)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

)

or https:// means you've safely connected to the .gov website. Share sensitive information only on official, secure websites.

Internal Revenue Bulletin: 2022-21

May 23, 2022

These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations.

This revenue procedure provides two simplified procedures for bona fide residents of Puerto Rico who are not otherwise required to file taxable year 2021 Federal tax returns, and who meet certain other requirements (Puerto Rico CTC filers) to claim the child tax credit. Under section 4 of this revenue procedure, Puerto Rico CTC filers who file simplified U.S. self-employment tax returns may omit their modified adjusted gross income for the purpose of claiming the child tax credit. Under section 5 of this revenue procedure, Puerto Rico CTC filers who file simplified Federal income tax returns may omit their modified adjusted gross income for the purpose of claiming the child tax credit.

26 CFR 1.6012-1: Individuals required to make returns of income.

(Also Part I, §§ 24, 933, 7527A; 1.933-1.)

These proposed regulations provide guidance relating to the use of actuarial tables in valuing annuities, interests for life or a term of years, and remainder or reversionary interests. These regulations will affect the valuation of inter vivos and testamentary transfers of interests dependent on one or more measuring lives. These regulations are necessary because section 7520(c)(3) directs the Secretary to update the actuarial tables to reflect the most recent mortality experience available.

This notice publishes the inflation adjustment factor and reference price for calendar year 2022 for the renewable electricity production credit under section 45 of the Internal Revenue Code. The notice also provides the credit amounts for calendar year 2022 under section 45.

The notice announces that under § 613A(c)(6)(C) of the Internal Revenue Code, the applicable percentage for purposes of determining percentage depletion on marginal properties for calendar year 2022 is 15 percent. The format of the notice is identical to the format of notices previously published on this issue.

Provide America’s taxpayers top-quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all.

The Internal Revenue Bulletin is the authoritative instrument of the Commissioner of Internal Revenue for announcing official rulings and procedures of the Internal Revenue Service and for publishing Treasury Decisions, Executive Orders, Tax Conventions, legislation, court decisions, and other items of general interest. It is published weekly.

It is the policy of the Service to publish in the Bulletin all substantive rulings necessary to promote a uniform application of the tax laws, including all rulings that supersede, revoke, modify, or amend any of those previously published in the Bulletin. All published rulings apply retroactively unless otherwise indicated. Procedures relating solely to matters of internal management are not published; however, statements of internal practices and procedures that affect the rights and duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service on the application of the law to the pivotal facts stated in the revenue ruling. In those based on positions taken in rulings to taxpayers or technical advice to Service field offices, identifying details and information of a confidential nature are deleted to prevent unwarranted invasions of privacy and to comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not have the force and effect of Treasury Department Regulations, but they may be used as precedents. Unpublished rulings will not be relied on, used, or cited as precedents by Service personnel in the disposition of other cases. In applying published rulings and procedures, the effect of subsequent legislation, regulations, court decisions, rulings, and procedures must be considered, and Service personnel and others concerned are cautioned against reaching the same conclusions in other cases unless the facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code. This part includes rulings and decisions based on provisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation. This part is divided into two subparts as follows: Subpart A, Tax Conventions and Other Related Items, and Subpart B, Legislation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous. To the extent practicable, pertinent cross references to these subjects are contained in the other Parts and Subparts. Also included in this part are Bank Secrecy Act Administrative Rulings. Bank Secrecy Act Administrative Rulings are issued by the Department of the Treasury’s Office of the Assistant Secretary (Enforcement).

Part IV.—Items of General Interest. This part includes notices of proposed rulemakings, disbarment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index for the matters published during the preceding months. These monthly indexes are cumulated on a semiannual basis, and are published in the last Bulletin of each semiannual period.

This notice publishes the inflation adjustment factor and reference price for calendar year 2022 for the renewable electricity production credit under section 45 of the Internal Revenue Code. The 2022 inflation adjustment factor and reference price are used in determining the availability of the credit and apply to calendar year 2022 sales of kilowatt hours of electricity produced in the United States or a possession thereof from qualified energy resources. For calendar year 2022, the credit period for refined coal production and Indian coal production expired.

Section 45(a) provides that the renewable electricity production credit for any tax year is an amount equal to the product of 1.5 cents multiplied by the kilowatt hours of specified electricity produced by the taxpayer and sold to an unrelated person during the tax year. This electricity must be produced from qualified energy resources and at a qualified facility during the 10-year period beginning on the date the facility was originally placed in service.

Section 45(b)(1) provides that the amount of the credit determined under section 45(a) is reduced by an amount which bears the same ratio to the amount of the credit as (A) the amount by which the reference price for the calendar year in which the sale occurs exceeds 8 cents, bears to (B) 3 cents. Under section 45(b)(2), the 1.5 cent amount in section 45(a) and the 8 cent amount in section 45(b)(1) are each adjusted by multiplying such amount by the inflation adjustment factor for the calendar year in which the sale occurs. If any amount as increased under the preceding sentence is not a multiple of 0.1 cent, the amount is rounded to the nearest multiple of 0.1 cent. In the case of electricity produced in open-loop biomass facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic renewable energy facilities, section 45(b)(4)(A) requires the amount in effect under section 45(a)(1) (before rounding to the nearest 0.1 cent) to be reduced by one-half.

Section 45(b)(5) provides that in the case of any facility using wind to produce electricity, the amount of the credit determined under section 45(a) (determined after the application of section 45(b)(1), (2), and (3) and without regard to section 45(b)(5)) shall be reduced by (A) in the case of any facility the construction of which begins after December 31, 2016, and before January 1, 2018, 20 percent, (B) in the case of any facility the construction of which begins after December 31, 2017, and before January 1, 2019, 40 percent, (C) in the case of any facility the construction of which begins after December 31, 2018, and before January 1, 2020, 60 percent, and (D) in the case of any facility the construction of which begins after December 31, 2019, and before January 1, 2022, 40 percent.

Section 45(c)(1) defines qualified energy resources as wind, closed-loop biomass, open-loop biomass, geothermal energy, municipal solid waste, qualified hydropower production, and marine and hydrokinetic renewable energy.

Section 45(d)(1) defines a qualified facility using wind to produce electricity as any facility owned by the taxpayer that is originally placed in service after December 31, 1993, and the construction of which begins before January 1, 2022. See section 45(e)(7) for rules relating to the inapplicability of the credit to electricity sold to utilities under certain contracts.

Section 45(d)(2)(A) defines a qualified facility using closed-loop biomass to produce electricity as any facility (i) owned by the taxpayer that is originally placed in service after December 31, 1992, and the construction of which begins before January 1, 2022, or (ii) owned by the taxpayer which before January 1, 2022 is originally placed in service and modified to use closed-loop biomass to co-fire with coal, with other biomass, or with both, but only if the modification is approved under the Biomass Power for Rural Development Programs or is part of a pilot project of the Commodity Credit Corporation as described in 65 FR 63052. For purposes of section 45(d)(2)(A)(ii), a facility shall be treated as modified before January 1, 2022, if the construction of such modification begins before such date. Section 45(d)(2)(C) provides that in the case of a qualified facility described in section 45(d)(2)(A)(ii), (i) the 10-year period referred to in section 45(a) is treated as beginning no earlier than the date of the enactment of section 45(d)(2)(C)(i) (October 22, 2004), and (ii) if the owner of such facility is not the producer of the electricity, the person eligible for the credit allowable under section 45(a) is the lessee or the operator of such facility. A qualified facility using closed-loop biomass includes a new unit placed in service after the date of the enactment of section 45(d)(2)(B) (October 3, 2008) in connection with a qualified facility using closed-loop biomass, but only to the extent of the increased amount of electricity produced at the facility by reason of such new unit.

Section 45(d)(3)(A) defines a qualified facility using open-loop biomass to produce electricity as any facility owned by the taxpayer which (i) in the case of a facility using agricultural livestock waste nutrients, (I) is originally placed in service after the date of the enactment of section 45(d)(3)(A)(i)(I) (October 22, 2004) and the construction of which begins before January 1, 2022, and (II) the nameplate capacity rating of which is not less than 150 kilowatts, and (ii) in the case of any other facility, the construction of which begins before January 1, 2022. In the case of any facility described in section 45(d)(3)(A), if the owner of such facility is not the producer of the electricity, section 45(d)(3)(C) provides that the person eligible for the credit allowable under section 45(a) is the lessee or the operator of such facility. A qualified facility using open-loop biomass includes a new unit placed in service after the date of the enactment of section 45(d)(3)(B) (October 3, 2008) in connection with a qualified facility using open-loop biomass, but only to the extent of the increased amount of electricity produced at the facility by reason of such new unit.

Section 45(d)(4) defines a qualified facility using geothermal energy to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(4) (October 22, 2004) and the construction of which begins before January 1, 2022. A qualified facility using geothermal energy does not include any property described in section 48(a)(3) the basis of which is taken into account by the taxpayer for purposes of determining the energy credit under section 48.

Section 45(d)(6) defines a qualified facility using gas derived from the biodegradation of municipal solid waste to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(6) (October 22, 2004) and the construction of which begins before January 1, 2022.

