 80-27, 1980-1 C.B. 677 (as modified by Rev. Proc. 96-40, 1996-2 C.B. 301) by setting forth updated procedures under which recognition of exemption from federal income tax for organizations described in § 501(c) of the Internal Revenue Code (Code) may be obtained on a group basis for subordinate organizations affiliated with and under the general supervision or control of a central organization. This revenue procedure relieves each subordinate organization covered by a group exemption letter from filing its own application for recognition of exemption. This revenue procedure also sets forth updated procedures a central organization must follow to maintain a group exemption letter. This revenue procedure is provided as a matter of sound tax administration for the administrative convenience of central organizations and the Internal Revenue Service (IRS).

.01 The term “group exemption letter” means a letter issued to a central organization recognizing on a group basis the exemption of subordinate organizations described in § 501(c) on whose behalf the central organization has applied for recognition of exemption in accordance with this revenue procedure.

.02 The term “central organization” means an organization that has one or more subordinate organizations under its general supervision or control.

.03 The term “subordinate organization” means a chapter, local, post, or unit of a central organization. It may or may not be incorporated, but it must have an organizing document (see section 3.03(2)(d) of this revenue procedure).

.04 The term “application” means a request for recognition of exemption from federal income tax under § 501 in the manner described by Rev. Proc. 2020-5, 2020-1 I.R.B. 241 (or its successor).

.05 The term “annual information return or notice” means the return or notice an organization must file annually under § 6033(a) or § 6033(i) (that is, Form 990, “Return of Organization Exempt From Income Tax”; Form 990-EZ, “Short Form Return of Organization Exempt From Income Tax”; or Form 990-N, “Electronic Notice (e-Postcard) for Tax-Exempt Organizations Not Required to File Form 990 or Form 990-EZ”).

.06 The term “automatically revoked” refers to an organization that has had its exemption automatically revoked by operation of § 6033(j) for failure to file an annual information return or notice for three consecutive years.

.07 The term “application for reinstatement” means an application filed in the manner described by Rev. Proc. 2014-11, 2014-3 I.R.B. 411, as supplemented by Rev. Proc. 2020-5 (or its successor), after an organization’s exemption has been automatically revoked.

.08 The term “National Taxonomy of Exempt Entities code” or “NTEE code” means a three-character series of letters and numbers that is used to classify an organization. For a complete list of NTEE codes, visit the Urban Institute, National Center for Charitable Statistics website at nccs.urban.org.

.09 The term “preexisting group exemption letter” means a group exemption letter in existence on the date the final revenue procedure is published in the Internal Revenue Bulletin.

.10 The term “preexisting subordinate organization” means, with respect to a preexisting group exemption letter, a subordinate organization included in the preexisting group exemption letter on or before the date the final revenue procedure is published in the Internal Revenue Bulletin.

.11 The term “new subordinate organization” means a subordinate organization subsequently added to a preexisting group exemption letter after the date the final revenue procedure is published in the Internal Revenue Bulletin.

.12 The term “supplemental group ruling information” or “SGRI” means the information described in section 6 of this revenue procedure that a central organization must submit annually to the IRS about its subordinate organizations unless an exception applies.

.01 Central organization. (1) Exemption. (a) In general. A central organization must be—

(i) Described in § 501(c);

(ii) An instrumentality; or

(iii) An agency of a political subdivision.

(b) Recognition of exemption. A central organization described in § 501(c) (see section 3.01(1)(a)(i) of this revenue procedure) must obtain recognition of exemption from the IRS by filing an application or, in the case of a central organization that has had its exemption automatically revoked, by filing an application for reinstatement.

(2) Minimum number of subordinate organizations. A central organization must have at least five subordinate organizations to obtain a group exemption letter, and it must have at least one subordinate organization to maintain the group exemption letter thereafter (except as provided in section 14.02(2)(a)(i) of this revenue procedure, which provides a transition period for preexisting group exemption letters).