Section 45(d)(7) defines a qualified facility (other than a facility described in section 45(d)(6)) that uses municipal solid waste to produce electricity as any facility owned by the taxpayer that is originally placed in service after the date of the enactment of section 45(d)(7) (October 22, 2004) and the construction of which begins before January 1, 2022. A qualified facility using municipal solid waste includes a new unit placed in service in connection with a facility placed in service on or before the date of the enactment of section 45(d)(7), but only to the extent of the increased amount of electricity produced at the facility by reason of such new unit.

Section 45(d)(9) defines a qualified facility producing qualified hydroelectric production described in section 45(c)(8) as (i) any facility producing incremental hydropower production, but only to the extent of its incremental hydropower production attributable to efficiency improvements or additions to capacity described in section 45(c)(8)(B) placed in service after the date of the enactment of section 45(d)(9) (August 8, 2005) and before January 1, 2022, and (ii) any other facility placed in service after the date of the enactment of section 45(d)(9) (August 8, 2005) and the construction of which begins before January 1, 2022. Section 45(d)(9)(B) provides that, in the case of a qualified facility described in section 45(d)(9)(A), the 10-year period referred to in section 45(a) shall be treated as beginning on the date the efficiency improvements or additions to capacity are placed in service. Section 45(d)(9)(C) provides that for purposes of section 45(d)(9)(A)(i), an efficiency improvement or addition to capacity shall be treated as placed in service before January 1, 2022 if the construction of such improvement or addition begins before such date.

Section 45(d)(11) provides in the case of a facility producing electricity from marine and hydrokinetic renewable energy, the term “qualified facility” means any facility owned by the taxpayer which (A) has a nameplate capacity rating of at least 150 kilowatts, and (B) is originally placed in service on or after the date of the enactment of section 45(d)(11) (October 3, 2008) and the construction of which begins before January 1, 2022.

Section 45(e)(2)(A) requires the Secretary to determine and publish in the Federal Register each calendar year the inflation adjustment factor and the reference price for such calendar year. The inflation adjustment factor and the reference price for the 2022 calendar year were published in the Federal Register at 87 FR 22286 on April 14, 2022. A Correction notice was published in the Federal Register at 87 FR 27204 on May 6, 2022.

Section 45(e)(2)(B) defines the inflation adjustment factor for a calendar year as a fraction the numerator of which is the GDP implicit price deflator for the preceding calendar year and the denominator of which is the GDP implicit price deflator for the calendar year 1992. The term “GDP implicit price deflator” means the most recent revision of the implicit price deflator for the gross domestic product as computed and published by the Department of Commerce before March 15 of the calendar year.

Section 45(e)(2)(C) provides that the reference price is the Secretary’s determination of the annual average contract price per kilowatt hour of electricity generated from the same qualified energy resource and sold in the previous year in the United States. Only contracts entered into after December 31, 1989 are taken into account.

The inflation adjustment factor for calendar year 2022 for qualified energy resources is 1.7593.

The reference price for calendar year 2022 for facilities producing electricity from wind (based upon information provided by the Department of Energy) is 4.09 cents per kilowatt hour. The reference prices for facilities producing electricity from closed-loop biomass, open-loop biomass, geothermal energy, municipal solid waste, qualified hydropower production, and marine and hydrokinetic energy have not been determined for calendar year 2022.

Because the 2022 reference price for electricity produced from wind (4.09 cents per kilowatt hour) does not exceed 8 cents multiplied by the inflation adjustment factor (1.7593), the phaseout of the credit provided in section 45(b)(1) does not apply to such electricity sold during calendar year 2022. However, refer to section 45(b)(5) for an additional phaseout of the credit for wind facilities the construction of which begins after December 31, 2016. For electricity produced from closed-loop biomass, open-loop biomass, geothermal energy, municipal solid waste, qualified hydropower production, and marine and hydrokinetic energy, the phaseout of the credit provided in section 45(b)(1) does not apply to such electricity sold during calendar year 2022.

As required by section 45(b)(2), the 1.5 cent amount in section 45(a)(1) is adjusted by multiplying such amount by the inflation adjustment factor for the calendar year in which the sale occurs. If any amount as increased under the preceding sentence is not a multiple of 0.1 cent, such amount is rounded to the nearest multiple of 0.1 cent. In the case of electricity produced in open-loop biomass facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic renewable energy facilities, section 45(b)(4)(A) requires the amount in effect under section 45(a)(1) (before rounding to the nearest 0.1 cent) to be reduced by one-half. Under the calculation required by section 45(b)(2), the credit for renewable electricity production for calendar year 2022 under section 45(a) is 2.6 cents per kilowatt hour on the sale of electricity produced from the qualified energy resources of wind, closed-loop biomass, and geothermal energy, and 1.3 cents per kilowatt hour on the sale of electricity produced in open-loop biomass facilities, landfill gas facilities, trash facilities, qualified hydropower facilities, and marine and hydrokinetic energy facilities.

This notice announces the applicable percentage under § 613A of the Internal Revenue Code to be used in determining percentage depletion for marginal properties for the 2022 calendar year.

Section 613A(c)(6)(C) defines the term “applicable percentage” for purposes of determining percentage depletion for oil and gas produced from marginal properties. The applicable percentage is the percentage (not greater than 25 percent) equal to the sum of 15 percent, plus one percentage point for each whole dollar by which $20 exceeds the reference price (determined under § 45K(d)(2)(C)) for crude oil for the calendar year preceding the calendar year in which the taxable year begins. The reference price determined under § 45K(d)(2)(C) for the 2021 calendar year is $65.90.

The following table contains the applicable percentages for marginal production for taxable years beginning in calendar years 1991 through 2022.

Notice 2022-24 APPLICABLE PERCENTAGE FOR MARGINAL PRODUCTION

| Calendar Year | Applicable Percentage |

|---|---|

| 1991 | 15 percent |

| 1992 | 18 percent |

| 1993 | 19 percent |

| 1994 | 20 percent |

| 1995 | 21 percent |

| 1996 | 20 percent |

| 1997 | 16 percent |

| 1998 | 17 percent |

| 1999 | 24 percent |

| 2000 | 19 percent |

| 2001 | 15 percent |

| 2002 | 15 percent |

| 2003 | 15 percent |

| 2004 | 15 percent |

| 2005 | 15 percent |

| 2006 | 15 percent |

| 2007 | 15 percent |

| 2008 | 15 percent |

| 2009 | 15 percent |

| 2010 | 15 percent |

| 2011 | 15 percent |

| 2012 | 15 percent |

| 2013 | 15 percent |

| 2014 | 15 percent |

| 2015 | 15 percent |

| 2016 | 15 percent |

| 2017 | 15 percent |

| 2018 | 15 percent |

| 2019 | 15 percent |

| 2020 | 15 percent |

| 2021 | 15 percent |

| 2022 | 15 percent |

The principal author of this notice is Elimelech Brander of the Office of Associate Chief Counsel (Passthroughs and Special Industries). For further information regarding this notice contact Mr. Brander at (202) 317-6853 (not a toll-free number).

.01 This revenue procedure provides simplified procedures for certain bona fide residents of the Commonwealth of Puerto Rico (Puerto Rico) to claim the child tax credit under § 24.1 The Department of the Treasury and the Internal Revenue Service (IRS) have provided these procedures to make it easier for certain bona fide residents of Puerto Rico to file taxable year 2021 Federal tax returns to claim the child tax credit.

.02 Section 2 of this revenue procedure describes the child tax credit in further detail. Section 3 of this revenue procedure describes the scope of the procedures provided in this revenue procedure. Section 4 of this revenue procedure provides a simplified procedure for filing Form 1040-PR, Planilla para la Declaración de la Contribución Federal sobre el Trabajo por Cuenta Propia, or Form 1040-SS, U.S. Self-Employment Tax Return, to claim the child tax credit. Section 5 of this revenue procedure provides a simplified procedure for filing Form 1040, U.S. Individual Income Tax Return (also available as Formulario 1040(SP), Declaración de Impuestos de los Estados Unidos Sobre los Ingresos Personales), or Form 1040-SR, U.S. Tax Return for Seniors (also available as Formulario 1040-SR(SP), Declaración de Impuestos de los Estados Unidos para Personas de 65 Años de Edad o Más), to claim the child tax credit.

.01 Overview of 2021 Child Tax Credit. Section 9611 of the American Rescue Plan Act of 2021 (American Rescue Plan), Public Law 117-2, 135 Stat. 4, 144-149 (March 11, 2021), added §§ 24(i), 24(j), and 7527A to the Code. Section 24(i) modifies the child tax credit rules set forth in § 24 for any taxable year beginning after December 31, 2020, and before January 1, 2022 (taxable year 2021). Section 7527A provides for advance payments of the child tax credit and section 24(j) provides that the amount of the child tax credit is generally reduced by these advance payments. Section 9612(a) of the American Rescue Plan added § 24(k) to the Code to provide special rules for American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands (each, a U.S. territory), effective for taxable years beginning after December 31, 2020. 135 Stat. at 150-152.

.02 Credit Allowed. Under § 24(a), a taxpayer may claim a child tax credit against the taxpayer’s Federal income tax (as imposed by chapter 1 of the Code) for the taxable year with respect to each CTC qualifying child (as defined in section 2.06 of this revenue procedure) of the taxpayer.

.03 Expanded Credit Eligibility for Bona Fide Residents of Puerto Rico. Starting in 2021, a bona fide resident of Puerto Rico with one or more CTC qualifying children may claim the child tax credit. See §§ 24(i)(1) and 24(k)(2). Prior to enactment of the American Rescue Plan, § 24(d)(1)(B) required bona fide residents of Puerto Rico who had no earned income for Federal income tax purposes to have at least three CTC qualifying children as a condition for child tax credit eligibility.

.04 Credit Fully Refundable. The child tax credit for taxable year 2021 is fully refundable for a taxpayer if the taxpayer (or spouse, if filing a joint return) is a bona fide resident of Puerto Rico (within the meaning of § 937(a)) for such taxable year. See § 24(i)(1). Full refundability means that taxpayers can benefit from the maximum amount of the credit even if they do not have taxable earned income or do not owe any Federal tax for taxable year 2021. Bona fide residents of Puerto Rico may claim the fully refundable child tax credit for taxable year 2021 even if they had no income and paid no U.S. Social Security taxes.

.05 Credit Amounts. Taxpayers claiming the child tax credit for taxable year 2021 may receive up to $3,000 for each CTC qualifying child who is between the ages of 6 and 17 as of the end of taxable year 2021, and $3,600 for each CTC qualifying child who is under the age of 6 as of the end of taxable year 2021. See § 24(i)(2) and (3). The child tax credit for taxable year 2021 begins to be reduced if modified adjusted gross income (AGI) for purposes of the child tax credit exceeds $150,000 if filing a joint return or if filing as a surviving spouse (as defined in § 2(a) of the Code); $112,500 if filing as head of household (as defined in § 2(b)); or $75,000 if filing as single or married and filing a separate return. See § 24(i)(4).

.06 CTC Qualifying Child. A “CTC qualifying child” is a qualifying child of the taxpayer (as defined in § 152(c)) who has not attained the age of 18 at the close of taxable year 2021. See § 24(i)(2)(A). No child tax credit is allowed for a qualifying child unless the social security number (SSN) of the child, which must be valid for employment and be issued by the Social Security Administration before the due date of the taxpayer’s taxable year Federal income tax return (including extensions), is provided on the return. See § 24(h)(7). If the taxpayer’s child was a U.S. citizen when the child received the SSN, the SSN is valid for employment.

.07 Advance Child Tax Credit Payments for Calendar Year 2021. Section 7527A(a) required the Secretary of the Treasury or her delegate to establish a program for making periodic advance child tax credit payments to taxpayers the total of which, during any calendar year, equals the “annual advance amount” (as defined in § 7527A(b)(1)) determined with respect to that taxpayer for that calendar year. Although residents of Puerto Rico may be eligible to claim the child tax credit, residents of Puerto Rico were not eligible to receive advance child tax credit payments. See § 7527A(e)(4)(A). However, there may have been circumstances in which a resident of Puerto Rico nonetheless received advance child tax credit payments (for example, if the IRS estimated the Puerto Rico resident’s child tax credit for taxable year 2021 based on a Form 1040 or Form 1040-SR that the resident filed for taxable year 2019 or 2020).

.08 Reconciliation Requirement Regarding Child Tax Credit and Advance Child Tax Credit Payments. Bona fide residents of Puerto Rico who received advance child tax credit payments (described in section 2.07 of this revenue procedure) during calendar year 2021 must reduce (but not below zero) the amount of the child tax credit claimed for taxable year 2021 by the total amount of those advance child tax credit payments. See § 24(j)(1). If the amount of the taxpayer’s advance child tax credit payments received in calendar year 2021 exceeds the taxpayer’s allowable child tax credit for taxable year 2021, the taxpayer’s Federal income tax imposed for taxable year 2021 will be increased by the excess subject to reduction by a “safe harbor amount.” See § 24(j)(2).

.01 Overview. This revenue procedure allows Puerto Rico CTC filers (as defined in section 4.02 of this revenue procedure) to provide information to the IRS to claim the child tax credit through the filing of a simplified Federal tax return using either of the following procedures: (1) the procedures set forth in section 4 of this revenue procedure, which allow Puerto Rico CTC filers to provide this information through a simplified Form 1040-PR or Form 1040-SS or (2) the procedures set forth in section 5 of this revenue procedure, which allow Puerto Rico CTC filers to provide this information through a simplified Form 1040 or Form 1040-SR.

.02 Purpose of Simplified Filing Procedure under Section 4. Section 4 of this revenue procedure provides a simplified filing procedure that permits Puerto Rico CTC filers to file a Form 1040-PR or Form 1040-SS to claim the child tax credit. Specifically, Puerto Rico CTC filers who file a simplified Form 1040-PR or Form 1040-SS for taxable year 2021 in accordance with section 4 of this revenue procedure do not need to specify their income to compute the amount of child tax credit that they are eligible to claim.

.03 Purpose of Simplified Filing Procedure under Section 5. Section 5 of this revenue procedure provides a simplified filing procedure that permits Puerto Rico CTC filers to file a Form 1040 or Form 1040-SR to claim the child tax credit. Specifically, Puerto Rico CTC filers who file a simplified Form 1040 or Form 1040-SR for taxable year 2021 in accordance with section 5 of this revenue procedure do not need to specify their income to compute the amount of child tax credit that they are eligible to claim.

.04 Individuals Who Are Not Puerto Rico Residents Are Not Eligible. The procedures provided by this revenue procedure apply only to a U.S. citizen or U.S. resident alien who is a bona fide resident of Puerto Rico and who is not described in section 3.05, 3.06, 3.07, or 3.08 of this revenue procedure. The procedures provided by this revenue procedure do not apply to a resident of any U.S. territory (as defined in section 2.01 of this revenue procedure) other than Puerto Rico, or to a U.S. citizen or U.S. resident who is not a resident of a U.S. territory. Residents of a U.S. territory should contact their local territory tax agency for additional information about the child tax credit. A U.S. citizen or U.S. resident who is not a resident of a U.S. territory should refer to Form 1040 or Form 1040-SR, Schedule 8812 (Form 1040), Credits for Qualifying Children and Other Dependents, and their instructions, to claim the child tax credit for taxable year 2021. A U.S. citizen or U.S. resident alien who is not a bona fide resident of Puerto Rico or a resident of a U.S. territory may qualify to use the simplified filing procedures set forth in Rev. Proc. 2022-12, 2022-7 I.R.B. 494. See section 4.02(1) and (6) of this revenue procedure.

.05 Individuals Required to File a Form 1040-PR, Form 1040-SS, Form 1040, or Form 1040-SR Not Eligible. The procedures provided by this revenue procedure do not apply to individuals who are required to file a Form 1040-PR, Form 1040-SS, Form 1040, or Form 1040-SR for taxable year 2021 (including bona fide residents of Puerto Rico who are required to report tax on their self-employment income). See section 4.02(2) and (3) of this revenue procedure.

.06 Individuals With Modified AGI Above Applicable Income Thresholds Not Eligible. The procedures provided by this revenue procedure do not apply to individuals whose modified AGI for purposes of the child tax credit exceeds the applicable income threshold for claiming the maximum child tax credit amount as described in section 2.05 of this revenue procedure. That is, the procedures do not apply to individuals whose modified AGI exceeds (i) $150,000, if filing a joint return or filing as a surviving spouse; (ii) $112,500, if filing as head of household; and (iii) $75,000, if filing as single or married and filing a separate return. The amount of income of an individual with modified AGI at or below their applicable threshold will not impact the amount of the child tax credit that the individual is eligible to claim. See section 4.02(4) of this revenue procedure.

.07 Individuals Who Received Excess Advance Child Tax Credit Payments Not Eligible. The procedures provided by this revenue procedure apply to individuals who need to file a Federal income tax return to claim the child tax credit in an amount greater than zero for taxable year 2021. Individuals who received advance child tax credit payments during calendar year 2021, the total amount of which equals or exceeds the individual’s allowable child tax credit for taxable year 2021, cannot claim the child tax credit in an amount greater than zero for taxable year 2021. Accordingly, the procedures provided by this revenue procedure do not apply to such individuals, and they cannot file a Federal tax return under this revenue procedure. See section 4.02(5) of this revenue procedure.

.08 Individuals Who Previously Filed a Form 1040-PR, Form 1040-SS, Form 1040, or Form 1040-SR Not Eligible. The procedures provided by this revenue procedure do not apply to individuals who have already filed a paper or electronic Form 1040-PR, Form 1040-SS, Form 1040, or Form 1040-SR for taxable year 2021. Such individuals do not need to file any additional forms or otherwise contact the IRS to claim the child tax credit for each CTC qualifying child if the child tax credit was claimed on the previously filed return for taxable year 2021. See section 4.02(7) of this revenue procedure.

.01 Federal Tax Return Claiming the Child Tax Credit. Under the simplified procedure set forth in this section 4, a simplified return may be filed, on paper or electronically, for taxable year 2021 on a Form 1040-PR or Form 1040-SS. A Federal tax return for taxable year 2021 filed by a Puerto Rico CTC filer under the simplified procedure in this section 4 will result in the Puerto Rico CTC filer claiming the child tax credit for taxable year 2021.