(3) Only one group exemption letter. A central organization may maintain only one group exemption letter (except as provided in section 14.02(2)(a)(ii) of this revenue procedure, which provides a transition period for preexisting group exemption letters).

.02 The central organization’s relationship with its subordinate organizations. (1) In general. A central organization must establish that each subordinate organization to be included in the group exemption letter is affiliated with the central organization (as described in section 3.02(2) of this revenue procedure) and subject to its general supervision (as described in section 3.02(3) of this revenue procedure) or control (as described in section 3.02(4) of this revenue procedure).

(2) Affiliation. A subordinate organization’s affiliation with the central organization is demonstrated by the entirety of the information required to be submitted in section 5.03 of this revenue procedure.

(3) General supervision. A subordinate organization is subject to the central organization’s general supervision if the central organization—

(a) annually obtains, reviews, and retains information on the subordinate organization’s finances, activities, and compliance with annual filing requirements (see section 7 of this revenue procedure), and

(b) transmits written information to (or otherwise educates) the subordinate organization about the requirements to maintain tax-exempt status under the appropriate paragraph of § 501(c), including annual filing requirements (see section 7 of this revenue procedure).

(4) Control. A subordinate organization is subject to the central organization’s control if—

(a) The central organization appoints a majority of the subordinate organization’s officers, directors, or trustees; or

(b) A majority of the subordinate organization’s officers, directors, or trustees are officers, directors, or trustees of the central organization.

(5) Application. The term “general supervision” described in section 3.02(3) of this revenue procedure and the term “control” described in section 3.02(4) of this revenue procedure apply only for purposes of this revenue procedure and § 1.6033-2(d) of the Treasury Regulations (relating to group returns).

.03 Organizations eligible for initial inclusion in or subsequent addition to a group exemption letter as subordinate organizations. (1) In general. Unless described in section 3.04 of this revenue procedure and subject to the requirements described in section 3.03(2) of this revenue procedure, an organization described in § 501(c) may be eligible for initial inclusion in or subsequent addition to a group exemption letter as a subordinate organization.

(2) Requirements for initial inclusion in or subsequent addition to a group exemption letter. All subordinate organizations initially included in or subsequently added to a group exemption letter must meet the following requirements (except as provided in section 14.02(4) of this revenue procedure regarding preexisting subordinate organizations).

(a) Matching requirements. (i) Subordinate organizations. All subordinate organizations initially included in or subsequently added to a group exemption letter must be described in the same paragraph of § 501(c).

(ii) Central organization described in § 501(c). If the central organization is described in § 501(c), all subordinate organizations initially included in or subsequently added to a group exemption letter must be described in the same paragraph of § 501(c) as the central organization, including a central organization that is either an instrumentality or an agency of a political subdivision and that is described in § 501(c). For example, if a central organization is described in § 501(c)(3), all the subordinate organizations initially included in or subsequently added to the group exemption letter must also be described in § 501(c)(3).

(iii) Central organization not described in § 501(c). If the central organization is either an instrumentality or an agency of a political subdivision and is not described in § 501(c), the matching requirement described in section 3.03(2)(a)(ii) of this revenue procedure does not apply. In this case, such a central organization may have subordinate organizations described in any paragraph of § 501(c), provided that the organizations are eligible to be subordinate organizations (see section 3.04 of this revenue procedure) and the subordinate organizations initially included in or subsequently added to the group exemption letter are all described in the same paragraph of § 501(c) (see section 3.03(2)(a)(i) of this revenue procedure).

(b) Foundation classification requirement. (i) In general. Except as provided in section 3.03(2)(b)(iii) of this revenue procedure, all subordinate organizations described in § 501(c)(3) that are initially included in or subsequently added to a group exemption letter must be classified as public charities under the same paragraph of § 509(a) (but see section 3.04(3) of this revenue procedure, which provides that an organization described in § 501(c)(3) that is classified as a Type III supporting organization is not eligible to be initially included in or subsequently added to a group exemption letter as a subordinate organization).