.02 Definition of Puerto Rico CTC Filer. For purposes of this revenue procedure, a “Puerto Rico CTC filer” is an individual--

(1) Who is a bona fide resident of Puerto Rico (within the meaning of § 937(a) for taxable year 2021);

(2) Whose income for taxable year 2021 is completely exempt from taxation under § 933;

(3) Who is not required to file a Form 1040-PR, Form 1040-SS, Form 1040, or Form 1040-SR for taxable year 2021, such as to report tax on self-employment income;

(4) Whose modified AGI for taxable year 2021 under § 24(b)(1) is less than or equal to their applicable income threshold under § 24(i)(4)(B);

(5) Who is eligible to claim the child tax credit in an amount greater than zero for taxable year 2021;

(6) Who is a U.S. citizen or resident alien (or is treated as a United States resident alien in accordance with an election under § 6013(g) or (h)); and

(7) Who has not already filed a paper or electronic Form 1040-PR, Form 1040-SS, Form 1040, or Form 1040-SR for taxable year 2021.

.03 Simplified Filing Method.

(1) Overview. In the case of a Puerto Rico CTC filer, the IRS will process the filer’s Form 1040-PR or Form 1040-SS for taxable year 2021 to calculate the child tax credit if the form is prepared in the manner required by this section 4.03. The Form 1040-PR or Form 1040-SS must include the information described in this section 4.03 to claim the child tax credit. The information described in this section 4.03 generally follows the standard IRS instructions except that a Puerto Rico CTC filer is not required to report the filer’s modified AGI on line 1 of Part II. A Puerto Rico CTC filer may file a Schedule LEP (Form 1040), Request for Change in Language Preference (also available as Anexo LEP (Formulario 1040(SP)), Solicitud para Cambiar la Preferencia de Idioma), with Form 1040-PR or Form 1040-SS to request a change in language preference for further communications from the IRS.

(2) Personal information. A Puerto Rico CTC filer must enter their name, mailing address, and SSN or IRS Individual Taxpayer Identification Number (ITIN), and the name and SSN or ITIN of their spouse if filing a joint return, at the top of Form 1040-PR or Form 1040-SS.

(3) Virtual currency. A Puerto Rico CTC filer must check the appropriate box indicating whether the filer (either filer if filing a joint return) received, sold, exchanged, or otherwise disposed of a financial interest in any virtual currency.

(4) Part I, line 1 (filing status). A Puerto Rico CTC filer must select their filing status for taxable year 2021 on line 1 of Part I.

(5) Part I, line 2 (CTC qualifying children). A Puerto Rico CTC filer must complete the appropriate lines on line 2 of Part I regarding each CTC qualifying child for taxable year 2021 who has an SSN that is valid for employment. For each individual claimed as a CTC qualifying child, the Puerto Rico CTC filer must provide the name, SSN, and relationship to the individual.

(6) Part I, lines 3 through 8. A Puerto Rico CTC filer must leave lines 3 through 8 of Part I blank.

(7) Part I, line 9 (child tax credit entry). A Puerto Rico CTC filer must complete line 9 of Part I. To determine this amount, the Puerto Rico CTC filer must:

(a) Compute the sum of the following:

(i) $3,600 multiplied by the number of CTC qualifying children of the filer listed on line 2 of Part I who were under age 6 at the end of taxable year 2021; and

(ii) $3,000 multiplied by the number of CTC qualifying children of the filer listed on line 2 of Part I who were under age 18 at the end of taxable year 2021 but who were not under age 6 at the end of taxable year 2021;

(b) Subtract from that sum the aggregate amount of advance child tax credit payments the filer (and the filer’s spouse if filing jointly) received for 2021, if any, which may be obtained from the filer’s Letter 6419 or the filer’s IRS online account at https://www.irs.gov/account and, as applicable, Letter 6419 of the filer’s spouse or the IRS online account of the filer’s spouse; and

(c) Enter that result on line 9 of Part I.

(8) Part I, lines 10 through 11b. A Puerto Rico CTC filer must leave lines 10 through 11b of Part I blank.

(9) Part I, lines 12 through 14a. A Puerto Rico CTC filer must enter on lines 12 through 14a of Part I the amount entered on line 9 of Part I.

(10) Part I, line 14a checkbox (split direct deposit indicator). A Puerto Rico CTC filer may not check the box on line 14a of Part I.

(11) Part I, lines 14b through 14d (direct deposit information). A Puerto Rico CTC filer may request the direct deposit of their taxable year 2021 tax refund into an account at a bank or other financial institution by entering the information on lines 14b through 14d of Part I. The Puerto Rico CTC filer must not request that their taxable year 2021 tax refund be deposited into an account that is not in the name of that filer (for example, a Puerto Rico CTC filer must not request a direct deposit of their taxable year 2021 tax refund into their tax return preparer’s account).

(12) Part I, lines 15 and 16. A Puerto Rico CTC filer must leave lines 15 and 16 of Part I blank.

(13) Part II, line 1 (modified adjusted gross income). A Puerto Rico CTC filer must leave line 1 of Part II blank.

(14) Part II, line 3 (refundable child tax credit). A Puerto Rico CTC filer must enter on line 3 of Part II the amount entered on line 9 of Part I.

(15) Parts III through VI. A Puerto Rico CTC filer must leave Parts III through VI blank.

(16) Signature. A Puerto Rico CTC filer must sign the return under penalties of perjury, including the filer’s identity protection personal identification number (that is, the filer’s IP PIN), if applicable, as part of the filer’s signature. In addition, the Puerto Rico CTC filer may enter the identifying information of any third-party designee, if applicable, at the bottom of page 1 of Form 1040-PR or Form 1040-SS. A Puerto Rico CTC filer who has been assigned an IP PIN, but has misplaced it, may retrieve the IP PIN at https://www.irs.gov/identity-theft-fraud-scams/retrieve-your-ip-pin.

.04 Simplified Return Is a Federal Tax Return. A simplified return completed by a Puerto Rico CTC filer in accordance with the procedure described in section 4.03 of this revenue procedure is a taxable year 2021 Federal tax return for all purposes, whether filed on paper or electronically.

.01 Federal Tax Return Claiming the Child Tax Credit. Under the simplified procedure set forth in this section 5, a simplified return may be filed, on paper or electronically, for taxable year 2021 on a Form 1040 or Form 1040-SR. A Federal tax return for taxable year 2021 filed by a Puerto Rico CTC filer under the simplified procedure in this section 5 will result in the Puerto Rico CTC filer claiming the child tax credit for taxable year 2021.

.02 Definition of Puerto Rico CTC Filer. For purposes of this section 5, a “Puerto Rico CTC filer” has the same definition as in section 4.02 of this revenue procedure.

.03 Simplified Filing Method.

(1) Overview. In the case of a Puerto Rico CTC filer, the IRS will process the filer’s Form 1040 or Form 1040-SR for taxable year 2021 to calculate the child tax credit for taxable year 2021 if the form is prepared in the manner required by this section 5.03. The Form 1040 or Form 1040-SR must include the information described in this section 5.03 to claim the child tax credit. The information described in this section 5.03 generally follows the standard IRS instructions for filers whose income is completely exempt from taxation under § 933 except that a Puerto Rico CTC filer is not required to report the filer’s modified AGI on lines 1 through 3 of Schedule 8812 (Form 1040). A Puerto Rico CTC filer may file a Schedule LEP (Form 1040) with Form 1040 or Form 1040-SR to request a change in language preference for further communications from the IRS.

(2) Required general information on Form 1040 or Form 1040-SR.

(a) Filing status. A Puerto Rico CTC filer must select their filing status for taxable year 2021 at the top of Form 1040 or Form 1040-SR.

(b) Personal information. A Puerto Rico CTC filer must enter their name, mailing address, and SSN or ITIN, and the name and SSN or ITIN of their spouse if filing a joint return, on the appropriate lines of Form 1040 or Form 1040-SR.

(3) Virtual currency. A Puerto Rico CTC filer must check the appropriate box on Form 1040 or Form 1040-SR indicating whether the filer (either filer if filing a joint return) received, sold, exchanged, or otherwise disposed of a financial interest in any virtual currency.

(4) Individuals who could be claimed as dependents by other individuals. A Puerto Rico CTC filer must check the applicable boxes in the top line of the “Standard Deduction” section of the Form 1040 or Form 1040-SR for each individual who can be claimed as a dependent by any other individual for taxable year 2021.

(5) General information regarding dependents.

(a) In general. A Puerto Rico CTC filer must complete the appropriate lines in the “Dependents” section of Form 1040 or Form 1040-SR regarding each CTC qualifying child for taxable year 2021 who has an SSN that is valid for employment. For each individual claimed as a CTC qualifying child, the Puerto Rico CTC filer must provide the name, SSN, and relationship to the individual.

(b) CTC qualifying children. A Puerto Rico CTC filer must check the child tax credit box in Column (4) of the “Dependents” section for each CTC qualifying child for taxable year 2021 who has an SSN that is valid for employment.

(6) Limited information to provide in Form 1040 or Form 1040-SR, lines 1 through 38. A Puerto Rico CTC filer must leave blank lines 1 through 38 of Form 1040 or Form 1040-SR, except as provided in this section 5.03(6):

(a) Line 28 (child tax credit entry). A Puerto Rico CTC filer must enter the amount of the filer’s child tax credit for taxable year 2021 on line 28. The credit amount may be computed using Schedule 8812 (Form 1040), available at https://www.irs.gov/Schedule8812 (also available as Anexo 8812 (Formulario 1040(SP)), Créditos por Hijos Calificados y Otros Dependientes, at https://www.irs.gov/Schedule8812SP), and information from the filer’s Letter 6419 or the filer’s IRS online account at https://www.irs.gov/account and, as applicable, Letter 6419 of the filer’s spouse or the IRS online account of the filer’s spouse. The filer claiming the child tax credit must (i) complete Schedule 8812 pursuant to the instructions described in section 5.03(8) through (22) of this revenue procedure, and (ii) attach the Schedule 8812 to the filer’s Form 1040 or Form 1040-SR.

(b) Lines 32 through 35a. A Puerto Rico CTC filer must enter on lines 32 through 35a the amount entered on line 28.

(c) Line 35a checkbox (split direct deposit indicator). A Puerto Rico CTC filer may not check the box on line 35a.

(d) Lines 35b through 35d (direct deposit information). A Puerto Rico CTC filer may request the direct deposit of their taxable year 2021 tax refund into an account at a bank or other financial institution by entering the information on lines 35b through 35d. The Puerto Rico CTC filer must not request that their taxable year 2021 tax refund be deposited into an account that is not in the name of that filer (for example, a Puerto Rico CTC filer must not request a direct deposit of their taxable year 2021 tax refund into their tax return preparer’s account).

(7) Signature. A Puerto Rico CTC filer must sign the Form 1040 or Form 1040-SR under penalties of perjury, including the filer’s identity protection personal identification number (that is, the filer’s IP PIN), if applicable, as part of the filer’s signature. In addition, the Puerto Rico CTC filer may enter the identifying information of any third-party designee, if applicable, at the bottom of page 2 of Form 1040 or Form 1040-SR. A Puerto Rico CTC filer who has been assigned an IP PIN, but has misplaced it, may retrieve the IP PIN at https://www.irs.gov/identity-theft-fraud-scams/retrieve-your-ip-pin.

(8) Schedule 8812. A Puerto Rico CTC filer must enter the filer’s name and SSN and the name of their spouse if filing a joint return at the top of Schedule 8812.

(9) Schedule 8812, Part I-A, lines 1 through 3 (modified AGI). A Puerto Rico CTC filer must leave lines 1 through 3 of Schedule 8812 (Form 1040) blank.

(10) Schedule 8812, Part I-A, lines 4a-c (CTC qualifying children). A Puerto Rico CTC filer must complete lines 4a, 4b and 4c.

(11) Schedule 8812, Part I-A, line 5 (child tax credit). A Puerto Rico CTC filer must complete line 5. In completing line 5, the Puerto Rico CTC filer must provide the sum of the following:

(a) $3,600 multiplied by the number entered on line 4b; and

(b) $3,000 multiplied by the number entered on line 4c.

(12) Schedule 8812, Part I-A, line 6 (credit for other dependents) and line 7. A Puerto Rico CTC filer must leave lines 6 and 7 blank.

(13) Schedule 8812, Part I-A, line 8. A Puerto Rico CTC filer must enter on line 8 the amount entered on line 5.

(14) Schedule 8812, Part I-A, line 9: A Puerto Rico CTC filer must enter on line 9 $200,000 (or $400,000 if married and filing a joint return).

(15) Schedule 8812, Part I-A, lines 10 and 11. A Puerto Rico CTC filer must leave lines 10 and 11 blank.

(16) Schedule 8812, Part I-A, line 12. A Puerto Rico CTC filer must enter on line 12 the amount entered on line 5.

(17) Schedule 8812, Part I-A, line 13. A Puerto Rico CTC filer must check only the box on line 13B.

(18) Schedule 8812, Part I-B, line 14a. A Puerto Rico CTC filer must leave line 14a blank.

(19) Schedule 8812, Part I-B, line 14b. A Puerto Rico CTC filer must enter on line 14b the amount entered on line 5.

(20) Schedule 8812, Part I-B, lines 14c and 14d. A Puerto Rico CTC filer must leave lines 14c and 14d blank.

(21) Schedule 8812, Part I-B, line 14e. A Puerto Rico CTC filer must enter on line 14e the amount entered on line 5.

(22) Schedule 8812, Part I-B, line 14f (advance child tax credit payments received). A Puerto Rico CTC filer must enter on line 14f the aggregate amount of advance child tax credit payments the filer (and the filer’s spouse if filing jointly) received for 2021, which may be obtained from the filer’s Letter 6419 or the filer’s IRS online account at https://www.irs.gov/account and, as applicable, Letter 6419 of the filer’s spouse or the IRS online account of the filer’s spouse.

(23) Schedule 8812, Part I-B, line 14g (allowable child tax credit). A Puerto Rico CTC filer must complete line 14g. To determine this amount, the Puerto Rico CTC filer must:

(a) Subtract the amount entered on line 14f from the amount entered on line 14e (that is, the filer must subtract the aggregate amount of advance child tax credit payments that the filer received in 2021, if any, from the amount of child tax credit for which the filer is eligible); and

(b) Enter that result (that is, the allowable child tax credit) on line 14g.

(24) Schedule 8812, Part I-B, line 14h. A Puerto Rico CTC filer must leave line 14h blank.

(25) Schedule 8812, Part I-B, line 14i (refundable child tax credit). A Puerto Rico CTC filer must enter on line 14i the amount entered on line 14g.

(26) Schedule 8812, Parts I-C through III, lines 15a through 50. A Puerto Rico CTC filer must leave lines 15a through 50 blank.

.04 Simplified Return Is a Federal Tax Return. A simplified return completed by a Puerto Rico CTC filer in accordance with the procedure described in section 5.03 of this revenue procedure is a taxable year 2021 Federal tax return for all purposes, whether filed on paper or electronically.

This revenue procedure applies to Federal tax returns filed after May 6, 2022.

.01 Child Tax Credit and Advance Child Tax Credit Payments. Individuals can obtain additional information regarding advance child tax credit payments and the child tax credit for taxable year 2021 through the IRS child tax credit and advance child tax credit payment webpage at https://www.irs.gov/childtaxcredit2021.

.02 Completing a Federal Tax Return. Bona fide residents of Puerto Rico can obtain additional information regarding how to complete their Federal tax returns at https://www.irs.gov/Form1040PR (in Spanish); https://www.irs.gov/Form1040SS; https://www.irs.gov/Form1040SP (in Spanish); https://www.irs.gov/Form1040; and https://www.irs.gov/Form1040SR.

.03 Obtaining Tax Information in Other Languages. Taxpayers may obtain basic tax information in other languages at https://www.irs.gov/MyLanguage.

AGENCY: Internal Revenue Service (IRS), Treasury.

ACTION: Notice of proposed rulemaking.

SUMMARY: This document contains proposed regulations relating to the use of actuarial tables in valuing annuities, interests for life or a term of years, and remainder or reversionary interests. These regulations will affect the valuation of inter vivos and testamentary transfers of interests dependent on one or more measuring lives. These regulations are necessary because applicable law requires the actuarial tables to be updated to reflect the most recent mortality experience available.

DATES: Written or electronic comments and requests for a public hearing must be received by July 5, 2022. Requests for a public hearing must be submitted as prescribed in the “Comments and Requests for a Public Hearing” section.

ADDRESSES: Commenters are strongly encouraged to submit public comments electronically. Submit electronic submissions via the Federal eRulemaking Portal at www.regulations.gov (indicate IRS and REG-122770-18) by following the online instructions for submitting comments. Once submitted to the Federal eRulemaking Portal, comments cannot be edited or withdrawn. The IRS expects to have limited personnel available to process public comments that are submitted on paper through mail. Until further notice, any comments submitted on paper will be considered to the extent practicable. The Department of the Treasury (Treasury Department) and the IRS will publish for public availability any comment submitted electronically, and to the extent practicable on paper, to its public docket. Send paper submissions to: CC:PA:LPD:PR (REG-122770-18), room 5203, Internal Revenue Service, PO Box 7604, Ben Franklin Station, Washington, D.C. 20044.

FOR FURTHER INFORMATION CONTACT: Concerning the proposed regulations, Mayer R. Samuels of the Office of Associate Chief Counsel (Passthroughs and Special Industries), (202) 317-6859; concerning the submission of comments or requests for a public hearing, Regina L. Johnson, (202) 317-5177 (not toll-free numbers).

SUPPLEMENTARY INFORMATION:

This document contains amendments to the Income Tax Regulations (26 CFR part 1), the Estate Tax Regulations (26 CFR part 20), and the Gift Tax Regulations (26 CFR part 25) to reflect revisions to certain tables used for the valuation of interests in property under section 7520 of the Internal Revenue Code of 1986 (Code) to reflect the most recent mortality experience available.

Section 7520, effective for transfers for which the valuation date is on or after May 1, 1989, generally provides that the value of an annuity, an interest for life or a term of years, and a remainder or reversionary interest is to be determined under tables published by the Secretary of the Treasury or her delegate (Secretary) by using an interest rate (rounded to the nearest two-tenths of one percent) equal to 120 percent of the Federal midterm rate in effect under section 1274(d)(1) for the month in which the valuation date falls. If a charitable contribution is allowable for any part of the property transferred, the taxpayer may elect under section 7520(a) to use such Federal midterm rate for either of the two months preceding the month in which the valuation date falls. Section 7520(c)(2), as it existed on May 1, 1989, directed the Secretary to issue tables not later than December 31, 1989, utilizing the then most recent mortality experience. Thereafter, the Secretary is directed to revise these tables not less frequently than once each 10 years to take into account the most recent mortality experience available as of the time of the revision.

These proposed regulations contain Table 2010CM that is based on data compiled from the 2010 census. For transfers for which the valuation date is on or after the applicability date of the Treasury decision adopting these regulations as final regulations (published as the final rule in the Federal Register), the appropriate actuarial factors based on Table 2010CM may be computed by taxpayers. However, for the convenience of taxpayers, actuarial factors may be found on IRS websites and publications referenced in these proposed regulations. These proposed regulations also make conforming amendments to various sections of the existing regulations to provide the references to these revised actuarial factors. The updated actuarial tables will be available beginning May 5, 2022, at no charge, electronically via the IRS website at https://www.irs.gov/retirement-plans/actuarial-tables. IRS Publications 1457 “Actuarial Valuations Version 4A” (forthcoming 2022), 1458 “Actuarial Valuations Version 4B” (forthcoming 2022), and 1459 “Actuarial Valuations Version 4C” (forthcoming 2022) will provide additional references and explanations to the actuarial tables that are published on the IRS website. These publications will be available after the applicability date of the Treasury decision adopting these regulations as final regulations. Table S (Single Life Remainder Factors) and Table U(1) (Unitrust Single Life Remainder Factors), which are referenced and explained in Publications 1457 and 1458, respectively, will no longer be published in these regulations. Furthermore, the current Table S and Table U(1), effective for transfers for which the valuation date is after April 30, 2009, and before the applicability date of the Treasury decision adopting these regulations as final regulations is published in the Federal Register, will be moved to sections containing actuarial material for historical reference. Table B, Table D, Tables F(0.2) through F(20.0), Table J, and Table K, which are not based on mortality experience, are not changed.

The following chart summarizes the applicable interest rates and the citations to textual materials and tables for the various periods covered under the current regulations. For purposes of this chart, “DPAD” is the day prior to the applicability date of the Treasury decision adopting these regulations as final regulations and “AD” is the applicability date of the Treasury decision adopting these regulations as final regulations.

Cross Reference to Regulation Sections

| Valuation | Interest | Regulation | |

|---|---|---|---|

| Period | Rate | Section | Table |

| Section 642: | |||

| Valuation, in general | - | 1.642(c)-6 | |

| before 01/01/52 | 4% | 1.642(c)-6A(a) | |

| 01/01/52 - 12/31/70 | 3.5% | 1.642(c)-6A(b) | |

| 01/01/71 - 11/30/83 | 6% | 1.642(c)-6A(c) | |

| 12/01/83 - 04/30/89 | 10% | 1.642(c)-6A(d) | Table G |

| 05/01/89 - 04/30/99 | 7520 | 1.642(c)-6A(e) | Table S (5/1/89 - 4/30/99) |

| 05/01/99 - 04/30/09 | 7520 | 1.642(c)-6A(f) | Table S (5/1/99 - 4/30/09) |

| 05/01/09 – DPAD | 7520 | 1.642(c)-6A(g) | Table S (5/1/09- DPAD) |

| on or after AD | 7520 | 1.642(c)-6(e) | Table S (on or after AD) |

| Section 664: | |||

| Valuation, in general | - | 1.664-4 | |

| before 01/01/52 | 4% | 1.664-4A(a) | |

| 01/01/52 - 12/31/70 | 3.5% | 1.664-4A(b) | |

| 01/01/71 - 11/30/83 | 6% | 1.664-4A(c) | |

| 12/01/83 - 04/30/89 | 10% | 1.664-4A(d) | Table E, Table F(1) |

| 05/01/89 - 04/30/99 | 7520 | 1.664-4A(e) | Table U(1) (5/1/89 - 4/30/99) |

| 05/01/99 - 04/30/09 | 7520 | 1.664-4A(f) | Table U(1) (5/1/99 - 4/30/09) |

| 05/01/09 - DPAD | 7520 | 1.664-4A(g) | Table U(1) (5/1/09-DPAD) |

| on or after AD | 7520 | 1.664-4(e) | Table U(1) (on or after AD), Table D, and Table F |

| See Pub. 1458, ver. 4A | |||

| Section 2031: | |||

| Valuation, in general | - | 20.2031-7 | |

| before 01/01/52 | 4% | 20.2031-7A(a) | |

| 01/01/52 - 12/31/70 | 3.5% | 20.2031-7A(b) | |

| 01/01/71 - 11/30/83 | 6% | 20.2031-7A(c) | |

| 12/01/83 - 04/30/89 | 10% | 20.2031-7A(d) | Table A, Table B, Table LN |

| 05/01/89 - 04/30/99 | 7520 | 20.2031-7A(e) | Table S (5/1/89 - 4/30/99) |

| Table 80CNSMT | |||

| 05/01/99 - 04/30/09 | 7520 | 20.2031-7A(f) | Table S (5/1/99 - 4/30/09) |

| Table 90CM | |||

| 05/01/09 - DPAD | 7520 | 20.2031-7A(g) | Table S (5/1/09 - DPAD) |

| Table 2000CM | |||

| on or after AD | 7520 | 20.2031-7(d) | Table S (on or after AD) |

| Table 2010CM | |||

| Table B, Table J, Table K | |||

| see Pub. 1457, ver. 4A | |||

| Section 2512: | |||

| Valuation, in general | - | 25.2512-5 | |

| before 01/01/52 | 4% | 25.2512-5A(a) | |

| 01/01/52 - 12/31/70 | 3.5% | 25.2512-5A(b) | |

| 01/01/71 - 11/30/83 | 6% | 25.2512-5A(c) | |

| 12/01/83 - 04/30/89 | 10% | 25.2512-5A(d) | |

| 05/01/89 - 04/30/99 | 7520 | 25.2512-5A(e) | |

| 05/01/99 - 04/30/09 | 7520 | 25.2512-5A(f) | |

| 05/01/09 - DPAD | 7520 | 25.2512-5A(g) | |

| on or after AD | 7520 | 25.2512-5(d) |

These regulations are proposed to be applicable in the case of annuities, interests for life or a term of years, and remainder or reversionary interests that are valued as of a date on or after the first day of the month following the date on which the Treasury decision adopting these regulations as final regulations is published in the Federal Register.

The regulations provide certain rules to facilitate the transition to the new actuarial tables. For gift tax purposes, if the date of a transfer is on or after January 1, 2021, and before the applicability date of the Treasury decision adopting these regulations as final regulations, the donor may choose to determine the value of the gift (and/or any applicable charitable deduction) under tables based on either Table 2000CM or Table 2010CM. Similarly, for estate tax purposes, if the decedent dies on or after January 1, 2021, and before the applicability date of the Treasury decision adopting these regulations as final regulations, the value of any interest (and/or any applicable charitable deduction) may be determined in the discretion of the decedent’s executor under tables based on either Table 2000CM or Table 2010CM, provided that the decedent’s executor must use the same mortality table to value all interests in the same property. However, the section 7520 interest rate to be utilized is the appropriate rate for the month in which the valuation date occurs, subject to the following special rule for certain charitable transfers. Specifically, in accordance with this transitional rule and the rules contained in §§1.7520-2(a)(2), 20.7520-2(a)(2), and 25.7520-2(a)(2), in cases involving a charitable deduction, if the valuation date occurs on or after January 1, 2021, but before the applicability date of the Treasury decision adopting these regulations as final regulations, and the executor or donor elects under section 7520(a) to use the section 7520 interest rate for a month that is prior to January 1, 2021, then the mortality experience contained in Table 2000CM must be used. If the executor or donor uses the section 7520 interest rate for a month that is on or after January 1, 2021, but before the applicability date of the Treasury decision adopting these regulations as final regulations, then the tables based on either Table 2000CM or Table 2010CM may be used. However, if the valuation date occurs on or after the applicability date of the Treasury decision adopting these regulations as final regulations, the executor or donor must use the new mortality experience contained in Table 2010CM even if the use of a prior month’s interest rate is elected under section 7520(a).

In addition, the regulations no longer will provide that the estate of a decedent who was under a mental disability that prevented a change in the disposition of the decedent’s property may elect to value the property interest included in the gross estate either under the mortality table and interest rate in effect at the time the decedent first became subject to the mental disability or under the mortality table and interest rate in effect on the decedent’s date of death. The taxpayer decedent, during life and before the advent of the mental disability, would not know, beforehand, what the market interest rate would be at his or her future date of death, but can reasonably be expected to have understood that the property interest would be valued at the then-applicable market rate, whatever it might be. Becoming incapacitated should not alter the effect of that understanding. Therefore, a special rule permitting an election to use the interest rate in effect at the time the decedent first became subject to the mental disability is not necessary. The same is true with respect to mortality rates. Accordingly, estates of decedents with a mental disability who die after the applicability date of the Treasury decision adopting these regulations as final regulations will be required to use the mortality table and interest rate in effect on the decedent’s date of death or the alternate valuation date under section 2032, if elected.

These proposed regulations are not subject to review under section 6(b) of Executive Order 12866 pursuant to the Memorandum of Agreement (April 11, 2018) between the Treasury Department and the Office of Management and Budget (OMB) regarding review of tax regulations. Therefore, a regulatory impact assessment is not required.

Pursuant to the Regulatory Flexibility Act (5 U.S.C. chapter 6), it is hereby certified that this proposed rule will not have a significant economic impact on a substantial number of small entities. This document proposes to implement statutorily required periodic updates to actuarial tables used in valuing various interests in property that are affected by a person’s life expectancy. The updates would not impose any direct compliance requirements on any entities other than the time to read and understand the proposed updates. Notwithstanding this certification, the Treasury Department and the IRS invite comment on the impact this proposed rule would have on small entities.

The Treasury Department and the IRS have assessed that the proposed regulations do not establish a new collection of information nor modify an existing collection that requires the approval of the Office of Management and Budget under the Paperwork Reduction Act (44 U.S.C. chapter 35). The Treasury Department and the IRS seek comments on this assessment.

Pursuant to section 7805(f), this notice of proposed rulemaking has been submitted to the Chief Counsel for the Office of Advocacy of the Small Business Administration for comment on its impact on small business.

IRS Revenue Procedures, Revenue Rulings, Notices, and other guidance cited in this preamble are published in the Internal Revenue Bulletin (or Cumulative Bulletin) and are available from the Superintendent of Documents, U.S. Government Publishing Office, Washington, DC 20402, or by visiting the IRS website at https://www.irs.gov.

The Treasury Department and the IRS request comments on all aspects of the proposed rules.

Before these proposed amendments to the regulations are adopted as final regulations, consideration will be given to comments that are submitted timely to the IRS as prescribed in the preamble under the ADDRESSES section. Any electronic comments submitted, and to the extent practicable any paper comments submitted, will be made available at www.regulations.gov or upon request.

A public hearing will be scheduled if requested in writing by any person who timely submits electronic or written comments. Requests for a public hearing also are encouraged to be made electronically. If a public hearing is scheduled, notice of the date and time for the public hearing will be published in the Federal Register. Announcement 2020-4, 2020-17 I.R.B 1, provides that, until further notice, public hearings conducted by the IRS will be held telephonically. Any telephonic hearing will be made accessible to people with disabilities.

The principal author of these regulations is Mayer R. Samuels, Office of the Associate Chief Counsel (Passthroughs and Special Industries), IRS. However, other personnel from the IRS and Treasury Department participated in their development.

26 CFR Part 1

Income taxes, Reporting and recordkeeping requirements.

26 CFR Part 20

Estate taxes, Reporting and recordkeeping requirements.

26 CFR Part 25

Gift taxes, Reporting and recordkeeping requirements.

Accordingly, 26 CFR parts 1, 20, and 25 are proposed to be amended as follows:

PART 1--INCOME TAXES

Paragraph 1. The authority citation for part 1 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *

Par. 2. Section 1.170A-12 is amended by:

1. Revising paragraphs (b)(2) and (3).

2. Adding paragraph (b)(4).

3. Revising paragraphs (e)(2) and (f)

The revisions and addition read as follows:

§1.170A-12 Valuation of a remainder interest in real property for contributions made after July 31, 1969.

* * * * *

(b) * * *

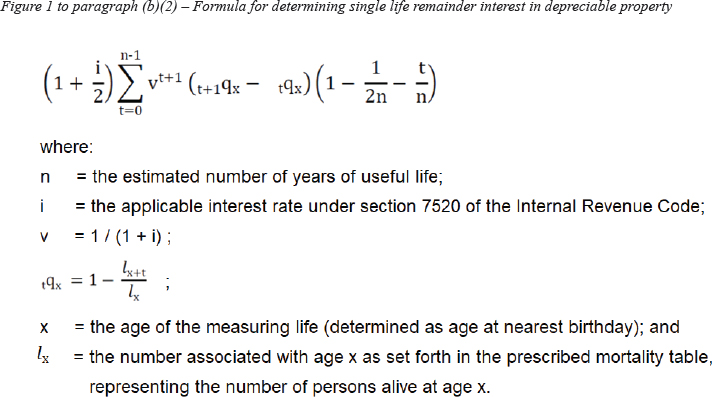

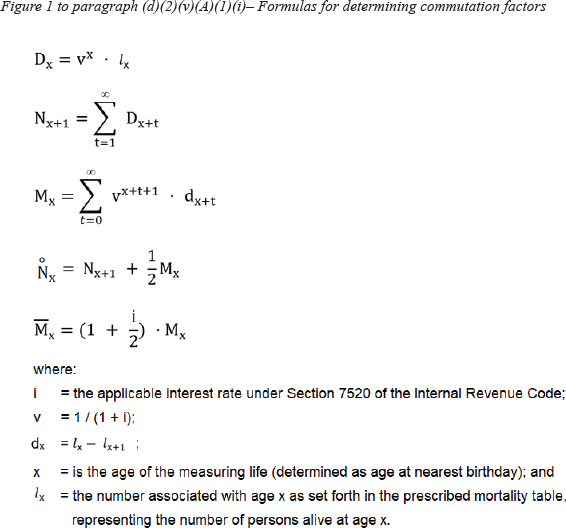

(2) Computation of depreciation factor. If the valuation of the remainder interest in depreciable property is dependent upon the continuation of one life, a special factor must be used. The factor determined under this paragraph (b)(2) is carried to the fifth decimal place. The special factor is to be computed on the basis of the interest rate and life contingency rates from the mortality table prescribed in §20.2031-7 of this chapter (or for periods before [applicability date of the Treasury decision adopting these regulations as final regulations], §20.2031-7A of this chapter) and on the assumption that the property depreciates on a straight-line basis over its estimated useful life. For transfers for which the valuation date is on or after [applicability date of the Treasury decision adopting these regulations as final regulations], special factors for determining the present value of a remainder interest following one life may be computed by taxpayers based on Table 2010CM, found in §20.2031-7(d)(7)(ii) of this chapter, and using the formula provided in this paragraph (b)(2). Alternatively, taxpayers may use the actuarial factors provided in Table C to determine the special factor for the remainder interest following one life. Table C will be available beginning May 5, 2022, at no charge, electronically via the IRS website at https://www.irs.gov/retirement-plans/actuarial-tables (or a corresponding URL as may be updated from time to time). IRS Publication 1459, “Actuarial Valuations Version 4C” (2022), references and explains Table C and provides examples describing the computation. This publication will be available after [date of publication of the final rule in the Federal Register]. For transfers for which the valuation date is on or after May 1, 2009, and before [applicability date of the Treasury decision adopting these regulations as final regulations], special factors for determining the present value of a remainder interest following one life and an example describing the computation are contained in the previous version of Table C, which is currently available, at no charge, electronically via the IRS website at https://www.irs.gov/retirement-plans/actuarial-tables. IRS Publication 1459, “Actuarial Valuations Version 3C” (2009), references and explains this version of Table C and provides examples describing the computation. See, however, §1.7520-3(b) (relating to exceptions to the use of prescribed tables under certain circumstances). Otherwise, in the case of the valuation of a remainder interest following one life, the special factor may be obtained through use of the formula in Figure 1 to this paragraph (b)(2). The prescribed mortality table is Table 2010CM as set forth in §20.2031-7(d)(7)(ii) of this chapter, or for periods before [applicability date of the Treasury decision adopting these regulations as final regulations], the appropriate table found in §20.2031-7A of this chapter. Table 2010CM is referenced by IRS Publication 1459, “Actuarial Values Version 4C.” The mortality tables prescribed for periods before [applicability date of the Treasury decision adopting these regulations as final regulations] are referenced by prior versions of IRS Publication 1459.

(3) Sample factors from actuarial Table S. The present value of a remainder interest dependent on the termination of one life is determined by using the formula in §20.2031-7(d)(2)(ii)(B) of this chapter to derive factors from the appropriate mortality table. For the convenience of taxpayers, actuarial factors have been computed by IRS and appear in Table S. The complete Table S can be found on the IRS website at https://www.irs.gov/retirement-plans/actuarial-tables. For purposes of the example in paragraph (b)(4) of this section, the following factors from Table S will be used:

Table 1 to paragraph (b)(3)

| Factors from Table S - Based on Table 2010CM | |||

|---|---|---|---|

| Interest at 3.2 Percent | |||

| Age | Annuity | Life Estate | Remainder |

| 62 | 14.6131 | 0.46762 | 0.53238 |

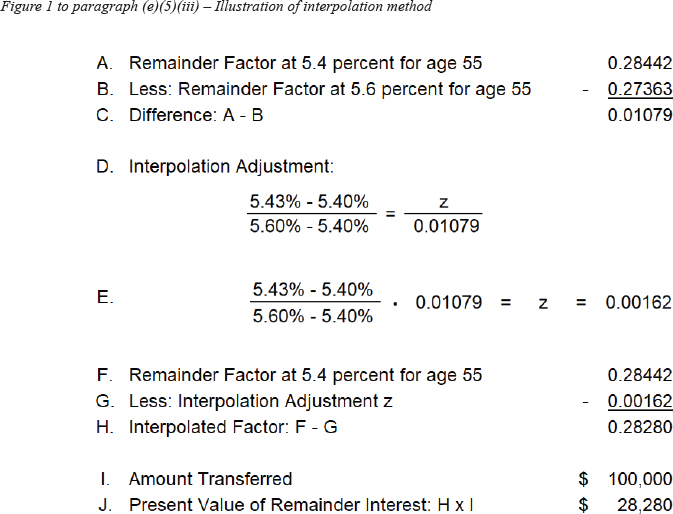

(4) Example. After [applicability date of the Treasury decision adopting these regulations as final regulations], A, who is 62, donates to Y University a remainder interest in a personal residence, consisting of a house and land, subject to a reserved life estate in A. At the time of the gift, the land has a value of $30,000 and the house has a value of $100,000 with an estimated useful life of 28 years, at the end of which period the value of the house is expected to be $10,000. The portion of the property considered to be depreciable is $90,000 (the value of the house ($100,000) less its expected value at the end of 28 years ($10,000)). The portion of the property considered to be nondepreciable is $40,000 (the value of the land at the time of the gift ($30,000) plus the expected value of the house at the end of 28 years ($10,000)). At the time of the gift, the interest rate prescribed under section 7520 is 3.2 percent. Based on an interest rate of 3.2 percent, the remainder factor for $1.00 prescribed in §20.2031-7(d) and found in Table S for a person age 62 is 0.53238. The value of the nondepreciable remainder interest is $21,295.20 (0.53238 times $40,000). The factor for the remainder interest in depreciable property is computed under the formula described in paragraph (b)(2) of this section and is 0.19392. (This factor, 0.19392, may instead be determined by using Table C, which can be found on the IRS website at https://www.irs.gov/retirement-plans/actuarial-tables, and following the method provided in IRS Publication 1459, “Actuarial Values Version 4C”.) The value of the depreciable remainder interest is $17,452.80 (0.19392 times $90,000). Therefore, the value of the remainder interest is $38,748.00 ($21,295.20 plus $17,452.80).

* * * * *

(e) * * *

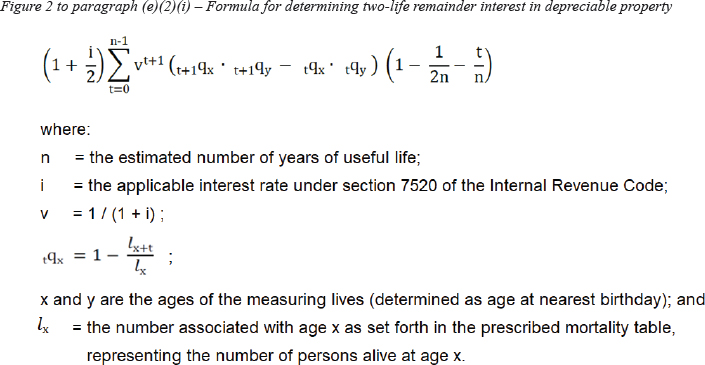

(2) In the case of the valuation of a remainder interest following two lives, the special factor may be obtained through use of the formula in Figure 2 to this paragraph (e)(2). The prescribed mortality table is Table 2010CM as set forth in §20.2031-7(d)(7)(ii) of this chapter, or for periods before [applicability date of the Treasury decision adopting these regulations as final regulations], the appropriate table found in §20.2031-7A of this chapter. Table 2010CM is referenced by IRS Publication 1459, “Actuarial Values Version 4C.” The mortality tables prescribed for periods before [applicability date of the Treasury decision adopting these regulations as final regulations] are referenced by prior versions of IRS Publication 1459.

* * * * *

(f) Applicability date. This section applies to contributions made after July 31, 1969, except that paragraphs (b)(2), (3), and (4) and (e)(2) of this section apply to all contributions made on or after [applicability date of the Treasury decision adopting these regulations as final regulations].

Par. 3. Section 1.170A-14 is amended:

1. In paragraph (h)(4) by designating Example 1 through 12 as paragraphs (h)(4)(i) through (xii), respectively.

2. By revising newly designated paragraph (h)(4)(ii).

3. In newly designated paragraphs (h)(4)(iii) and (iv) by removing “Example 2” and adding “paragraph (h)(4)(ii) of this section (Example 2)” in its place.

4. In newly designated paragraph (h)(4)(v) by removing “Example 4” and adding “paragraph (h)(4)(iv) of this section (Example 4)” in its place.

5. In newly designated paragraph (h)(4)(vi) by removing “Example 2” and adding “paragraph (h)(2)(ii) of this section (Example 2)” in its place.

6. In newly designated paragraph (h)(4)(viii) by removing “Example 7” and adding “paragraph (h)(4)(vii) of this section (Example 7)” in its place.

7. In newly designated paragraph (h)(4)(xi) by removing “example (10)” and adding “paragraph (h)(4)(x) of this section (Example 10)” in its place.

8. By revising paragraph (j).

The revisions read as follows:

§1.170A-14 Qualified conservation contributions.

* * * * *

(h) * * *

(4) * * *

(ii) Example 2. In 1984 B, who is 62, donates a remainder interest in Greenacre to a qualifying organization for conservation purposes. Greenacre is a tract of 200 acres of undeveloped woodland that is valued at $200,000 at its highest and best use. Under §1.170A-12(b), the value of a remainder interest in real property following one life is determined under §25.2512-5 of this chapter (Gift Tax Regulations). (See §25.2512-5A of this chapter with respect to the valuation of annuities, interests for life or a term of years, and remainder or reversionary interests transferred before [applicability date of the Treasury decision adopting these regulations as final regulations].) For transfers occurring after November 30, 1983, and before May 1, 1989, the single life remainder factors, valued at 10 percent, can be found in Table A of §20.2031-7A(d)(6) of this chapter. Accordingly, the value of the remainder interest, and thus the amount eligible for an income tax deduction under section 170(f), is $55,996 ($200,000 × 0.27998).

* * * * *

(j) Applicability dates. Except as otherwise provided in paragraph (g)(4)(ii) and paragraph (i) of this section, this section applies only to contributions made on or after December 18, 1980. Paragraph (h)(4)(ii) of this section applies on and after [applicability date of the Treasury decision adopting these regulations as final regulations].

Par. 4. Section 1.642(c)-6 is amended by:

1. Revising paragraph (d).

2. Redesignating paragraph (e) as paragraph (g) of §1.642(c)-6A.

3. Adding new paragraph (e) and revising paragraph (f).

The revisions and addition read as follows:

§1.642(c)-6 Valuation of a remainder interest in property transferred to a pooled income fund.

* * * * *

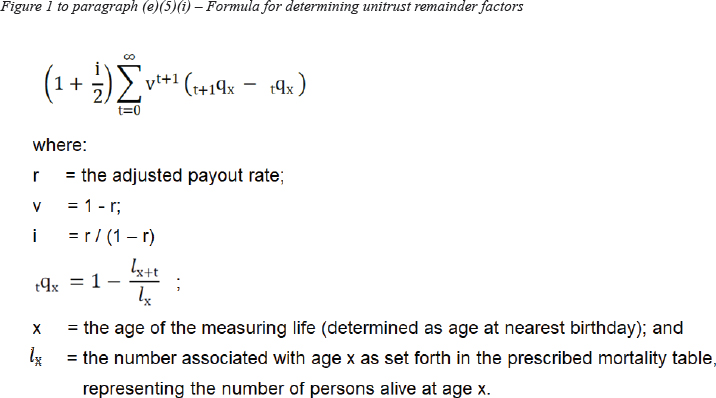

(d) Valuation. The present value of the remainder interest in property transferred to a pooled income fund on or after [applicability date of the Treasury decision adopting these regulations as final regulations], is determined under paragraph (e) of this section. The present value of the remainder interest in property transferred to a pooled income fund for which the valuation date is before [applicability date of the Treasury decision adopting these regulations as final regulations] is determined under the following sections:

Table 6 to paragraph (d)

| Valuation Dates | Applicable Regulations | |

|---|---|---|

| After | Before | |

| - | 01-01-52 | 1.642(c)-6A(a) |

| 12-31-51 | 01-01-71 | 1.642(c)-6A(b) |

| 12-31-70 | 12-01-83 | 1.642(c)-6A(c) |

| 11-30-83 | 05-01-89 | 1.642(c)-6A(d) |

| 04-30-89 | 05-01-99 | 1.642(c)-6A(e) |

| 04-30-99 | 05-01-09 | 1.642(c)-6A(f) |

| 04-30-09 | AD | 1.642(c)-6A(g) |

AD = [applicability date of the Treasury decision adopting these regulations as final regulations].